Stablecoins

Welcome to this week’s Tranched newsletter.

For most of the last five years, stablecoins were described as a cross-border tool. The pitch was always the same: dollars on rails, faster than SWIFT, useful for remittances, useful for FX hedging in countries where the dollar is hard to get. That description was accurate for a while. It is no longer the most useful one.

The data through Q1 2026 tells a different story. The share of stablecoin payment volume that stays inside a single country has risen from roughly half in early 2024 to nearly three-quarters by early 2026. Stablecoin velocity has roughly doubled, climbing from 2.6x to 6x over the same period, which means each dollar of supply is being used more often rather than sitting still. Adjusted Q1 2026 transfer volume reached around $4.5T, and 2025 saw $10.9T in adjusted transaction volume across the category, against Visa's $14.2T of annual payments volume.

What is happening underneath those numbers is the part most coverage is missing. Stablecoins are turning into payment infrastructure rather than dollar-bridge infrastructure. Three vectors are pulling them there at once:

Stablecoin-backed cards

Local payment - rail integrations

B2B payroll and treasury flows.

That is the mainstreaming. It is already underway.

Cards

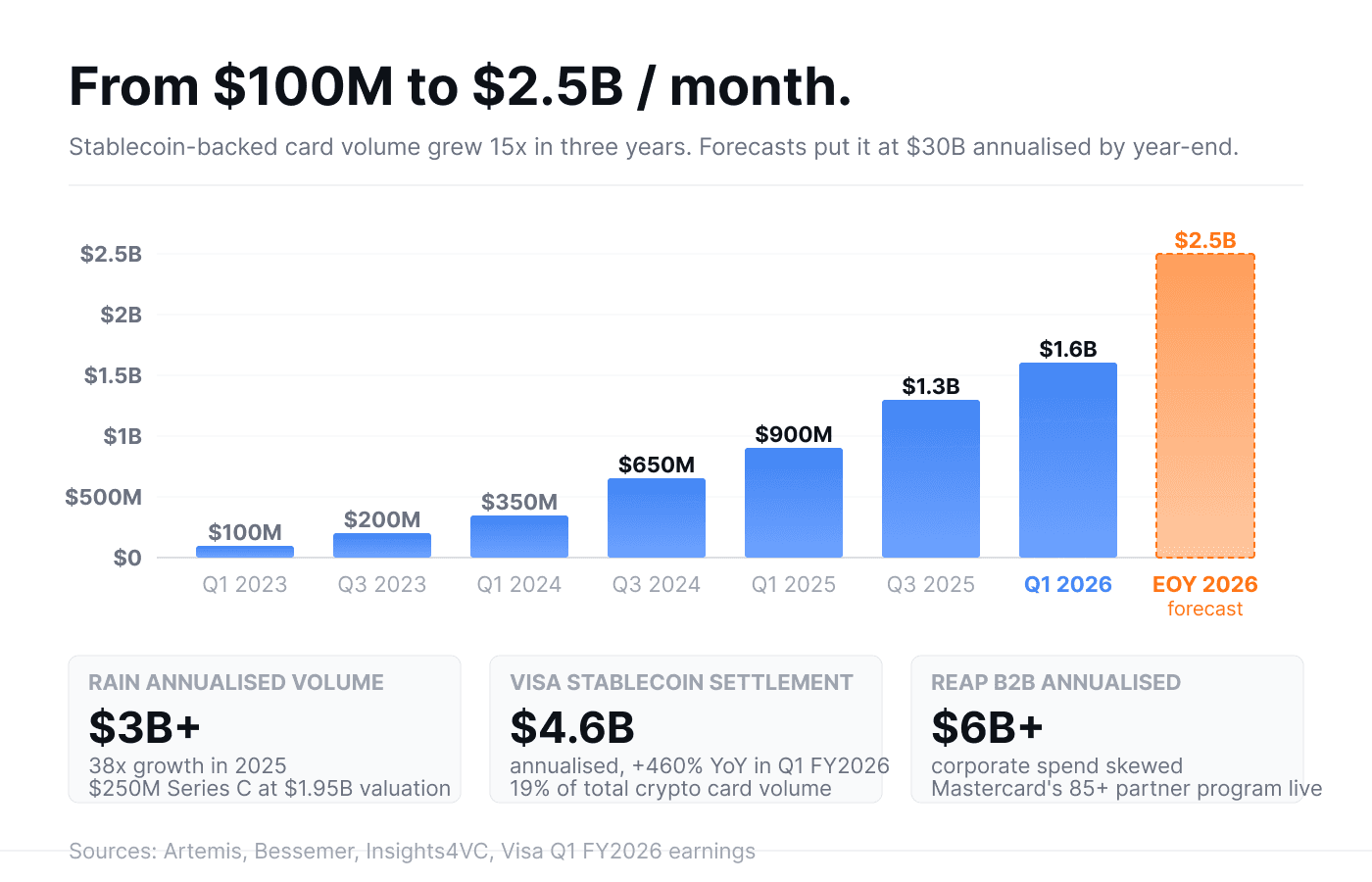

The cards segment is the cleanest proof point of the mainstreaming, and it is the one most coverage understates.

Crypto card spending has gone from roughly $100M/month in early 2023 to over $1.5B/month by late 2025, per Artemis. Annualised volume now sits at around $18B, rivalling the size of peer-to-peer stablecoin transfers ($19B), which grew just 5% over the same period. Visa's stablecoin-linked card spend reached a $4.6B annualised run rate in Q1 FY2026, up roughly 460% year-over-year. End-2026 forecasts put the category at $30B annualised, in the base case.

