Private Credit

Welcome to this week’s Tranched newsletter.

In this issue, we look at what happens when private credit's infrastructure fails to keep pace with its growth. A new survey of 38 senior operators, nearly half managing $50B+ in assets, reveals that the industry's most urgent problem is a unified data model that does not yet exist.

We examine why LP pressure is accelerating that demand, why the market keeps conflating asset-based lending collapses with direct lending redemptions, and what the non-linear pattern of AI adoption across firm sizes tells us about where infrastructure is heading next.

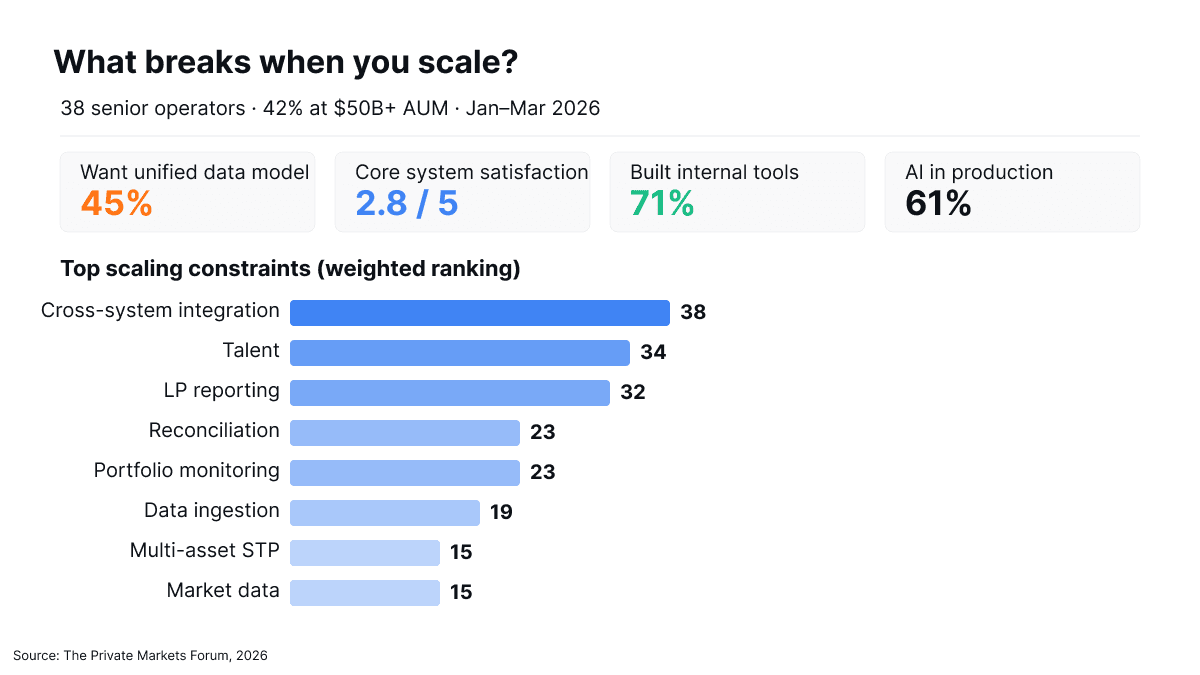

In January, the Private Markets Forum surveyed 38 senior private credit operators. 42% of them manage $50B or more in assets. These are CTOs, Heads of Data, and operations leaders at the largest platforms in the market. The question was straightforward: what breaks when you scale?

What the survey found

The findings converge on a clear picture. 45% of respondents said that if they could solve one operational problem, it would be a unified data model across strategies and systems. Cross-system data integration ranked as the number one weighted scaling constraint. Core system satisfaction averaged 2.8 out of 5, and 71% of firms have built internal tools because nothing on the market fits.

This is an industry that has scaled in assets faster than it has scaled in infrastructure. The direct lending team uses one system. The ABF team uses another. The accounting team uses a third. The reporting team stitches them together manually. As one respondent put it: too much of the day is spent connecting dots between systems via email and spreadsheets, rather than finding the next deal.

