Welcome to this week’s Tranched newsletter.

The build phase of digital finance infrastructure has been underway for years.

But it has never been happening everywhere at once, in the same week, with this much institutional weight behind it. The question was always which geography would set the template. This week, the answer started to look more complicated than anyone expected.

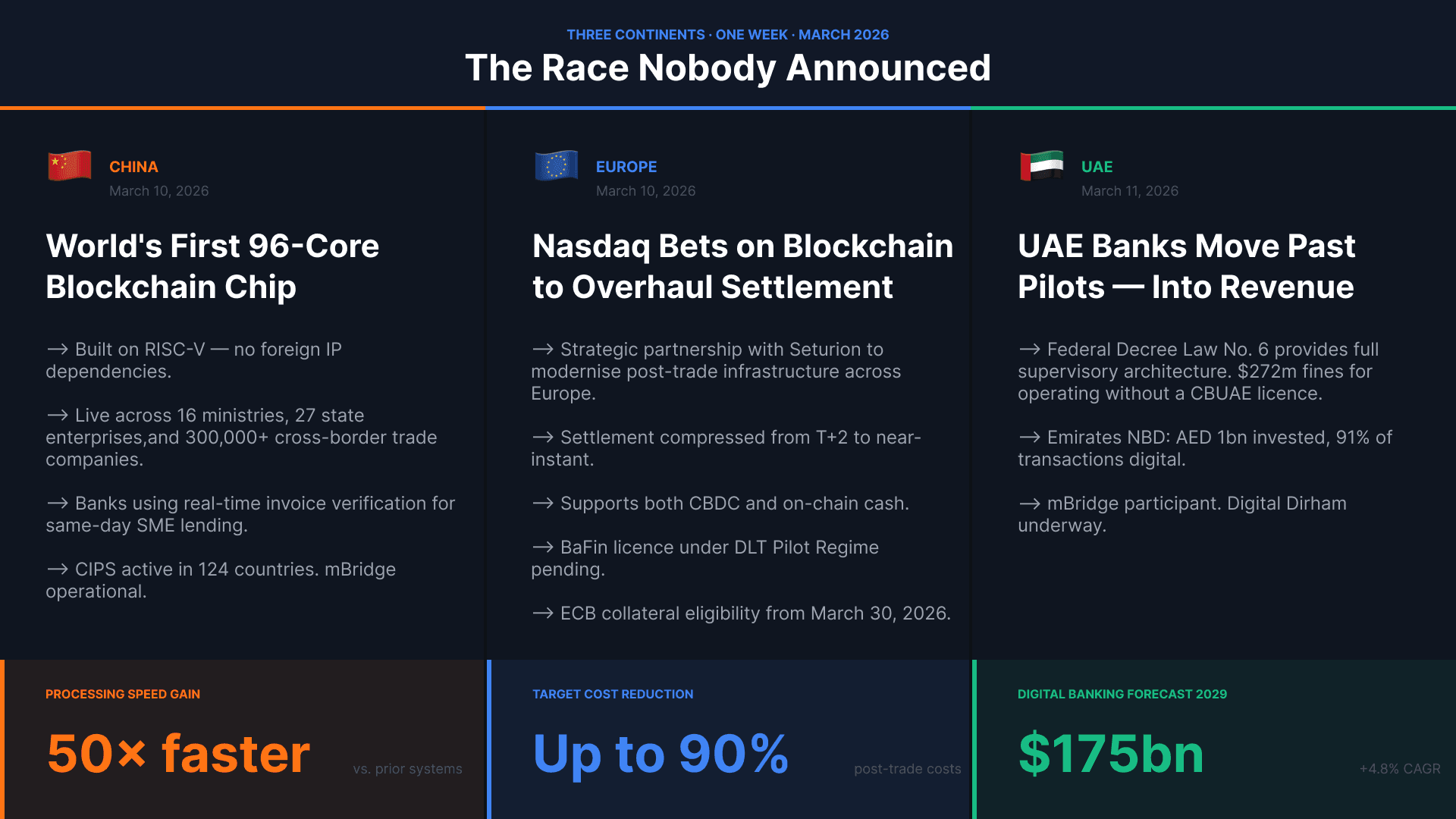

On March 10, Beijing confirmed that China had built the world's first 96-core blockchain acceleration chip. The same day, Nasdaq announced a partnership to overhaul European post-trade settlement on distributed ledger infrastructure. The following morning, a report out of Dubai declared that UAE banks had moved past blockchain pilots and into revenue-generating products.

