Securitisation

Welcome to this week’s Tranched newsletter.

Over the past year, tokenised funds, sovereign bonds, and repo markets have all scaled materially, while central banks and regulators have begun integrating distributed ledger infrastructure into core market operations. The result is the early formation of a parallel financial architecture, one designed for instantaneous settlement, continuous liquidity, and global interoperability.

This week’s newsletter examines how quickly that transition is accelerating, where adoption is taking hold first, and why the institutions building on-chain infrastructure today are positioning themselves to define the next generation of capital markets.

On February 21, BNP Paribas Asset Management tokenised a money market fund share class on Ethereum, essentially permissioned tokens on a permissionless chain.

It is one signal of how the convergence between traditional capital markets and public blockchain rails is accelerating.

Nine days earlier, on February 12, HM Treasury appointed HSBC to build the platform for DIGIT, the UK's first-ever digital gilt.

And on February 2, J.P. Morgan Asset Management launched MONY, a tokenised money market fund on public Ethereum, available through Morgan Money, its institutional liquidity platform that already serves hundreds of the world's largest corporations.

In the space of three weeks, three of the world's largest financial institutions all made moves onto the same public blockchain.

Reinforcing the institutional trajectory, AFME's dropped its 2025 full-year report on DLT-based capital markets last week, spotlighting an architecture of a parallel financial system where bonds, equities, funds, and sovereign debt are being re-issued as programmable, on-chain instruments.

This week, we unpack the hard numbers behind tokenised fixed income and funds, before examining how sovereign issuers are setting the pace. We then turn to the banks building directly on public infrastructure, Europe’s regulatory paradox, and the market structure gaps that will determine whether this remains a parallel system, or becomes the new one.

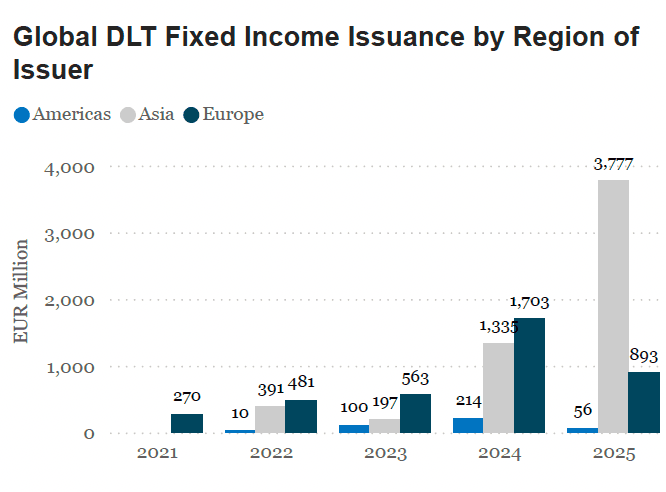

Global DLT fixed income issuance hit €4.8B in 2025, up 48% from €3.25B in 2024. Asia accounted for 79% of that total (roughly €3.8B) led by the Hong Kong Monetary Authority's multi-currency sovereign digital bonds and HSBC Orion, which alone facilitated over €2.3B in issuance across sovereign, supranational, and corporate sectors.

Source: AFME Report, Page 5 (Chart 1.2, Page 12)