47% of respondents rated their core portfolio system at the midpoint, 3 out of 5. That score reflects tolerance. The market is enduring mediocre tools because better alternatives do not exist, or the cost of switching is prohibitive.

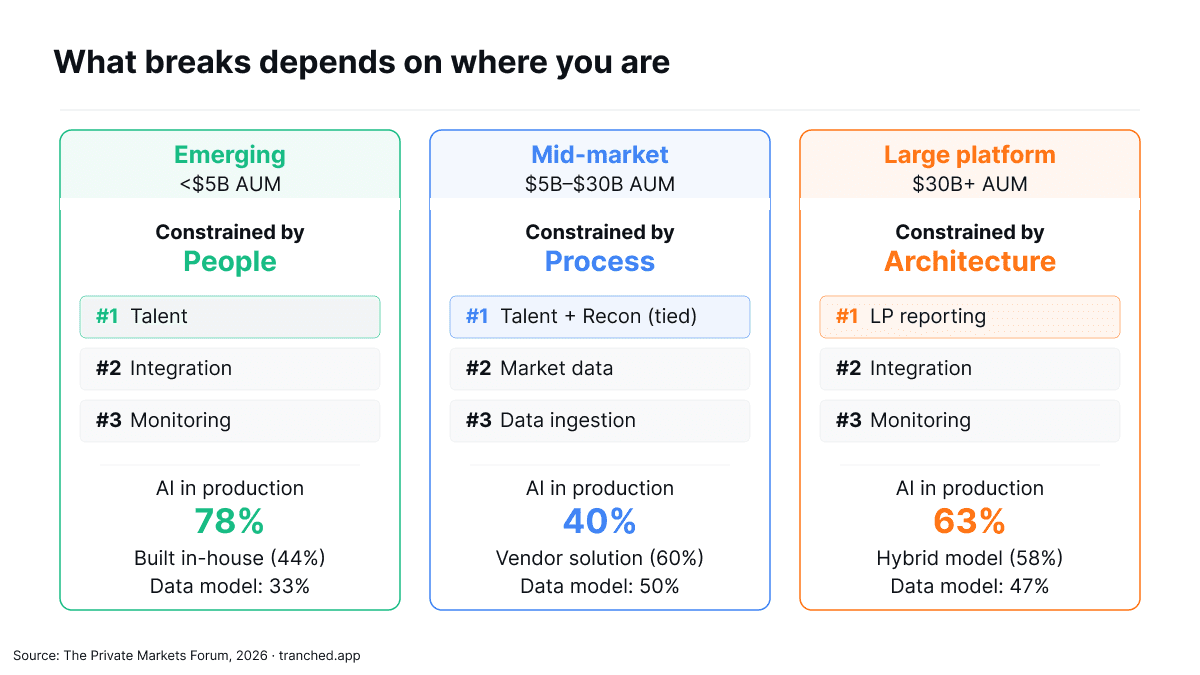

The constraints shift as firms grow. Emerging firms (under $5B) are constrained by not being able to hire people fast enough. The talent pool of professionals with both operational expertise and technology capability in private credit is thin. Mid-market firms ($5B to $30B) are past the headcount problem and into process: reconciliation breaks, data ingestion is manual, market data gaps appear as they add strategies. Large platforms ($30B+) face something structural. LP reporting and cross-system integration dominate because these firms run multiple systems across multiple strategies that were never designed to work together.

The demand for a unified data model, however, is consistent across all three tiers. 33% of emerging firms named it as their top wish. 50% of mid-market firms. 47% of large platforms. The path to get there looks different at each stage, but the destination is the same.

