Tokenisation

Welcome to this week’s Tranched newsletter.

Last week, three of the largest institutions in global finance said that tokenisation has moved from pilot to production. The week before, Grayscale called it a $300T megatrend. The financial press has covered this as a moment of arrival.

This week, we delve into a brief history of what tokenisation actually is, and why this time, the wrapper finally compounds.

Last week, Citi's Ryan Rugg, speaking at Consensus 2026, told the room that the bank's tokenised deposit platform had moved from handling "millions" twelve months ago to "billions" today. JPMorgan's Kara Kennedy noted that Kinexys, the bank's blockchain platform, had just crossed $1T in cumulative transactions. And DTCC's Nadine Chakar, sitting between them, confirmed that DTC's tokenisation service, built with feedback from over 50 financial firms, would launch in October.

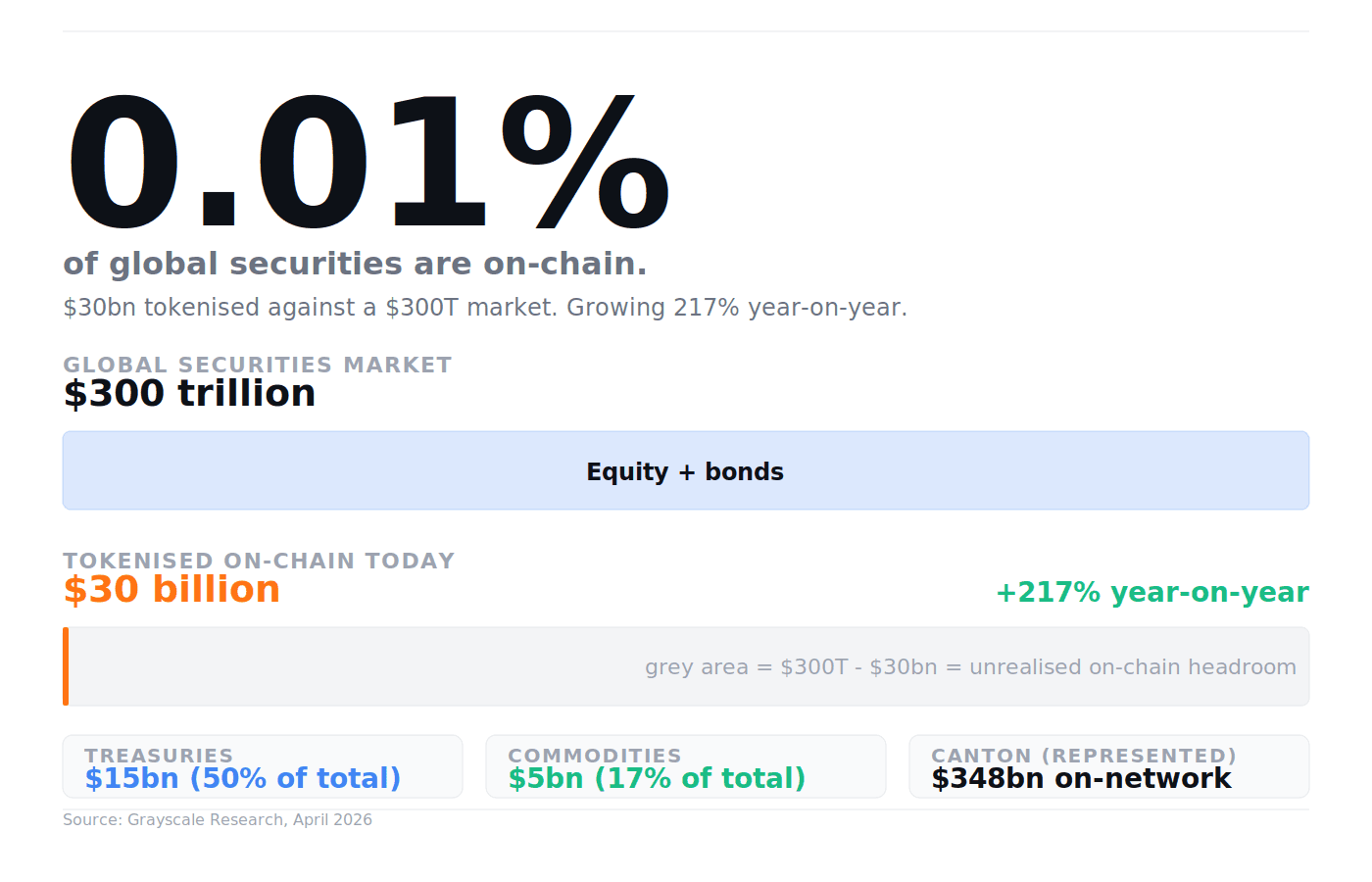

The week before, Grayscale Research published Investing in the Tokenization Megatrend, naming six protocols it expects to anchor the shift and projecting that "much of the ~$300T securities market" will eventually migrate on-chain. Today, $30B of assets are tokenised, about 0.01% of that universe. The growth rate, per Grayscale, is 217% year-on-year.

The financial press has covered this as a moment of arrival. It is more accurate to call it a moment of convergence.