Three continents. Three announcements. One week.

Across every major financial geography, the build phase of digital finance infrastructure has arrived simultaneously, and the decisions being made right now about who controls that infrastructure, and under what regulatory architecture it operates, will shape how capital moves for the next decade.

This week, Tranched maps the field.

China: Infrastructure as Sovereignty

Beijing's new chip, developed under the national Chang'An Chain initiative, delivers smart contract processing speeds 50 times faster than current systems and signature verification 20 times quicker. Cryptographic tasks that previously consumed over 60% of a node's computing resources now complete in microseconds.

The chip is already live across 16 central government ministries, 27 major state enterprises including State Grid, China Telecom, and Sinopec, and more than 300,000 cross-border trade companies. Banks on the network are using real-time invoice verification to offer same-day lending to small and medium-sized enterprises.

Crucially, the chip runs on RISC-V, an open-source instruction set architecture that gives China complete domestic control over its technology stack. There are no foreign IP dependencies and no licensing chokepoints.

Analysts watching the project closely are framing it as a deliberate move toward real-world asset migration: institutional processes in customs, taxation, shipping, and cross-border payments being brought onto infrastructure Beijing controls end to end.

The geopolitical context is impossible to separate from the technical.

China has built CIPS, its own cross-border interbank payment system, now with participants across 124 countries. Project mBridge, the multi-CBDC settlement platform developed alongside Hong Kong, the UAE, and Thailand, demonstrated that cross-border transactions can settle in seconds at a fraction of correspondent banking costs. The BIS handed the project to participating central banks in late 2024. The infrastructure for a parallel settlement architecture, operating alongside SWIFT-dependent rails, is operational.

UAE: Clarity as Competitive Advantage

The UAE has demonstrated that regulatory architecture is itself a form of infrastructure.

Federal Decree Law No. 6 of 2025 gave the Central Bank of the UAE direct supervisory authority over the entire virtual asset ecosystem: decentralised finance, wallets, stablecoins, custody, and lending. Operating without a CBUAE licence now carries fines of up to AED 1B, approximately $272M. That is a structural deterrent that converts board-level uncertainty into a solved problem.

Emirates NBD has invested over AED 1B in digital transformation, with 91% of transactions now running through digital channels. Stephen Richardson of Fireblocks has stated that what the industry predicted would happen in 2026 is already visible in the UAE today: real money running on blockchain infrastructure. The UAE's digital banking sector is forecast to reach $175B by 2029, growing at a compound annual rate of 4.8%.

The strategic logic extends beyond domestic banking. Project mBridge positions the UAE as a participant in the multilateral settlement architecture being built across Asia and the Gulf.

Examples?

The Digital Dirham CBDC rollout is underway.

Tether launched a Dirham-backed stablecoin in 2024 targeting remittance and trade corridors.

Dubai's Virtual Assets Regulatory Authority and Abu Dhabi Global Market offer distinct licensing tracks for different institutional use cases.

The UAE is building a neutral, legally clear, technically capable hub through which capital from multiple jurisdictions can flow without choosing sides.

For structured finance and cross-border transactions specifically, that positioning is worth watching closely.

Europe: The Paradox of Good Frameworks

This week's European headline belongs to Nasdaq, which announced a strategic partnership with Seturion, the blockchain post-trade platform operated by Boerse Stuttgart Group, to modernise securities settlement across the continent. The promise is substantial: post-trade costs reduced by up to 90%, settlement compressed from T+2 to near-instant, support for both central bank digital currency and on-chain cash. The initial focus is structured products, with a broader rollout planned into 2027.

Europe has the frameworks.

