Blockchain

Welcome to this week’s Tranched newsletter.

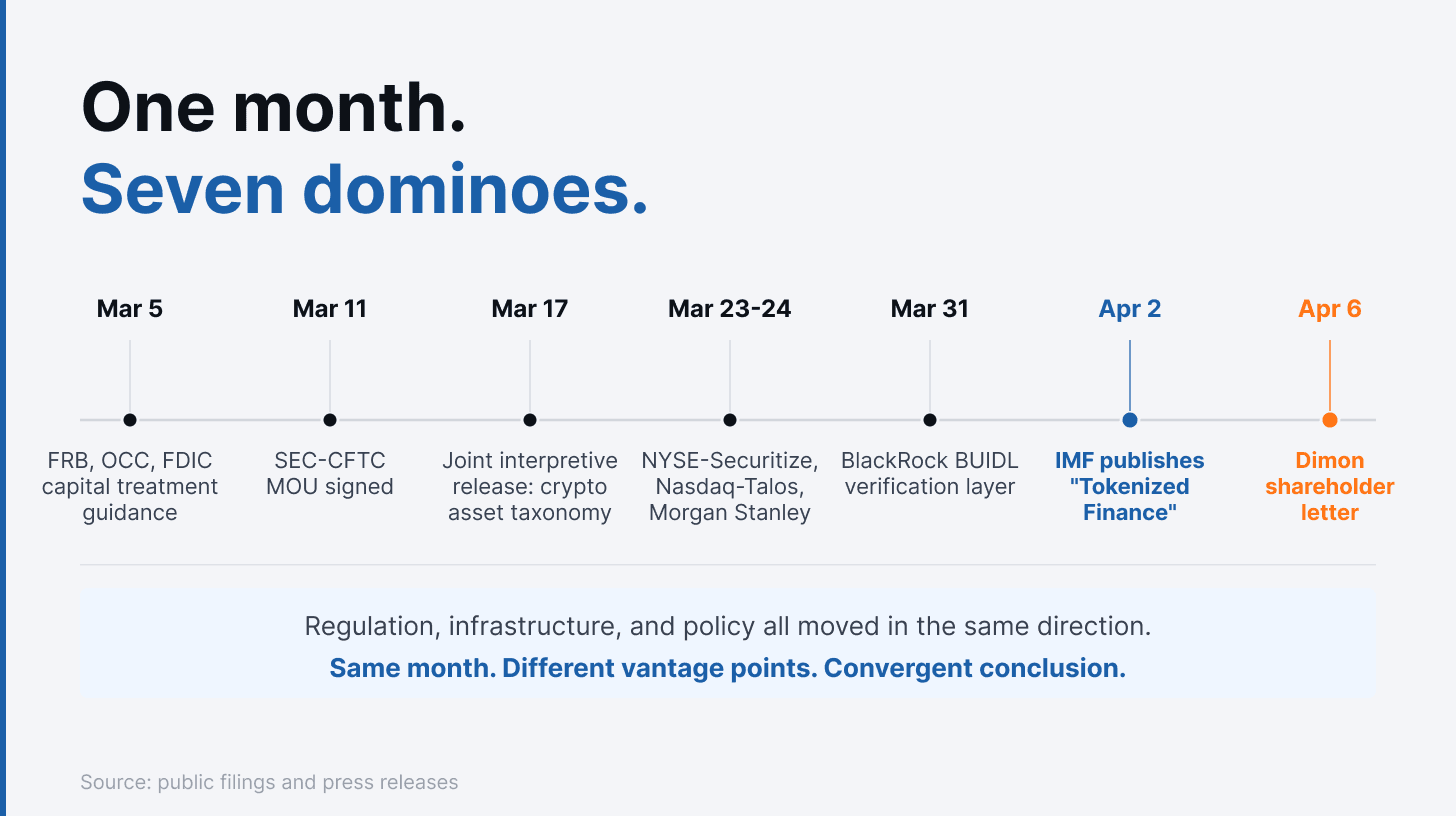

In the span of a single month, U.S. banking regulators clarified capital treatment for tokenised securities, the SEC and CFTC issued their first joint crypto taxonomy, three of Wall Street's largest institutions announced tokenised trading platforms, and the IMF published its most definitive statement yet on the future of digital finance.