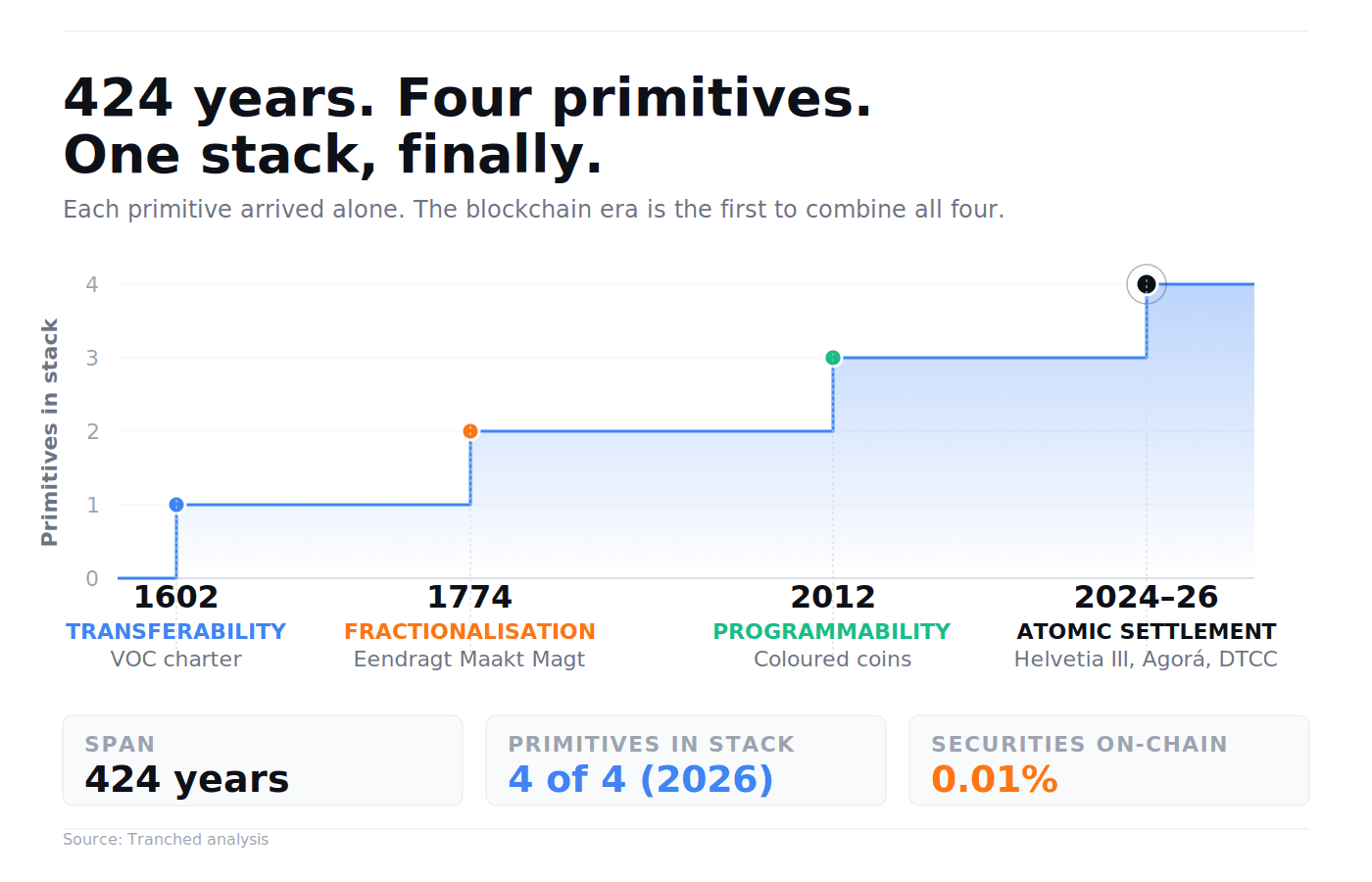

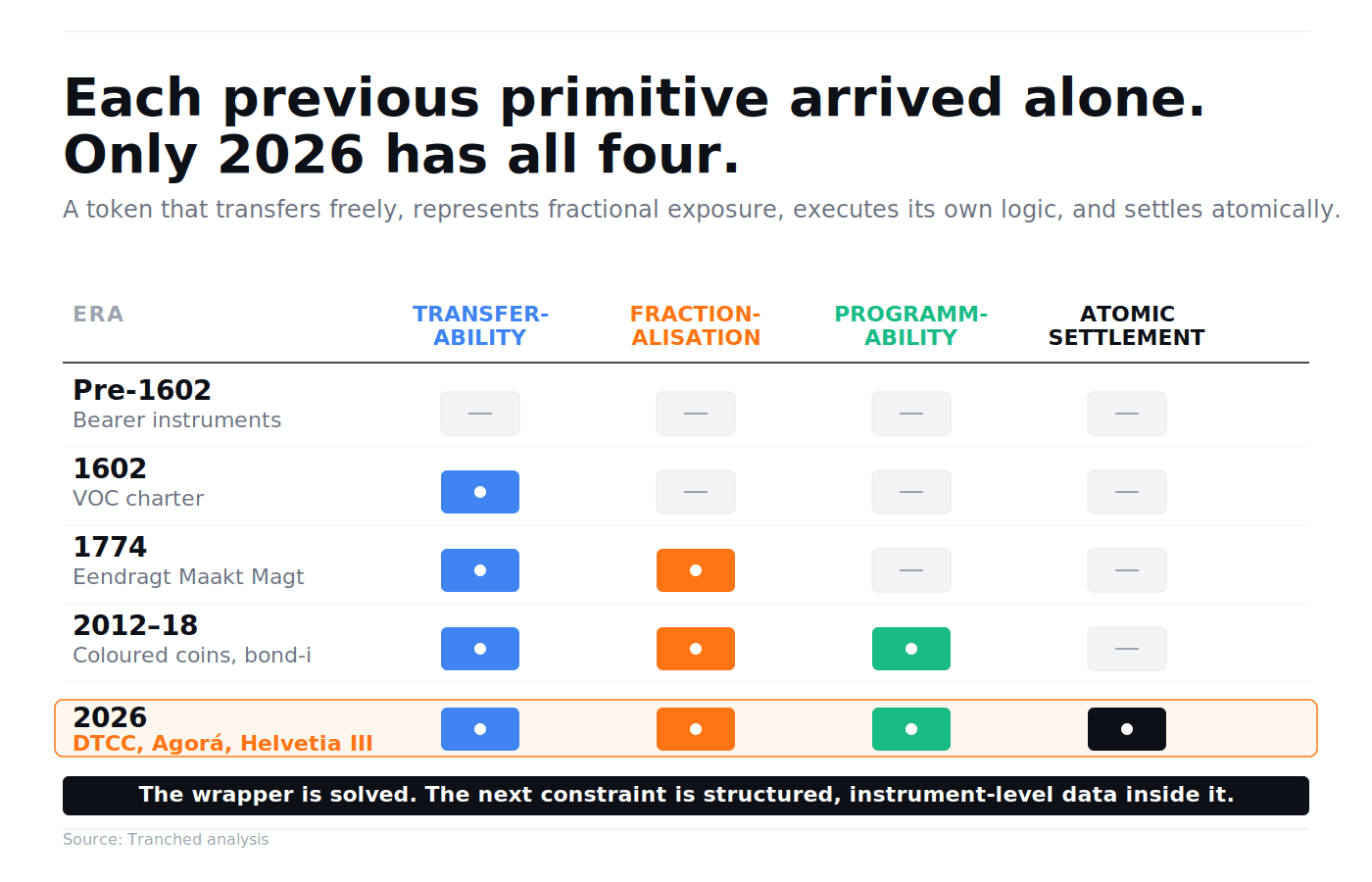

Tokenisation, the issuance of a transferable claim that represents an underlying asset, was not invented by Ethereum, by bond-i, or by Mastercoin. It was invented in Amsterdam, in 1602, and the 424 years since have been a slow accumulation of four specific primitives. The blockchain era is the first to combine all four at once.

Primitive 1: Transferability (1602)

The Vereenigde Oostindische Compagnie was chartered on 20 March 1602 with a 21-year monopoly over Asian trade. Article 10 of its founding document made the move that mattered: "All the residents of these lands may buy shares in this Company." In August, 1,143 investors subscribed to the first IPO in history, contributing 6.4M guilders.

The novelty was not that ordinary citizens could fund a venture. Dutch voorcompagnieën had pooled merchant capital for decades. The novelty was structural. VOC shares were entered on a registry held by the company's chambers; transferring ownership required both parties to appear in person before two directors, who recorded the change in the books. The asset, the ships, the warehouses, the Banda nutmeg, stayed where it was. The claim moved.

Within months, shareholders were trading those claims at the Hendrick de Keyser Exchange. The asset was illiquid; the token was not. Gelderblom, de Jong and Jonker, in the Journal of Economic History, describe this as the foundational corporate-form innovation: legal personhood, permanent capital, freely transferable shares. In tokenisation terms, it is the foundational primitive: a registered claim that moves independently of what it represents.