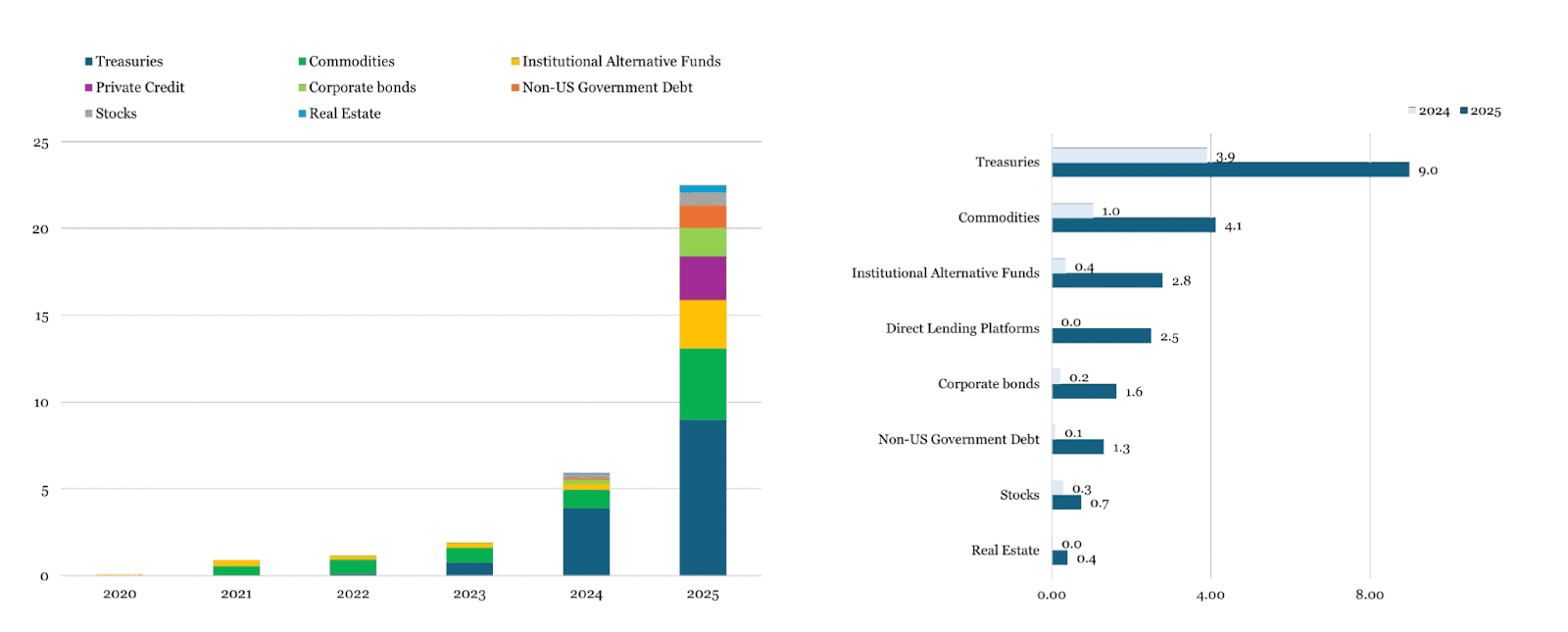

Tokenised US Treasuries reached $9B, up 130% year-on-year from $3.9B. But the more striking figure sits one layer up the capital stack: tokenised fund AUM surged to $10.9B, a 420% increase from 2024, driven primarily by BlackRock's BUIDL fund, which grew 168% and remains the single largest tokenised Treasury product. Some $6.6B of the total is allocated to US government securities within money market fund structures.

Here's the detail that matters: 27% of US Treasury tokenisations are direct bond tokenisations, no fund wrapper, no intermediary. For equities, 71% of tokenisations are direct stocks or baskets. The fund-of-everything model isn't the only path. Direct tokenisation is already here.

Source: RWA.xyz, AFME, AFME Report, Page 45 (Chart 6.2, Page 45)