The settlement layer is being rebuilt. The regulatory layer is catching up. This week, we ask what is happening inside the transactions themselves, where waterfall distributions, borrowing bases, and eligibility tests still run on spreadsheets and conflicted intermediaries.

On April 6, JPMorgan published its 2025 Annual Report. In it, Jamie Dimon told shareholders that "a whole new set of competitors is emerging based on blockchain, which includes stablecoins, smart contracts and other forms of tokenisation." He added that these technologies "may change the fundamental nature of how all this is done." His prescription: "We need to roll out our own blockchain technology and continually focus on what our customers want."

Four days earlier, the International Monetary Fund (IMF) published Tokenized Finance, a note authored by Tobias Adrian, its Financial Counsellor and Director of the Monetary and Capital Markets Department. The argument was blunt: tokenisation is a structural reallocation of trust within the financial system, not an efficiency gain at the margin. The report described a world in which execution, settlement, and risk management migrate from institutions to infrastructure and programmable logic, with significant consequences for liquidity, governance, and the stability of the financial system itself.

Same week. Different vantage points. Convergent conclusion.

The settlement layer is being rebuilt. The regulatory layer is catching up. But inside the transactions themselves, in the waterfalls, the borrowing bases, the eligibility tests, the operational layer remains largely untouched.

The Scoreboard

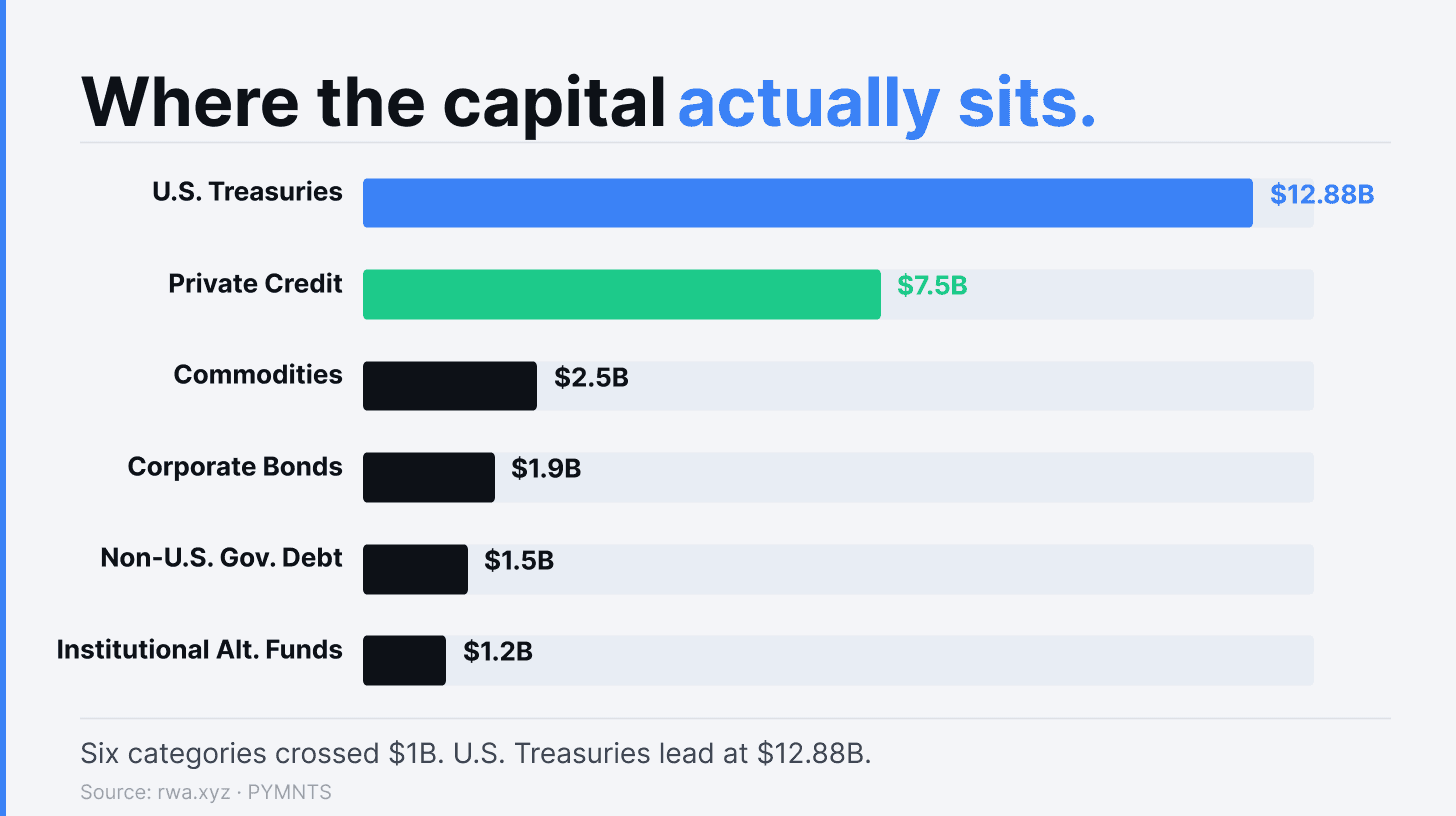

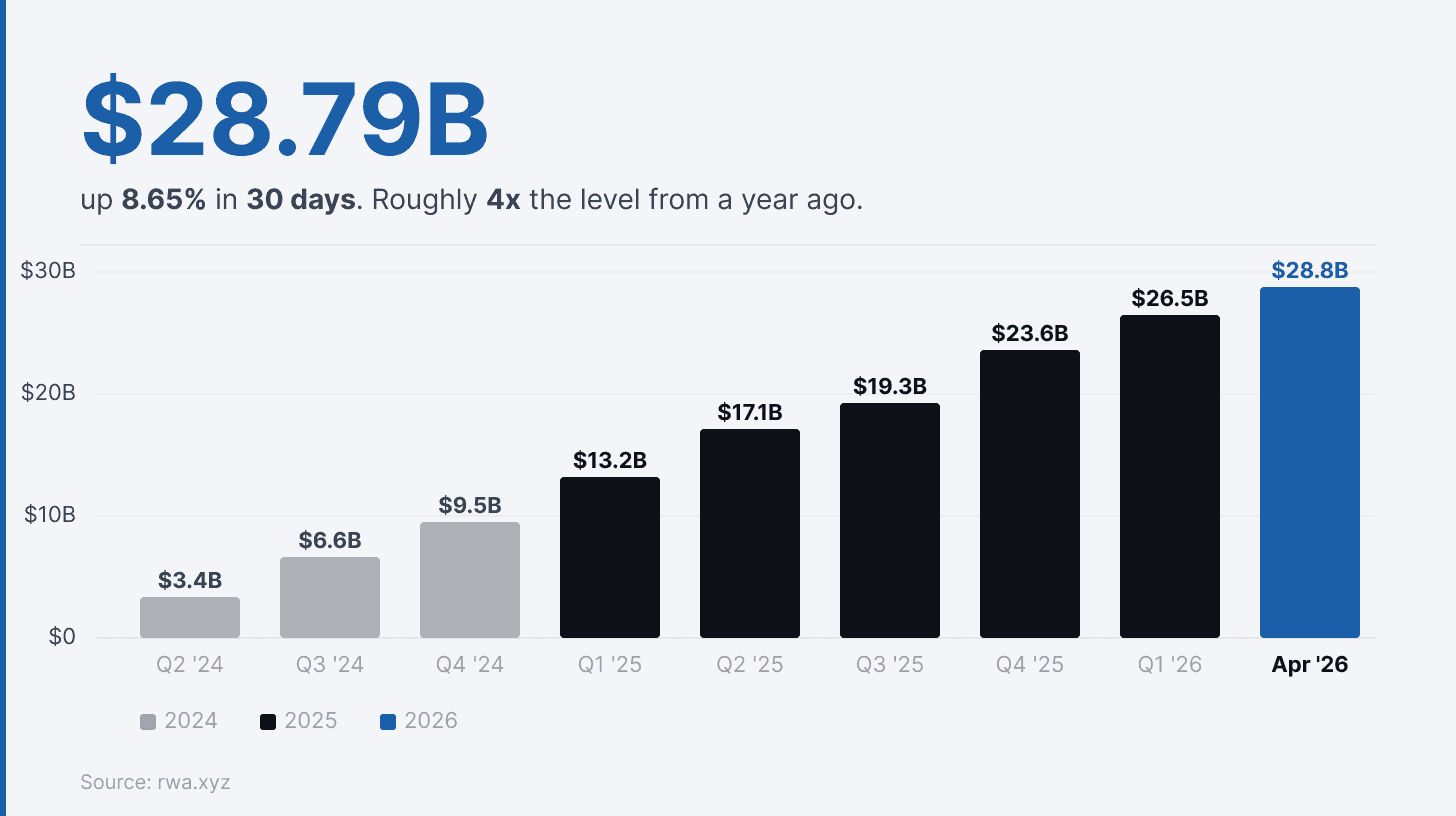