Primitive 2: Fractionalisation (1774)

A century and a half later, Abraham van Ketwich, an Amsterdam broker, issued Eendragt Maakt Magt, "unity makes strength." It was the world's first closed-end fund. Two thousand actiën at 500 guilders each, each one a transferable claim on a diversified basket: Russian sovereign debt, Danish toll revenues, plantation loans in Essequibo and Berbice, equity in American bridge and toll companies. The investor bought one piece of paper and got fractional exposure to the entire portfolio.

This is the second tokenisation primitive: pooled exposure, divided into transferable units. It is the conceptual ancestor of every tokenised fund issued since, including BlackRock's BUIDL, which today holds tokenised T-bills on the same logic, in a permissioned smart contract instead of a Dutch ledger book.

The cautionary tail came earlier and louder. From 1753, Dutch merchant bankers had been floating negotiatie: pooled mortgages on Caribbean and Surinamese plantations, collateralised by the land, the equipment, and, terribly, the enslaved labour those plantations ran on. By 1770, bundles were being issued under names as opaque as "L.a. A, B, or C." Investors had little idea what they owned. In December 1772, Clifford & Co, one of Amsterdam's largest plantation-loan houses, failed; the credit crunch tore through the Dutch West Indies, plantations defaulted, and bundle valuations collapsed.

Goetzmann and Newman, in their NBER working paper Securitization in the 1920s, document a near-identical pattern 150 years later: real estate bonds reached 23% of all US corporate debt issued in 1925, with $4.1B raised across 1,090 offerings. Retail bought eagerly. Issuance fell to 0.14% of corporate debt by the early 1930s. The collateral cycle broke before the equity market did.

The lesson, repeated twice across two centuries: fractionalisation without data discipline ends the same way every time.

Primitive 3: Programmability (2012)

Skip forward to a blog post. In March 2012, Yoni Assia, then chief executive of eToro, wrote up an idea he was calling "coloured coins": tagging individual satoshis on the Bitcoin blockchain with metadata to represent something other than bitcoin. A share. A bond. A deed. A loyalty point. On 4 December 2012, Meni Rosenfeld, then president of the Israeli Bitcoin Association, published the whitepaper that formalised the concept.

What coloured coins added was not a registry. VOC chambers had registries. Nor divisibility, which Van Ketwich had solved. They added logic. The token could now do things. It could enforce a transfer restriction, execute a coupon payment, check a counterparty against a whitelist, redeem itself on a date. The third primitive is programmability: a claim that runs code.