The growth is being driven by a small number of full-stack issuers that hold direct Visa or Mastercard membership and run the wallet, custody, conversion, and settlement layers as one. Rain is the category leader: a Visa Principal Member, ~$3B in annualised card volume after a 38x increase in 2025, $250M Series C in January at a $1.95B valuation, and an APAC expansion launching in Q2 2026. Reap, focused on B2B corporate spend, is reportedly above $6B annualised. Together they are quietly absorbing what was supposed to be the next frontier of fintech card-issuing.

The networks themselves have moved in. Visa expanded its card partnership with Stripe's Bridge to over 100 countries in March. Mastercard launched its Crypto Partner Program in March 2026 with 85+ initial members and is processing stablecoin settlement through partnerships with Circle, Paxos, and Nuvei. The Mastercard $1.8B acquisition of BVNK earlier this year was an enterprise stablecoin payroll bet wearing payments-acquirer clothing. Western Union partnered with Rain to launch stablecoin-linked cards directly into one of the world's largest remittance networks.

Most of the cards work the same way for the cardholder: a normal-looking Visa or Mastercard card that pulls from a stablecoin balance, with the conversion to local fiat happening invisibly at the point of sale. A BVNK and YouGov survey of more than 4,000 stablecoin users found 71% would use a linked debit card to spend stablecoins. The product is built. The latent demand is there. The card-network rails accept it. From a consumer perspective, this is what mainstreaming looks like in practice.