The numbers behind these statements are moving quickly. As of April 8, tokenised real-world assets have reached $28.79B in distributed on-chain value, up 8.65% in the past 30 days alone, and roughly 4x the level from a year ago. Six asset classes have now crossed the $1B mark: private credit, commodities, U.S. Treasuries, corporate bonds, non-U.S. government debt, and institutional alternative funds. U.S. Treasuries remain the largest single category at approximately $12.88B.

The institutional buildout is keeping pace.

→ The New York Stock Exchange (NYSE) signed an Memorandum of Understanding (MOU) with Securitize to develop a blockchain-native securities platform, naming Securitize the first digital transfer agent eligible to mint tokenised stocks and ETFs for corporate issuers.

→ Nasdaq partnered with Talos to integrate tokenised collateral management into its Calypso platform, targeting over $35B in excess collateral currently trapped in non-interest-bearing measures.

→ Morgan Stanley announced it will enable tokenised stock trading on its internal dark pool, "Trajectory Cross," by the second half of 2026, describing it as "a natural path forward."

→ BlackRock's BUIDL fund, the largest tokenised Treasury vehicle with approximately $1.7B under management, added Chronicle's Proof of Asset system: an independent verification layer attesting to the composition, valuation, and custody of the fund's underlying assets.

The Governance Question

The macro picture is clear enough. What is less discussed, and what the IMF's April report goes furthest in articulating, is the governance layer that needs to accompany this infrastructure.