→ MiCA is in force.

→ The DLT Pilot Regime is active.

→ The ECB's Pontes programme will bridge DLT platforms to TARGET Services from Q3 2026.

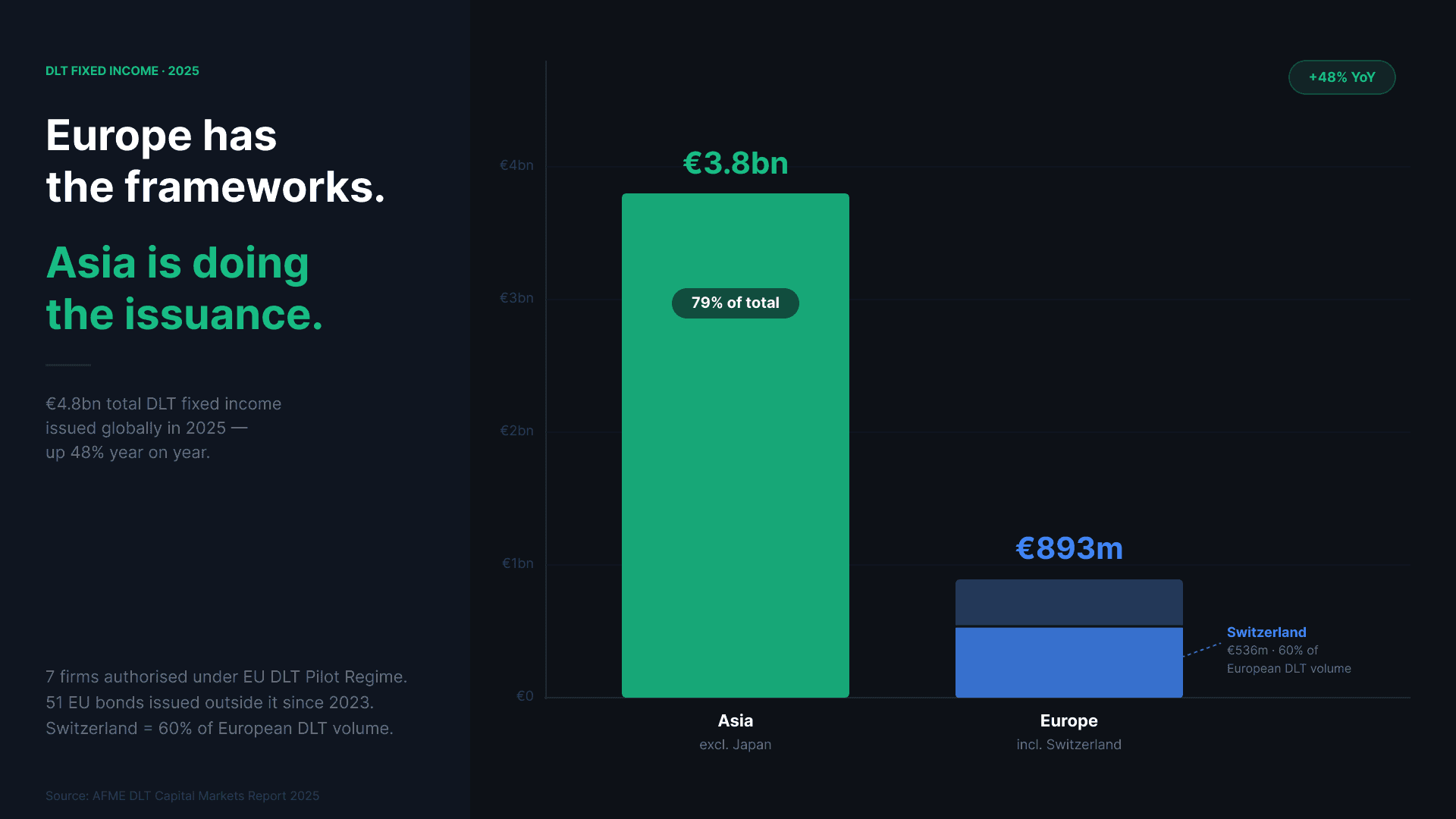

From March 30 this year, the ECB will accept DLT-based securities as eligible collateral, a policy decision that may do more for institutional adoption than any single pilot. The AFME data from 2025 shows €4.8B in DLT fixed income issuance, up 48% year-on-year.