The Limited Partner forcing function

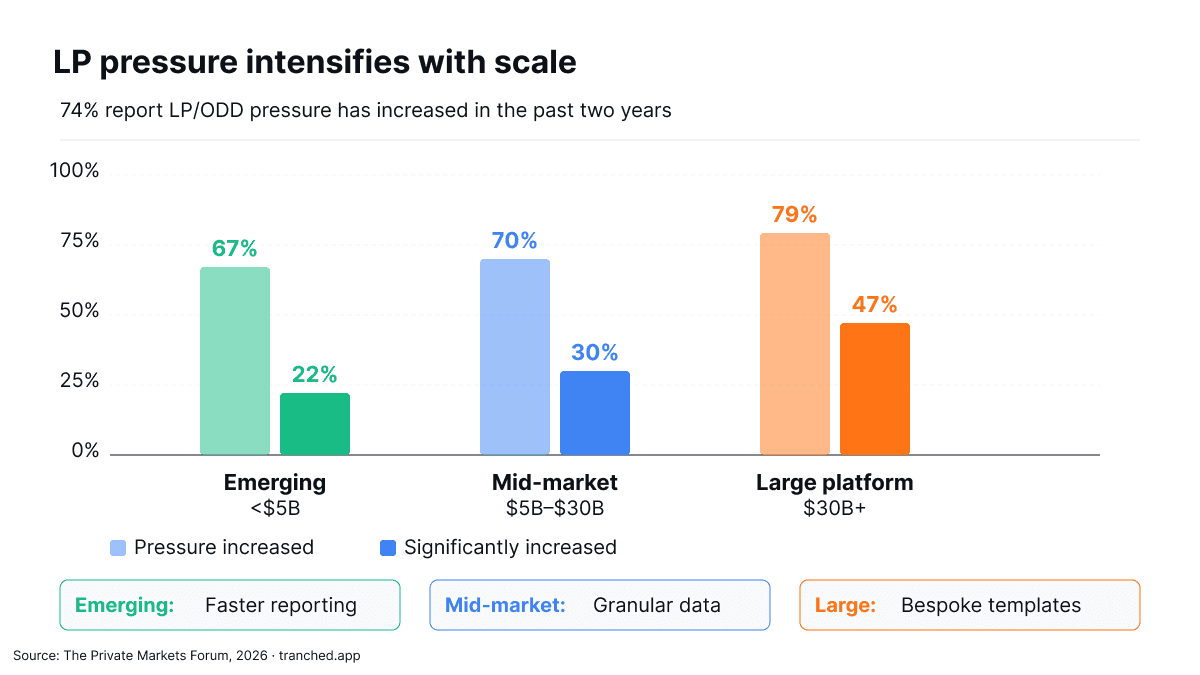

74% of respondents report that Limited Partner (LP) and operational Due Diligence (ODD) pressure has increased in the past two years. 37% describe the increase as significant. The top three demands are closely ranked: faster reporting, bespoke templates, and real-time data access.

These demands reinforce each other. LPs want reports faster, customised to their templates, with self-service access to the underlying data. Meeting all three simultaneously requires a fundamentally different data architecture than most GPs have today. GPs cannot deliver faster, bespoke, on-demand reporting without clean, normalised, continuously updated data pipelines.

The pressure intensifies with scale. Nearly half of large platforms report a significant increase in LP and ODD demands, compared to roughly one in five emerging managers. The nature of what LPs are asking for also shifts. Emerging managers face a straightforward demand: report faster. Large platforms face something more complex: deliver bespoke, real-time, self-service data access across diverse investor types. The infrastructure required to serve these two demands is fundamentally different.

One respondent captured the competitive dynamic: LPs are starting to walk with their dollars toward managers who make their lives easier. If one manager costs an LP five to ten additional FTEs just to process their data because the format is inflexible, the commitment moves elsewhere.

Another described how the pressure compounds: you promise daily NAV and real-time data room access to differentiate in fundraising, then an LP sees another manager offering the same thing, and they come back asking you to match it. The promises stack up. The infrastructure to deliver them often does not.