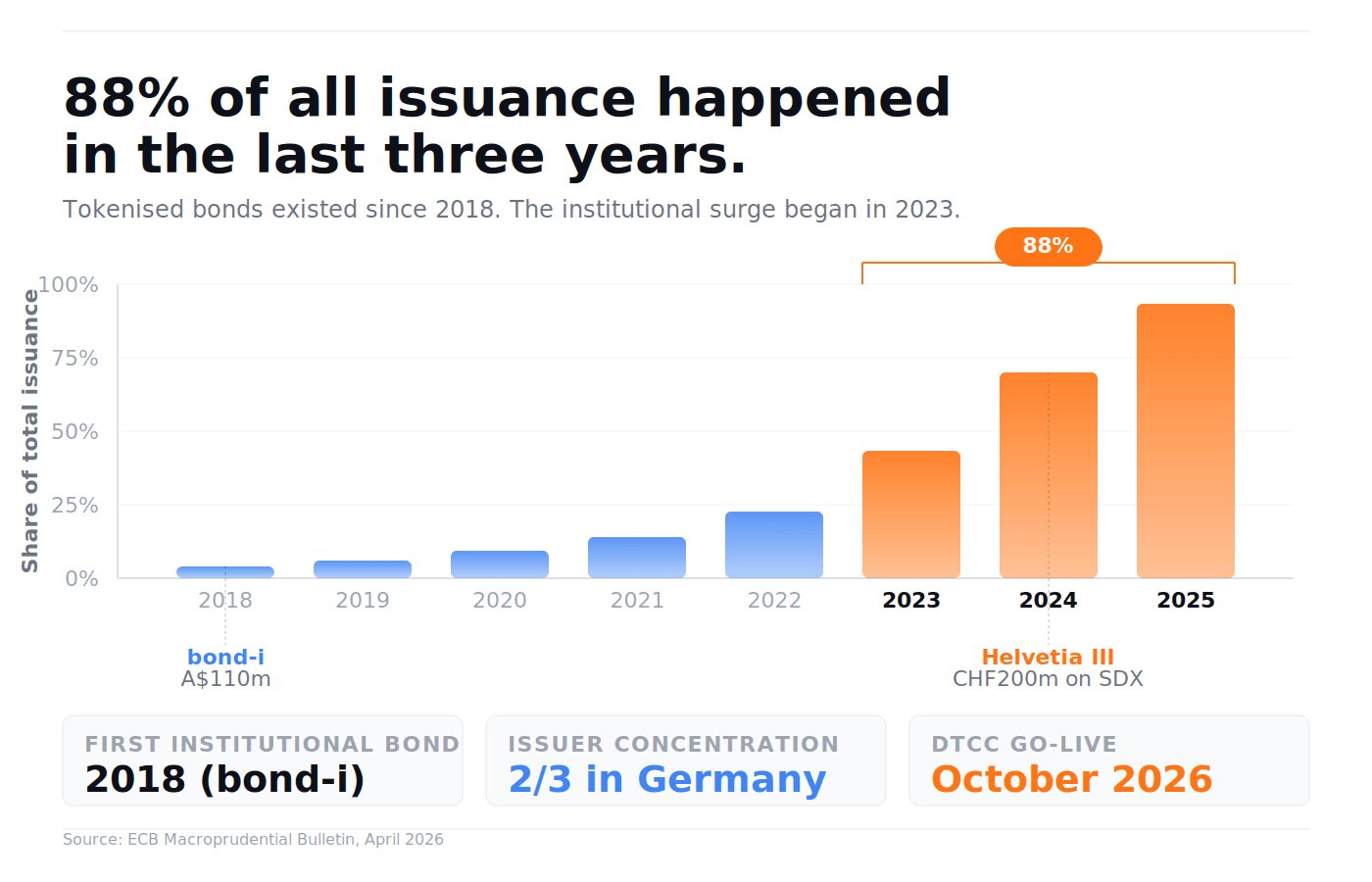

The early experiments are quietly strange. In June 2014, Counterparty, a protocol layered on Bitcoin, minted OLGA, one of the first NFTs; it ostensibly contained an image, though no one is now sure of what. Realcoin, later renamed Tether, launched on Mastercoin/Omni in October 2014: the first dollar-pegged stablecoin, today a market in the hundreds of billions. In August 2018, the World Bank issued bond-i, a A$110M two-year Kangaroo bond whose entire lifecycle (issuance, allocation, transfer, redemption) was managed on a blockchain platform built by Commonwealth Bank of Australia. It is widely regarded as the first institutional tokenised bond.