The IMF's core observation is that traditional financial systems rely on temporal buffers: end-of-day settlement, batch processing, delayed reconciliation. These frictions are expensive and slow, but they also provide time: for exposures to be netted, for liquidity to be mobilised, and for authorities to intervene before settlement becomes final. Tokenised systems compress or eliminate these buffers entirely.

→ Settlement becomes continuous.

→ Margining becomes automated.

→ Liquidity demands materialise instantaneously.

The report frames the policy challenge around five pillars: anchor settlement in safe money, implement global standards, ensure legal certainty, promote interoperability, and adapt crisis management frameworks.

But embedded within it is a more specific argument about the governance of code itself. When trading, settlement, custody, and compliance are embedded in programmable logic, the IMF argues, "supervision must extend beyond market participants to the design, governance, and resilience of market infrastructures themselves." Failures can originate in smart contracts, data feeds, or consensus mechanisms, rather than firm balance sheets.

The U.S. regulatory apparatus has been moving quickly. On March 5, the Federal Reserve Board (FRB), Office of the Comptroller of the Currency (OCC), and (Federal Deposit Insurance Corporation) FDIC jointly clarified that tokenised securities receive the same capital treatment as their non-tokenised equivalents, removing a significant source of uncertainty for banks evaluating adoption. On March 17, the Securities and Exchange Commission (SEC) and Commodity Futures Trading Commission (CFTC) issued a joint interpretive release, their first major coordinated statement, establishing a five-category taxonomy for crypto assets and confirming that a security remains a security regardless of whether it is issued on-chain or off.