The friction is in the execution. Seturion's full European deployment depends on a BaFin licence under the DLT Pilot Regime, an application currently under review. Seven firms have been authorised under the regime so far, yet 51 EU debt securities have been issued outside it since 2023. Switzerland, operating under a separate framework via SIX Digital Exchange, accounted for 60% of all European DLT bond volume in 2025. The regulatory architecture is coherent. The implementation velocity is not matching it.

This is the European paradox in digital finance: the most sophisticated regulatory frameworks on earth, producing the slowest institutional deployments.

The Nasdaq-Seturion partnership is the right structural move. Whether it translates into production at scale before the BaFin approval process runs its course remains the open question.

United States: Capital Ready, Rules Pending

The US brings the largest institutional capital base to this race and, for the moment, the most unresolved regulatory picture.

The GENIUS Act, passed in July 2025, established the first federal framework for stablecoins, formally classifying payment stablecoins as non-securities and providing a structured licensing regime.

On February 18 this year, the SEC and CFTC announced a joint oversight agreement on digital assets, moving away from what had been characterised as regulation by enforcement toward a coordinated framework. SEC Chair Paul Atkins has predicted that US securities markets could move substantially on-chain within two years.

The CLARITY Act, designed to resolve jurisdictional boundaries between the SEC and CFTC across the broader digital asset landscape, has passed the House but remains stalled in the Senate, caught in a dispute over whether stablecoin yield restrictions should be extended further.

Despite the regulatory stall, institutional appetite is unambiguous.The NYSE is developing a blockchain-based platform for 24/7 trading of tokenised securities. BlackRock's BUIDL fund, the largest tokenised Treasury product in the world at $2.3B, is being used as collateral on-chain.

The US pattern is familiar: large-scale private sector movement with regulatory resolution trailing behind.

The gap between intent and infrastructure is closing, but it has not yet closed.

Singapore: The Blueprint

Singapore operates at a different scale to the other players on this map, but the model it has developed through Project Guardian has become arguably the most-studied regulatory approach in institutional digital finance.

Launched in 2022, Project Guardian now involves over 40 institutional participants including JPMorgan, DBS, Franklin Templeton, Hamilton Lane, and Standard Chartered. Pilots have covered tokenised bonds, foreign exchange, and fund structures, with live transactions running across public and private blockchain infrastructure. The MAS has published detailed operational frameworks for tokenised funds, introduced a Global-Asia Digital Bond Grant to catalyse issuance, and expanded the initiative to include the Deutsche Bundesbank, Swift, and the World Bank as members.

The MAS model treats regulation as a collaborative process with the institutions that will eventually operate the infrastructure, iterating in real time through sandbox pilots before codifying rules.

It is slower than the UAE's top-down clarity and faster than Europe's consensus-driven process.

Several jurisdictions, including the UK's FCA through its participation in Project Guardian, are adopting elements of it.