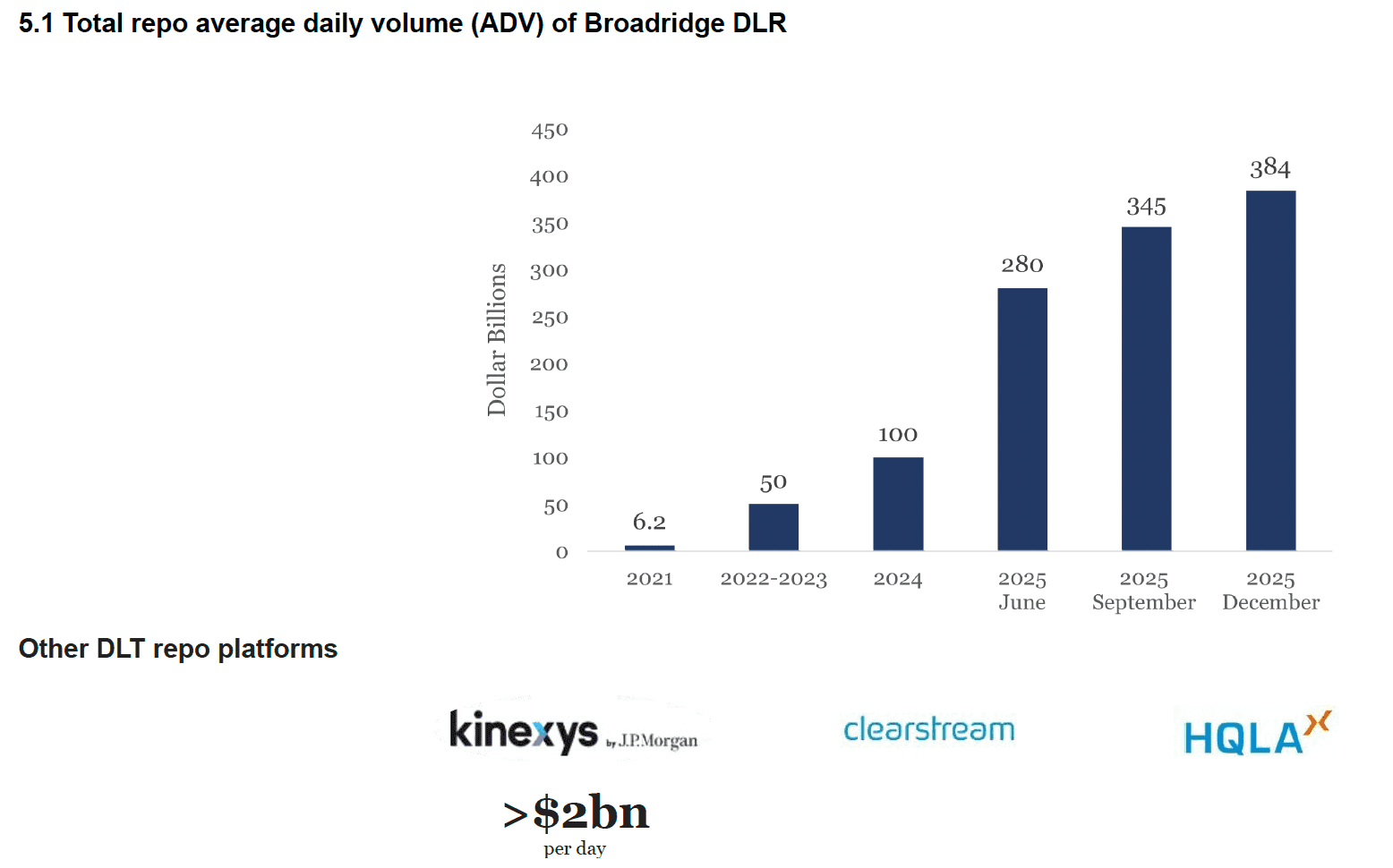

Then there's repo, the market's plumbing. Broadridge's DLR platform processed an average of $384B per day in December 2025, according to data compiled by AFME and RWA.xyz. That's up from $100B per day in 2024 and just $6.2B per day in 2021. JP Morgan's Kinexys handles over $2B per day across all applications, including intraday repo.

Think about that trajectory for a moment.

A 62x increase in daily DLT repo volume in four years. At what point does the "pilot" label stop applying?

Source: AFME, Ledger Insights, Broadridge, JPM, ECB, AFME Report, Page 41 (Chart 5.1, Page 41)