These are significant steps. They address the settlement layer, the classification layer, and the capital layer. What they do not yet address in depth is the operational layer: what happens inside a transaction once it is live, funded, and running.

Inside the Transaction

This is where the conversation gets quieter, and more consequential.

In structured credit (European ABS, Collateralised Loan Obligations (CLOs), private credit facilities) there is a role that sits at the centre of every reporting date: the calculation agent.

Waterfall distributions, borrowing base certificates, advance rate determinations, eligibility testing: these outputs directly determine how much capital a lender releases and how much cash flows to equity. The role exists precisely because different parties in a transaction have different economic interests, and someone needs to do the maths from a position of neutrality.

In practice, that neutrality is often structural fiction. As a recent Finextra analysis observed, when a law firm acts as calculation agent, it is typically also transaction counsel. When an accountant does it, they often audit the same vehicle. The independent party certifying your cash flows is rarely independent at all. This is not a matter of dishonesty; it is a matter of commercial entanglement that has become so normalised that almost nobody questions it.

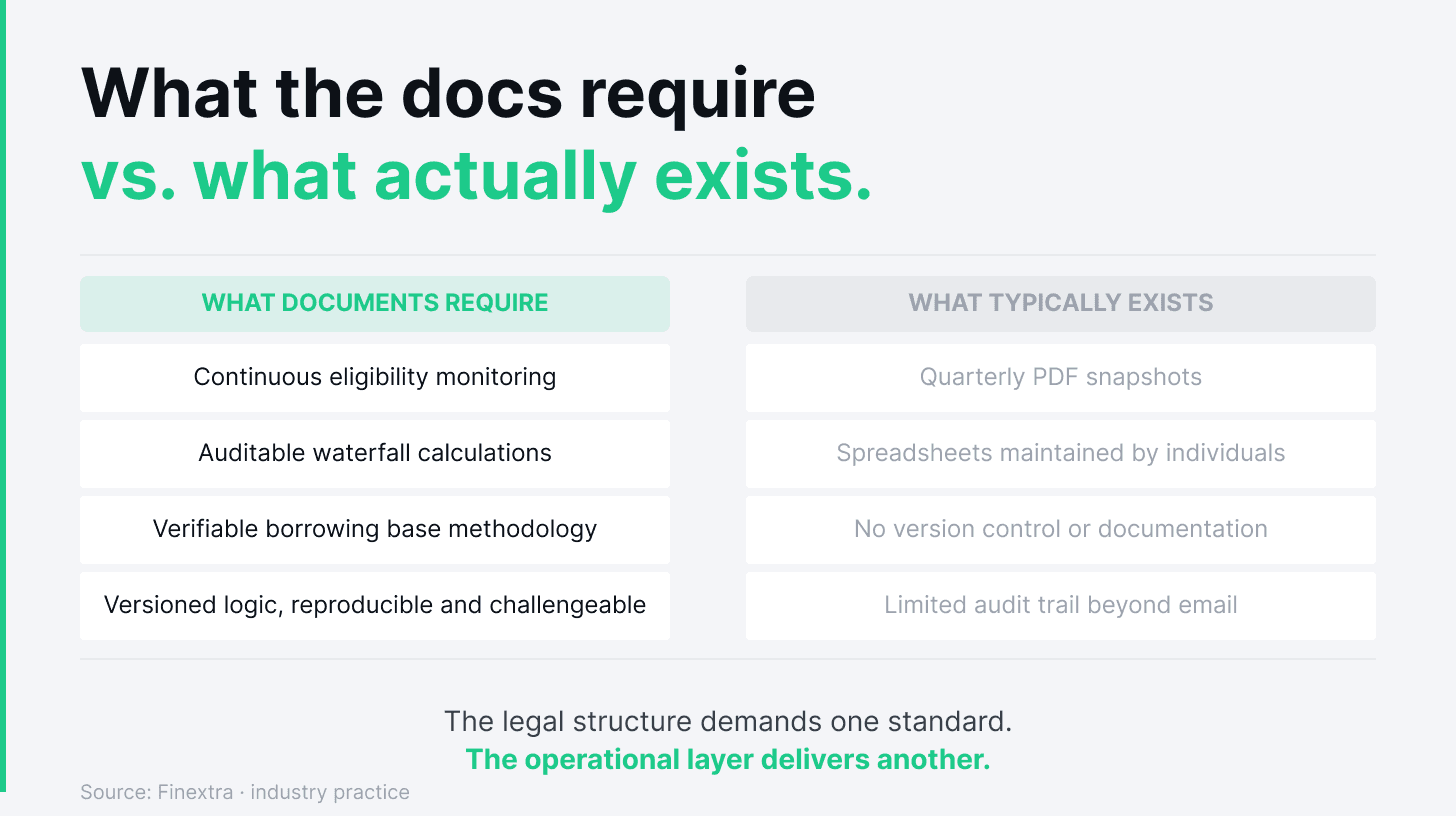

The operational infrastructure underneath compounds the problem. Most calculation agents in European private credit still run on spreadsheets, often sophisticated ones, but spreadsheets nonetheless.

No meaningful versioning. No automated testing. No audit trail beyond email attachments and a quarterly PDF.

When errors occur (a formula breaks, an eligibility criterion gets misconfigured after an amendment, a concentration limit is calculated on the wrong denominator) they tend to be caught and corrected quietly. The gap between what transaction documents require and what actually gets monitored on a continuous basis is wider than most capital providers appreciate.

This is the micro version of the IMF's macro argument. If the policy establishment is saying that supervision must extend to how transactions are executed at their most fundamental level, in the code itself, then the current state of calculation agent infrastructure in structured credit is a concrete example of what that gap looks like.

What Independent Means in Practice

Independence in the calculation agent role requires two things.

First, no commercial entanglement with any party to the transaction: no origination, no lending, no advisory mandate, no investment position.