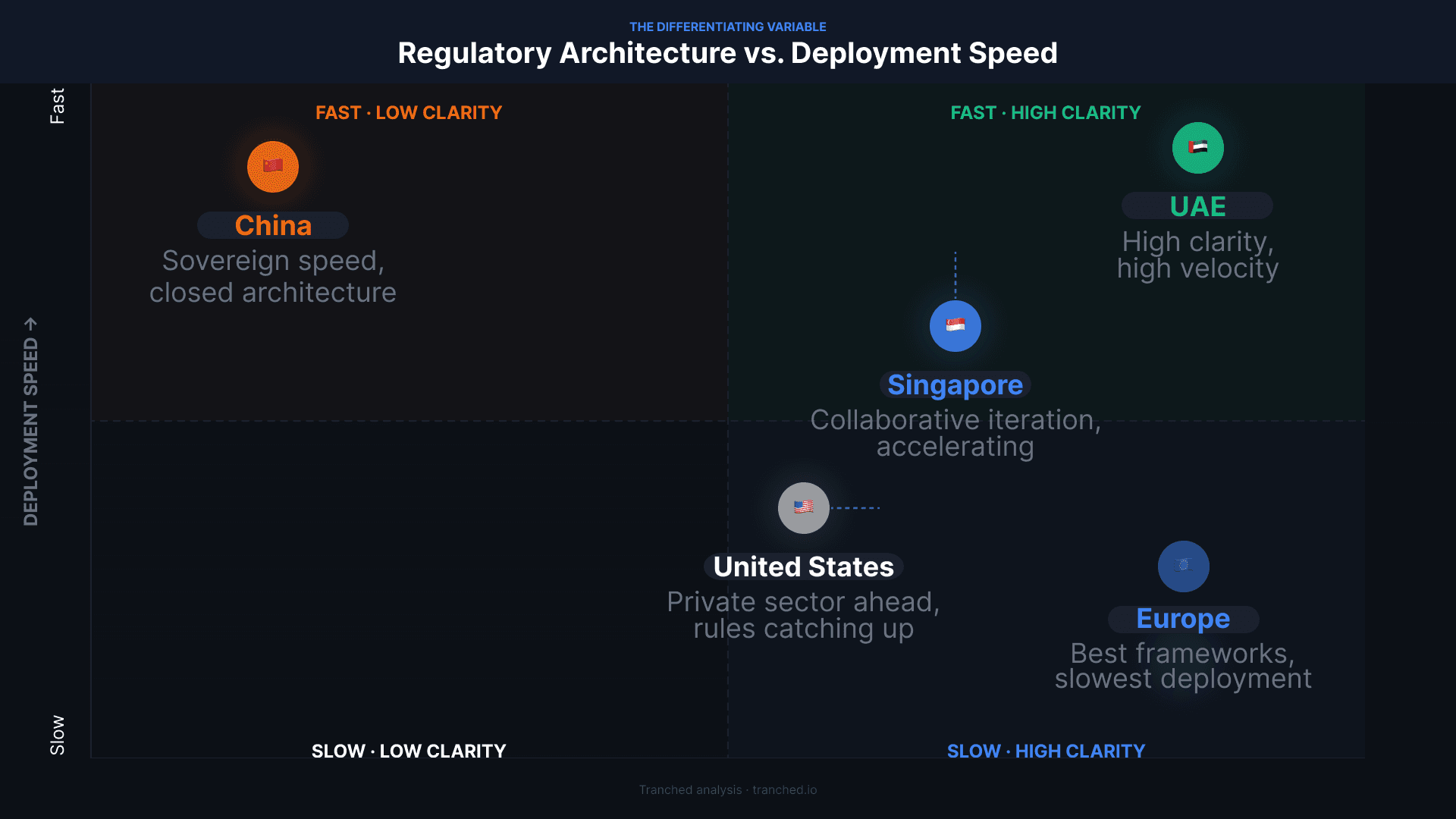

The Variable That Decides the Race

Five geographies, five strategies.

→ China moves through sovereign control.

→ The UAE moves through regulatory clarity.

→ Europe moves through institutional consensus.

→ The United States moves through private sector acceleration followed by regulatory catch-up.

→ Singapore moves through collaborative iteration.

The technology across each of these jurisdictions is increasingly comparable.

What differs is the architecture that governs it: how quickly institutions can commit capital, how freely that capital can move, and whether the infrastructure being built is designed for global interoperability or domestic control.

For anyone operating in structured finance, securitisation, or cross-border capital markets, these distinctions are starting to carry direct implications.

The post-trade infrastructure that Nasdaq is building in Europe is, structurally, an answer to the settlement fragmentation that has historically constrained European ABS markets. China's closed architecture limits the international participation that makes CLO and SRT markets liquid. The UAE's neutral positioning makes it a natural candidate for cross-border tokenised structured product clearing as those markets develop.

The race was never announced. But the finishing line is coming into view.