Sovereigns Are Setting the Pace

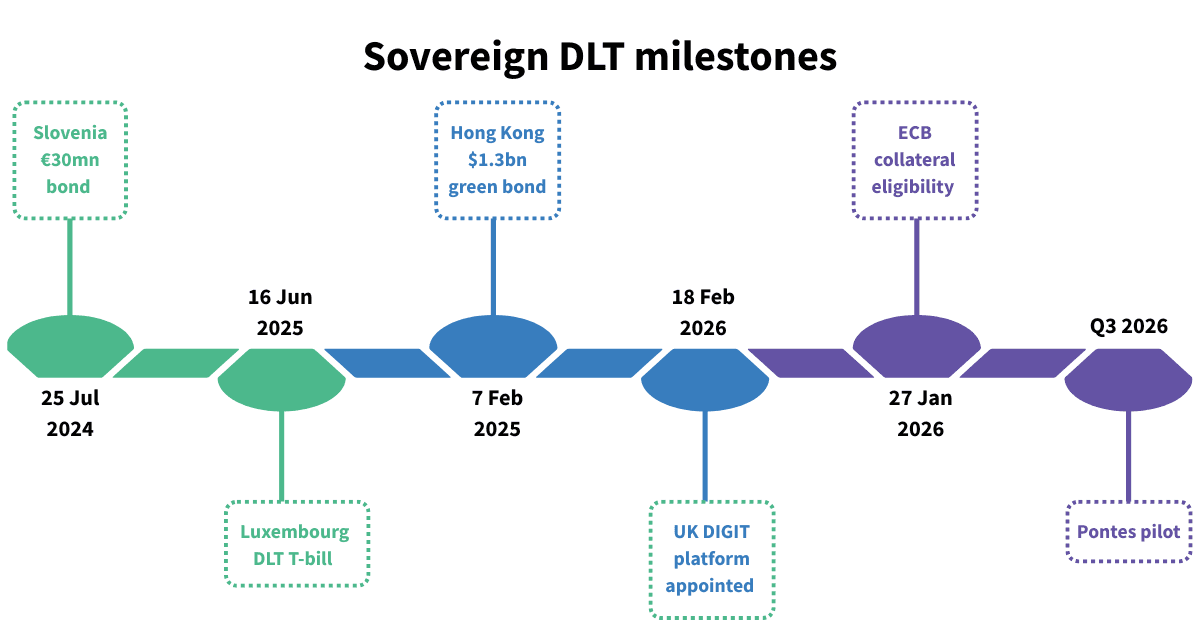

Perhaps the most consequential shift in 2025 was the normalisation of sovereign DLT issuance. The Grand Duchy of Luxembourg issued its first DLT treasury bill via HSBC Orion in 2025, making them the second EU sovereign to go digital after Slovenia's €30M bond in 2024. The Hong Kong government issued the world's largest digital bond to date: a multi-currency, $1.3B-equivalent green bond, also on HSBC Orion.

And then came DIGIT. On February 12, HM Treasury selected HSBC Orion (the same platform behind Hong Kong's and Luxembourg's issuances) to power the UK's Digital Gilt Instrument pilot. The instrument will be digitally native, short-dated, settled on-chain within the UK's Digital Securities Sandbox, and entirely separate from the Debt Management Office's existing gilt programme. HSBC's Patrick George called it positioning the UK "in pole position among the G7 nations to issue the first-ever tokenised sovereign bonds on a blockchain."

AFME's Managing Director James Kemp, in a statement the same day, pushed for more: the UK should "move at pace and set an ambitious issuance calendar that will build confidence that the UK supports capital markets digitisation."

A single pilot is a proof of concept and a recurring programme is a market.

The ECB is taking a different path.

Having concluded its DLT settlement trials in November 2024, the Eurosystem announced two successor programmes: Pontes, a short-term bridge connecting DLT platforms to TARGET Services (pilot expected Q3 2026), and Appia, a longer-term integrated European settlement ecosystem.

But the single most consequential decision?

From March 30, 2026, the ECB will accept DLT-based securities as eligible collateral. That one policy change may matter more than any pilot programme.

Banks Go Native

The institutional stack is filling in from every direction in February 2026, with remarkable velocity.

J.P. Morgan Asset Management's MONY fund, launched February 2 on public Ethereum via Kinexys Digital Assets, was the first tokenised money market fund from a G-SIB bank. John Donohue, J.P. Morgan's head of Global Liquidity, called Morgan Money "the first institutional liquidity trading platform to integrate traditional and onchain assets" and predicted other G-SIBs would "follow our lead."

He didn't have to wait long.

On February 21, BNP Paribas Asset Management issued a tokenised share class of a French-domiciled money market fund on Ethereum. This was its second tokenisation trial but the first on a permissionless chain. Edouard Legrand, BNP Paribas AM's chief digital and data officer, described the move as supporting "ongoing efforts to explore how tokenisation can contribute to greater operational efficiency and security within a regulated framework."

Below the fund layer, tokenised deposits are taking shape. On February 18, Bloomberg reported that five US banks: First Horizon, Huntington Bancshares, KeyCorp, M&T Bank, and Old National Bancorp, plan to launch a tokenised deposit network by Q4 2026. The network, built through the Cari Network and led by former Comptroller of the Currency Gene Ludwig, will initially facilitate money movement between the banks' own customers. Ludwig's framing was deliberate: tokenised deposits should "strengthen, not displace, the regulated banking system."