The distinction the market keeps getting wrong

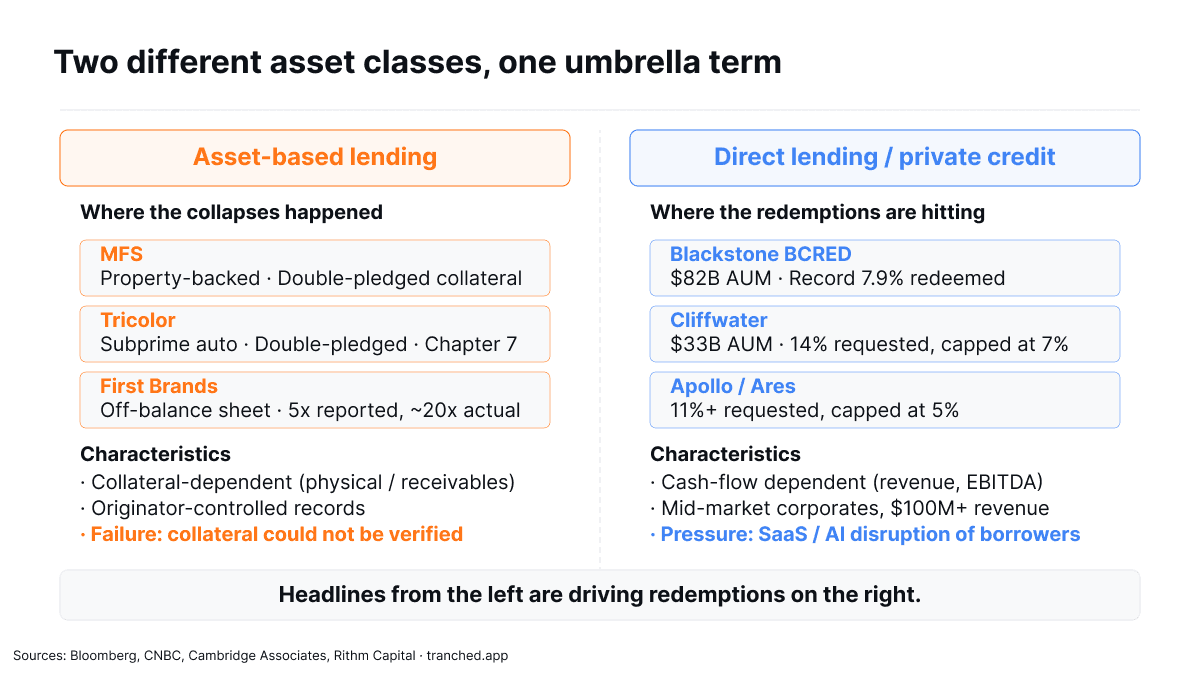

In the last several months, private credit has been the subject of sustained negative headlines. MFS collapsed with a collateral shortfall in the hundreds of millions. Tricolor Holdings filed for Chapter 7 after allegations of double-pledged loans. First Brands went from a $6B loan opportunity to bankruptcy in weeks, with off-balance sheet financing that left lenders believing they were underwriting at roughly 5x leverage when the actual figure was closer to 20x.

These are real failures. They are also, specifically, asset-based lending failures.

→ Collateral that could not be independently verified.

→ Originators who controlled the records.

→ Structures where the underlying assets were physical or receivables-based.

Rithm Capital's analysis concluded that the issue was lender control, not product complexity: lenders relied on borrower-produced borrowing base reports instead of independent data, and on registry systems that do not operate at the asset-ID level.

Cambridge Associates described both as company-specific frauds rather than systemic issues.

The funds seeing the largest redemption pressure are a fundamentally different product.

Ares and Apollo both capped withdrawals this week after investors requested more than double the quarterly limit. Blackstone allowed a record 7.9% redemption from its $82B flagship fund earlier this month. Apollo returned just 45 cents on the dollar to investors who requested withdrawals. BlackRock's HLEND fund hit its 5% redemption cap for the first time since inception. These are Business Development Companies (BDCs) and interval funds lending to mid-market corporates: companies with 500-plus employees, tens of millions in revenue, individual loans close to $100M.

The confusion comes from the fact that both asset-based lending and direct lending sit under the same "private credit" umbrella. When MFS collapses and Blackstone caps redemptions in the same quarter, the narrative writes itself. The mechanism connecting them is sentiment, not credit quality.