Local payment rails

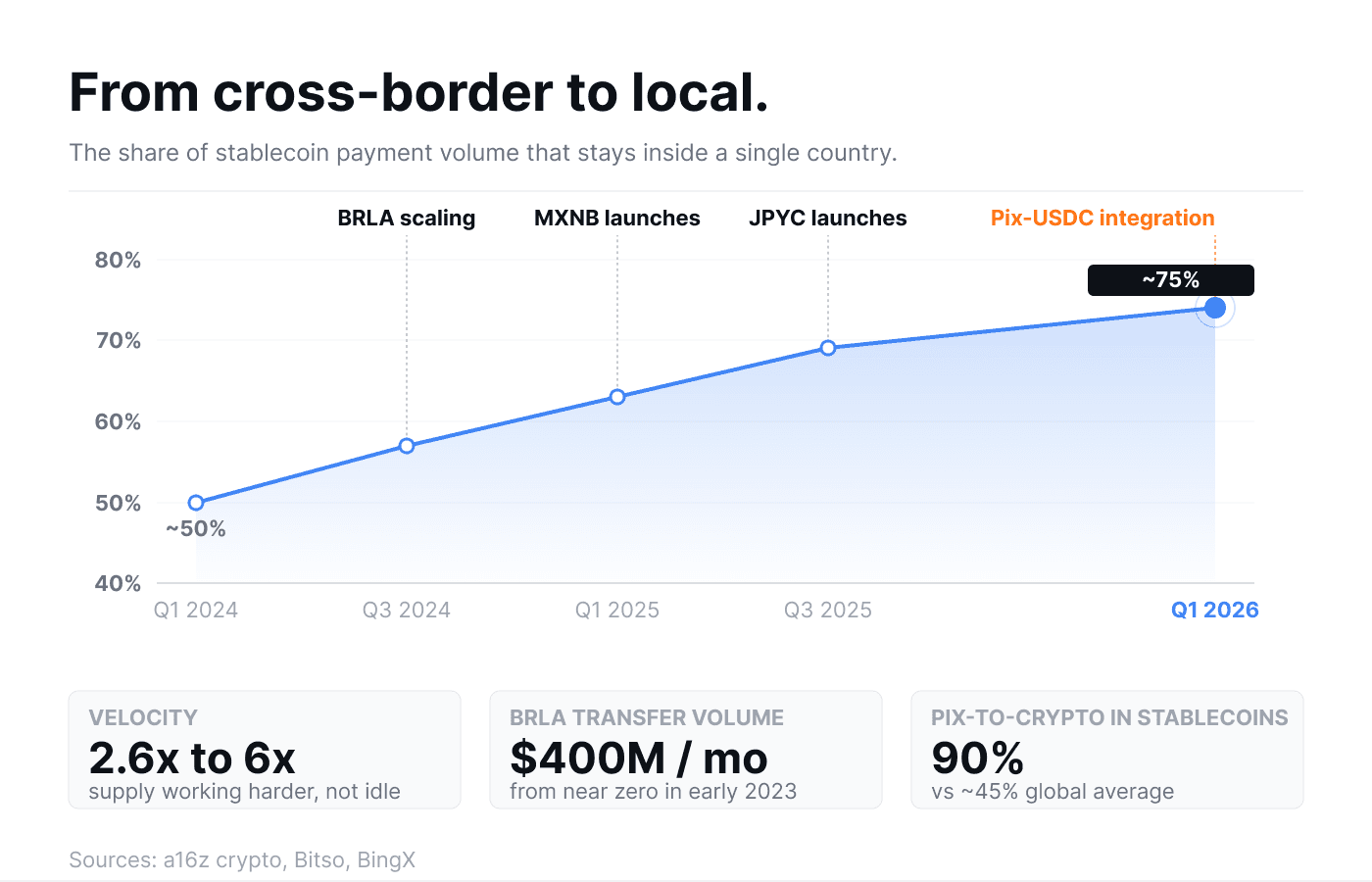

The clearest signal of the local turn is what the world's instant-payment networks have started doing. In April 2026, Brazil's central bank officially expanded Pix to support USDC, enabling licensed financial institutions to convert between BRL and the leading dollar stablecoin in real time, on the same rails Brazilians already use for billions of monthly retail transactions. The integration matters less for what it enables technically and more for what it confirms institutionally: a G20 central bank embedded a private stablecoin directly into its national payment infrastructure.

The Brazilian numbers were already striking before that. Roughly 90% of Pix-to-crypto volume flows into stablecoins, against a global average closer to 45%. Bitso processed $12B in 2024 across its enterprise rails, $6.5B of that in the US-Mexico corridor alone, more than 10% of the world's largest remittance flow. BRLA, the Brazilian-real-backed stablecoin, has grown from near zero in early 2023 to roughly $400M/month in transfer volume by early 2026.

Mexico moved the same way through SPEI. Bitso launched MXNB, a 1:1 peso-pegged stablecoin, in March 2025 with mint and redeem flows running directly through SPEI. The full BRL → USDC → MXNB hop now closes in seven to ten minutes, at spreads under 10 basis points, against the 48-hour and 40 to 65 basis point spreads typical of legacy correspondent banking.

The same pattern is showing up across other regions, each with local specifics.

Singapore has XSGD live as a payment method at Grab merchants and Alipay+ stores, with MAS running Project Orchid on top of it as a programmable money pilot.

Japan's first FSA-regulated yen stablecoin, JPYC, launched in October 2025 through the fund-transfer-service-provider licence path, with the three megabanks (MUFG, SMBC, and Mizuho) testing a joint stablecoin on the Progmat platform since November.

Across Africa, M-Pesa announced a partnership with ADI Chain in January 2026, bringing 34M existing mobile money users one integration away from on-chain stablecoin rails.