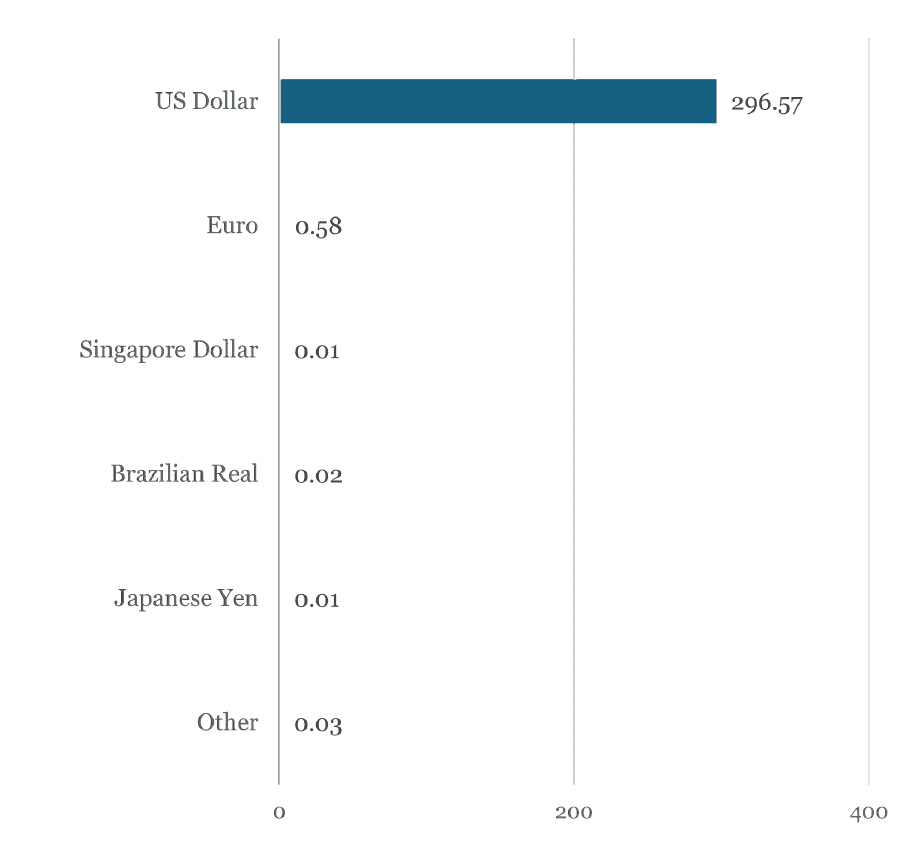

Stablecoins continue to serve as connective tissue. Market capitalisation reached a record $297B by year-end 2025, up 53% from $194 B, with USD-pegged tokens accounting for 99.7% of supply. Bernstein's analysts, led by Gautam Chhugani, forecast total stablecoin supply reaching approximately $420B in 2026, a 56% year-on-year increase, driven by cross-border payments, remittances, and "agentic payments."

European stablecoins remain vanishingly small: $586M total, or 0.2% of global market cap (98.6% euro-denominated, with small GBP and CHF fractions).

But momentum is building.

In the EU, A 12-bank European consortium called Qivalis is developing a MiCAR-compliant euro stablecoin. Overall, AFME's data shows eight global banks had issued stablecoins by December 2025, with major Japanese and Korean institutions exploring issuance.

How long will it be before every G-SIB has a stablecoin, a tokenised fund, and a digital bond desk as standard product lines?

Source: RWA.xyz, Coingecko, AFME Report, Page 35 (Chart 4.1, Page 35)

Europe's Paradox

Still then, the AFME data reveals an uncomfortable dynamic. While Asian issuance surged and sovereign adoption accelerated globally, European DLT bond issuance fell to €893M across 15 deals in 2025, equating to roughly half of 2024's €1.7B. The explanation is partly mechanical as the ECB's DLT settlement trials, which contributed over €1B in 2024, concluded in November of that year.

But the structural picture is more troubling. The EU's DLT Pilot Regime, which was designed as a regulatory sandbox for tokenised securities, has authorised seven firms (CSD Prague, 21X AG, 360X AG, UAB Axiology, LISE SA, Securitize Europe, and one other).

The result so far? Two debt securities and 17 equity tokens through the regime, versus 51 debt securities issued by EU entities since 2023 outside of it.

Switzerland, operating under the SNB's Helvetia Pilot via SIX Digital Exchange, issued €536M in 2025, which accounted for 60% of all European volume. Germany contributed €300M. Luxembourg added €50M.

Europe has the regulation, the frameworks, the sandboxes, the pilot regimes. What it doesn't have is velocity.

The Convergence

Let’s Zoom out for a moment.

In twelve months…

Tokenised Treasuries more than doubled to $9B.

Tokenised fund AUM grew fivefold to $10.9B. DLT repo volumes nearly quadrupled to $384B per day.

Two G-SIB banks, J.P. Morgan and BNP Paribas, launched tokenised money market funds on public Ethereum.

The UK appointed a platform for its first digital gilt.

Five US banks began building a tokenised deposit network.

And the SEC, on January 28, published its formal statement on tokenised securities, confirming that existing securities law applies to tokenised instruments regardless of format.

No matter where you are standing, convergence is happening from all angles. The asset classes are converging, the infrastructure is converging and the regulatory frameworks are converging.

Bernstein's analysts call it a tokenisation "supercycle," forecasting on-chain tokenised asset value to double from $37B to roughly $80B in 2026. We're past the question of whether traditional finance adopts blockchain infrastructure.

The question now is which institutions will own the rails, and which will pay rent?