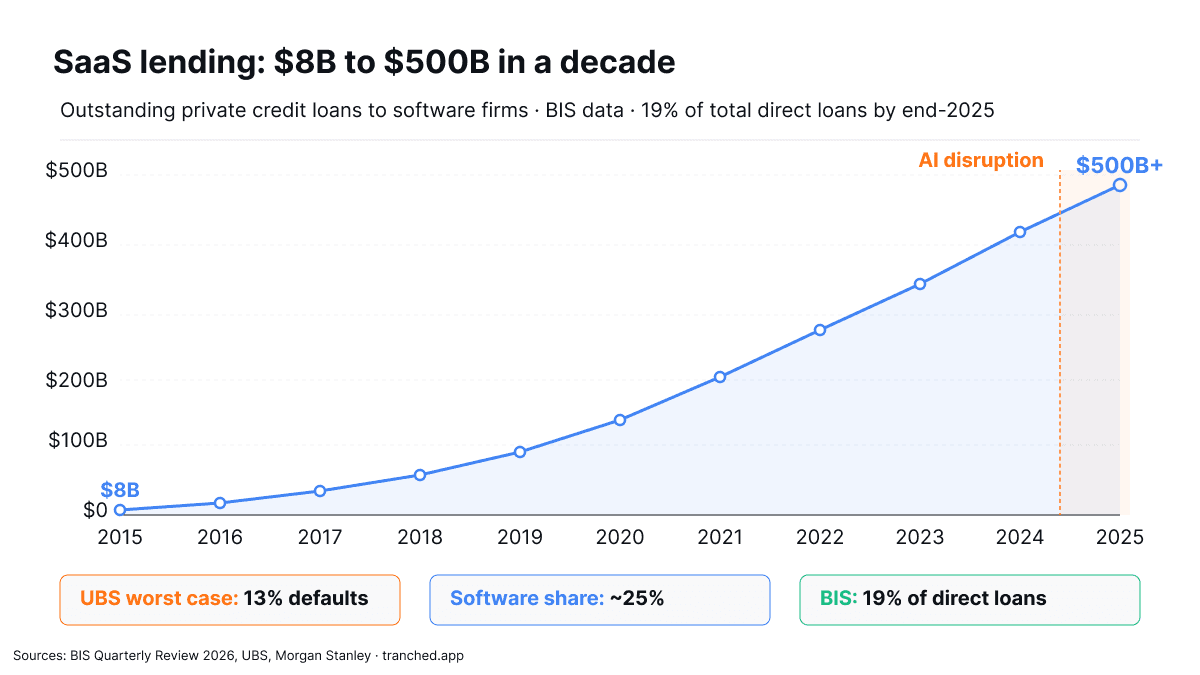

There is a real pressure point in direct lending, and it deserves attention on its own terms. BIS data shows that outstanding loans to SaaS firms increased from roughly $8B in 2015 to over $500B by end-2025, representing 19% of total direct loans.

The thesis that powered much of private credit's expansion, sticky recurring revenue from software companies, is now being tested by AI disruption. UBS has warned that in an aggressive scenario, default rates could climb to 13%. Morgan Stanley estimates software exposure in direct lending at around 26%. Apollo CEO Marc Rowan has been explicit about the concentration risk: if 30% of your portfolio is in one industry and that industry is being disrupted by technology, you have not been a good risk manager.

That is a legitimate concern creating real redemption pressure. But it is a fundamentally different concern from collateral fraud.

1️⃣ One is about whether borrowers' business models survive a technology shift.

2️⃣ The other is about whether collateral that was represented to exist actually existed.

Conflating the two makes both harder to address.

The survey data lands on this point directly. 32% of operators said the interoperability problem they most want solved is common identifiers for private credit assets. Unlike public securities with the Committee on Uniform Securities Identification Procedures (a US standard for identifying securities) (CUSIPs) or International Securities Identification Numbers (ISINs), private credit has no universal identifier. When even the data taxonomy is broken, the market's inability to distinguish ABL from direct lending at the headline level is a predictable consequence.