This is also the era in which the architecture bifurcated. Grayscale's report identifies the split clearly: open networks like Ethereum and Solana, where tokenised assets coexist with permissionless DeFi protocols, versus institution-centric networks like Canton and Provenance, where privacy and identity are built in. The six protocols Grayscale names (Ethereum, Solana, Canton, Avalanche, BNB Chain, and Chainlink) sit on different points of that spectrum. They are not competing for the same role.

Primitive 4: Atomic Settlement (2024–2026)

The fourth primitive is the one institutions have spent the longest building toward. In a tokenised world, the asset moves on one ledger and the payment on another, unless they move on the same ledger, simultaneously, and only if both legs succeed. That is atomic delivery-versus-payment. It collapses messaging, reconciliation, and settlement into a single conditional operation.

Project Helvetia III, run by the Swiss National Bank and the BIS Innovation Hub, demonstrated it at scale in 2024 when the World Bank issued a CHF200M digital bond on SIX Digital Exchange, settled in tokenised wholesale central bank money.

The BIS, in Chapter III of its 2025 Annual Economic Report, made the architectural argument: a "unified ledger" combining tokenised central bank reserves, tokenised commercial bank money, and tokenised government bonds. Project Agorá, led by the BIS with seven central banks (including the Fed, ECB, Bank of England, and Bank of Japan) and over 40 private institutions, has been in testing since January, with a full report expected by mid-2026. In April 2026, the IMF's Tobias Adrian published Note 2026/001, framing tokenised deposits not as an experiment but as a structural addition to the monetary system.

What changed in the last six months is the production data. Citi's tokenised deposit volumes have moved an order of magnitude. JPMorgan's Kinexys has crossed $1T cumulative. The DTCC, which custodies over $114T of US securities, plans to begin tokenised production trades in July under the SEC's December 2025 No-Action Letter, with the full service launching in October. The ECB's April 2026 Macroprudential Bulletin confirms the trajectory in the bond market specifically: 88% of all tokenised bond issuance has occurred in the last three years.

Grayscale's numbers fill in the rest. Total tokenised assets stand at roughly $30B, with Treasuries leading at $15B and commodities at $5B. Canton, the institution-centric network backed by DRW, Goldman Sachs, Nasdaq, and Tradeweb, hosts $348B in represented asset value. Ethereum leads open-network distributed assets at $16B. The 217% growth rate is real, and so is the 0.01% number. Both can be true at the same time. The market is small and accelerating.

The Convergence

Each previous primitive arrived alone. The VOC had transferability but no fractionalisation; the negotiatie had pooled exposure but no programmability; coloured coins had logic but no settlement infrastructure. The blockchain era is the first in which all four primitives sit in the same stack: a token that transfers freely, represents fractional exposure to a pool, executes its own logic, and settles atomically against tokenised cash on a unified ledger.

This is why Grayscale's $300T projection is directional rather than speculative. The technical conditions for the migration of capital markets on-chain are present for the first time in 424 years. The DTCC launch in October, the Project Agorá report in mid-2026, the production volumes at Citi and JPMorgan: these are the institutional infrastructure of the next system being assembled in public.

The constraint, on Tranched's reading, has shifted. The wrapper is now the solved problem. What determines whether on-chain capital markets compound to $300B or $300T is the data layer beneath it.

Every previous tokenisation wave broke the same way: when retail investors, professional allocators, or rating agencies could no longer see what was inside the package, prices stopped reflecting fundamentals and the structure unwound. Negotiatie in 1772, real estate bonds in 1929, MBS in 2008. The wrapper was never the problem.

The four primitives have finally arrived. Whether the fifth wave compounds or repeats is a question about structured, instrument-level data (covenants, cash flows, defaults, recoveries), rendered as cleanly on-chain as the tokens that wrap them.

That is the build that comes next.