The European story is slower but no less directional. Twelve major banks including ING, UniCredit, and BBVA are backing Qivalis, a MiCA-regulated euro stablecoin targeted at H2 2026. The case for it, made by CEO Jan-Oliver Sell, is that "in the blockchain space, the euro makes up about 0.2% of transactions" against the euro's 20-25% share of global financial activity offline. The gap is the opportunity.

What ties these moves together is that they are domestic payment networks, regulated banks, and central banks themselves making stablecoins part of their existing rail. That is the kind of integration that takes infrastructure mainstream.

B2B and payroll

The third vector sits one layer up the stack and is moving the largest dollar amounts.

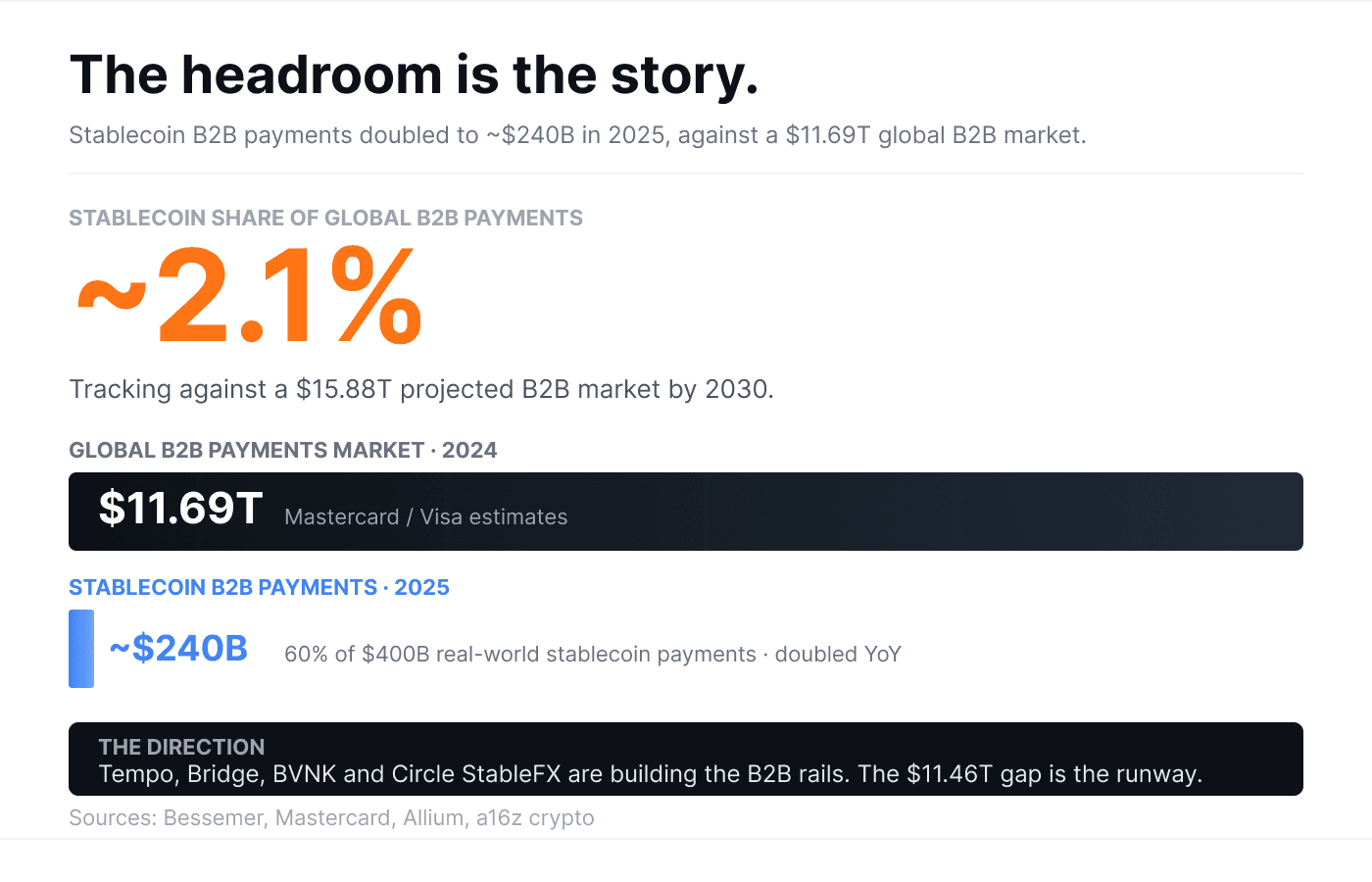

Real-world stablecoin payment volume doubled in 2025 to roughly $400B, of which around 60% was B2B. The global B2B payments market itself sits at $11.69T in 2024 and is projected to reach $15.88T by 2030, so the share of stablecoin penetration is still small. The growth rate is the relevant number.