Second, a verifiable methodology: inputs logged, calculations versioned, outputs traceable.

The first requirement disqualifies most parties currently performing this work, at least in principle.

The second is where software changes the picture.

→ Every calculation can be logged.

→ Every input recorded.

→ Every output tied to a specific methodology, a specific version, a specific date.

When a lender or investor asks how a borrowing base number was derived, the answer is a complete, auditable record that can be inspected, challenged, and reproduced.

European private credit has grown substantially in sophistication over the past decade. The capital entering the asset class is more institutional. Regulatory expectations, including European Securities and Markets Authority (ESMA) securitisation reporting, Digital Operational Resilience Act (DORA), and MaRisk for German vehicles, are more demanding. The structures themselves are more complex: multi-tranche, multi-originator, with eligibility criteria spanning dozens of parameters.

The operational layer has not kept pace. And the expectation that a calculation agent can demonstrate how it works, not just what it produced, is becoming more common among the institutional capital providers now allocating to the asset class.

The Layer That Connects

The institutions building settlement infrastructure (NYSE, Nasdaq, Morgan Stanley, BlackRock) are solving for the rails. The regulators (the SEC, CFTC, IMF) are solving for the rules.

The question for structured credit is whether anyone is solving for the operational layer in between: the verification, the calculation, the ongoing monitoring that determines whether capital is correctly allocated on every reporting date.

The macro case for tokenised finance is increasingly settled. The competitive pressure is real, and Dimon's letter makes that plain enough. The regulatory momentum is tangible and the market is scaling.

But infrastructure that moves fast without governance that keeps pace creates a specific kind of fragility. The IMF's April report describes this dynamic at the systemic level. In structured credit, the same dynamic plays out transaction by transaction, waterfall by waterfall, spreadsheet by spreadsheet.

The firms that can demonstrate verifiable, conflict-free, continuously auditable operational infrastructure will find themselves better positioned as the capital base grows more institutional and the regulatory lens sharpens.

That is the thesis behind Tranched and its calculation agent platform, built to deliver structural independence, automated audit trails, and methodology that can be inspected at any point in a transaction's life.

The macro is converging. The question is whether the micro catches up.