What good looks like

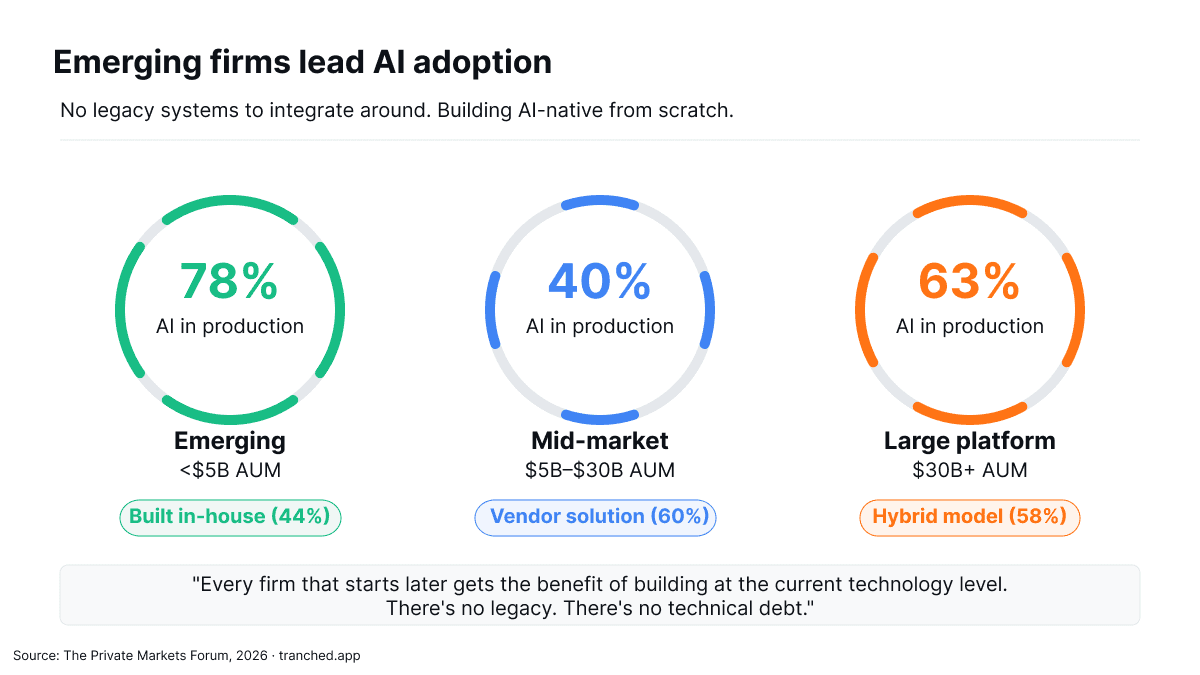

One finding cuts against the expected narrative. AI adoption does not follow a simple size gradient. 78% of emerging firms have AI in production, the highest rate in the sample, above the 63% for large platforms.

The explanation is structural. Smaller, tech-forward teams are moving faster precisely because they have no legacy to integrate around. One emerging manager drew the comparison to banking infrastructure: South Africa skipped cheques entirely and went straight to electronic transfers because they started later. The same applies to private credit firms launching today. There is no legacy. There is no technical debt. You get to start where the industry is today.

This is the principle at the centre of what Tranched is building. Loan-level data ingested and validated on-chain. Collections matched against expected ledgers automatically. Waterfall execution running deterministically from a pre-configured priority sequence. Every authorised party seeing the same state simultaneously, rather than reconstructing it from disconnected systems at quarter-end.

The survey's finding that 45% of operators want a unified data model describes infrastructure that already exists in the securitisation market. ABS has had standardised loan-level data templates, universal identifiers, trustee-verified reporting, and automated waterfall mechanics for years. Private credit has been reinventing these capabilities firm by firm, spreadsheet by spreadsheet.

The firms that solve the data model first will be the platforms that scale. The vendors that build to this need will find a market starving for solutions. And the industry standards that emerge will be the foundation on which the next generation of private credit infrastructure is built.