Two structural shifts are driving it. The first is enterprise payroll and contractor disbursement. DoorDash is reportedly running stablecoin-based payouts to drivers via Stripe's Tempo chain. Anthropic, Shopify, Revolut, OpenAI and a growing list of others have signed up to use the same rails. BVNK, now Mastercard-owned, is processing enterprise stablecoin payroll at scale. Bridge, owned by Stripe, is routing contractor payouts for SaaS and marketplace businesses operating across multiple jurisdictions.

The second is treasury and FX management. Circle launched StableFX and Circle Partner Stablecoins in November 2025 on its Arc layer-1, onboarding eight initial regional issuers (Avenia for BRLA, Forte fobr AUDF, JPYC, Juno for MXNB, BDACS for KRW1, Stablecorp for QCAD, ZAR Universal Network for ZARU, and Coins.ph for PHPC) and pitching the combination as a 24/7 institutional FX engine.

The testnet participants alone include BlackRock, Visa, Goldman Sachs, Deutsche Bank, Standard Chartered, BNY, State Street, ICE, AWS, Cloudflare, and Mastercard. Stripe's Tempo is competing for the same workflow with a different design philosophy. Better Money, the clearinghouse founded by former a16z investor Sam Broner, raised $10M in March to address the same problem at a different layer of the stack: making one stablecoin actually exchangeable for another at par.

The pattern across all three of these is the same. The infrastructure is being built by companies the existing financial system already does business with, on rails the existing financial system already integrates. Tether is building Stable, a USDT-dedicated chain. Visa, Stripe, and Standard Chartered are running validators on payment chains that, in 2019, the US government sent threatening letters to companies for considering joining. The institutional posture has reversed.

What it adds up to

A category that does $4.5T in adjusted quarterly volume, settles $4.6B annualised through Visa, has a central bank plugged into one of its tokens, and is being adopted by Western Union, Mastercard, BlackRock, and DoorDash is no longer reasonably described as crypto. It is a payments infrastructure that runs on a different settlement substrate.

The local turn is what makes this mainstreaming possible.

Cross-border stablecoin volume continues to grow, but the structural break is that intra-country use grew faster, which means the product is being used as money rather than as a remittance vehicle.

Velocity doubling tells the same story, alongside the cards segment crossing $18B annualised on rails the existing card networks already control and the BRLA, MXNB, JPYC, XSGD, and KRW1 issuers being onboarded onto the same FX engine alongside USDC. The shape of the system, two years out, is a payment network where local stablecoins handle local rails and dollar stablecoins handle the global hub, with FX engines and clearinghouses in the middle to keep things at par.

The card growth is the most obvious tell of the mainstreaming, and it is also the most obvious tell of what hasn't happened yet. Visa and Mastercard are settling some of those transactions in stablecoins behind the scenes, but the merchant on the other end is still receiving local fiat. The full loop, where a consumer holds stablecoin, taps a card, the merchant settles in stablecoin, and the merchant pays a supplier in stablecoin, is still mostly a pilot. Until the acceptance side closes, stablecoins remain a more efficient way to fund dollar-denominated card spend in places where dollar access carries friction. That is meaningful. It is also not the end state.

The shape of what comes next is becoming clearer in another way as well. Each new stablecoin that joins the system, and there are now hundreds, is another reserve pool that has to remain genuinely 1:1 backed for the rails above it to keep working. As the category crosses $300B in float and approaches Visa's annual payment volume, the layer underneath that confirms one stablecoin is one of its referenced fiat unit, continuously, at every level of the stack, becomes systemic infrastructure rather than a periodic disclosure. Not because it is failing today, but because the cost of it failing tomorrow is no longer contained to the category.

The mainstreaming has happened. The plumbing for what mainstream actually means is the next thing to build.