Welcome to this week’s Tranched newsletter.

In one week, regulators across the US, UK, and EU defined the legal architecture for tokenised finance. But while policy and infrastructure are accelerating, the critical data layer needed to price, verify, and scale tokenised assets at institutional level remains unresolved.

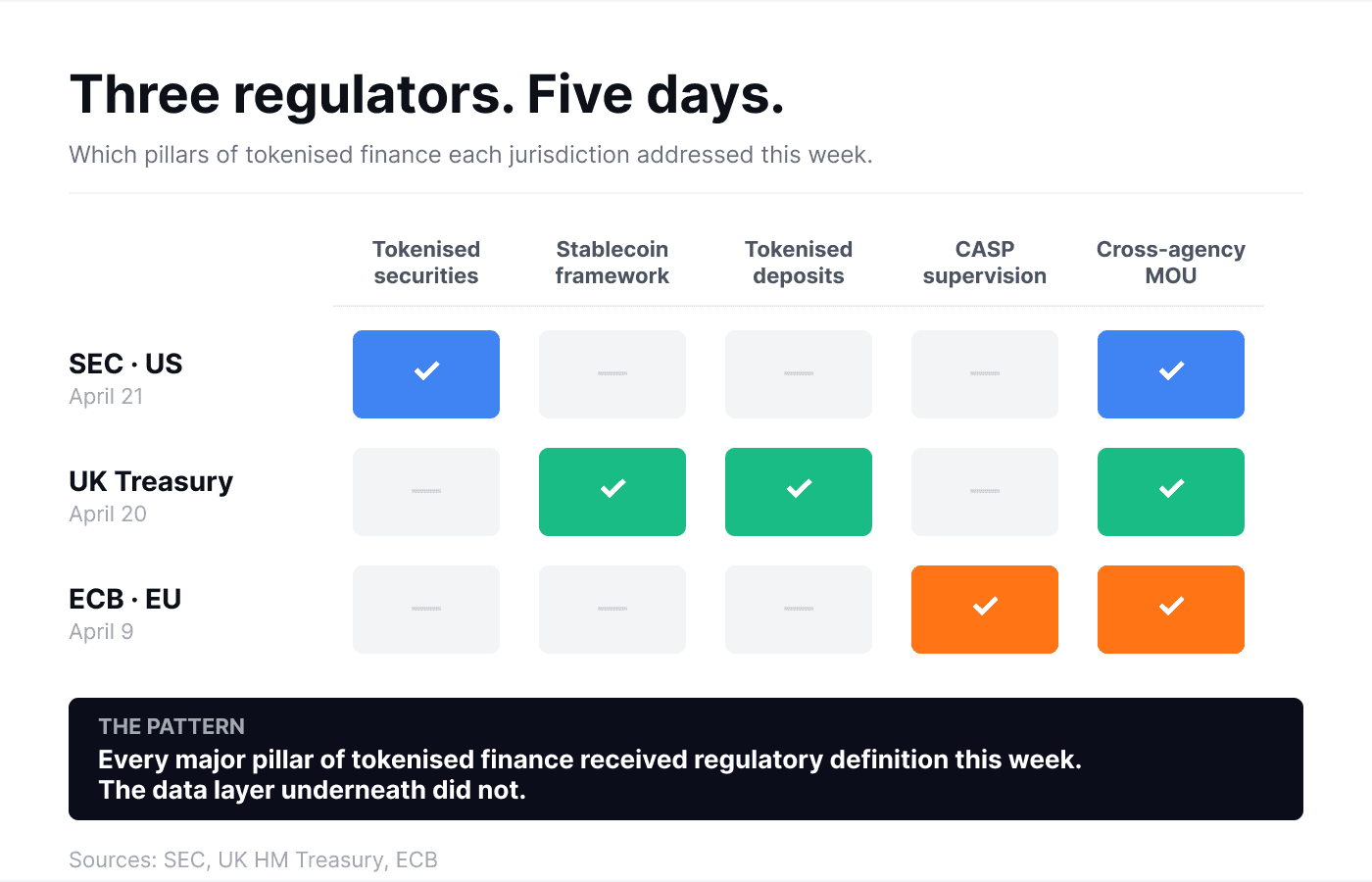

In the past five days, three regulators on three continents published the blueprints for how tokenised finance will actually work.

On Monday, SEC Chair Paul Atkins used the first anniversary of his chairmanship to unveil an "innovation exemption" for tokenised securities and formalise a memorandum of understanding with the CFTC. On Tuesday, the UK Treasury used Fintech Week London to announce a unified framework placing stablecoins, tokenised deposits, and traditional payments under one regime. Earlier in the month, the ECB published an opinion backing Brussels' plan to centralise supervision of crypto-asset service providers under ESMA, ending the jurisdictional race to the bottom that has defined MiCA's first year.

Same week, different continents, one direction of travel. The legal and supervisory architecture for tokenised finance is finally being defined.

And yet…

This week also produced a reminder that:

→ The announcements are not the deployment.

→ Regulation clears a path.

→ Rails carry a trade.

But the data layer underneath, the thing that makes any of it trustworthy at institutional scale, is still missing. And until it exists, the rest is scaffolding.

The Regulatory Layer Snaps Into Place

Atkins framed the innovation exemption in direct terms. Qualified firms will receive a 12 to 36 month grace window from full registration requirements to issue and trade tokenised securities on-chain, after which they must either demonstrate "sufficient decentralisation" or transition into the standard securities regime.

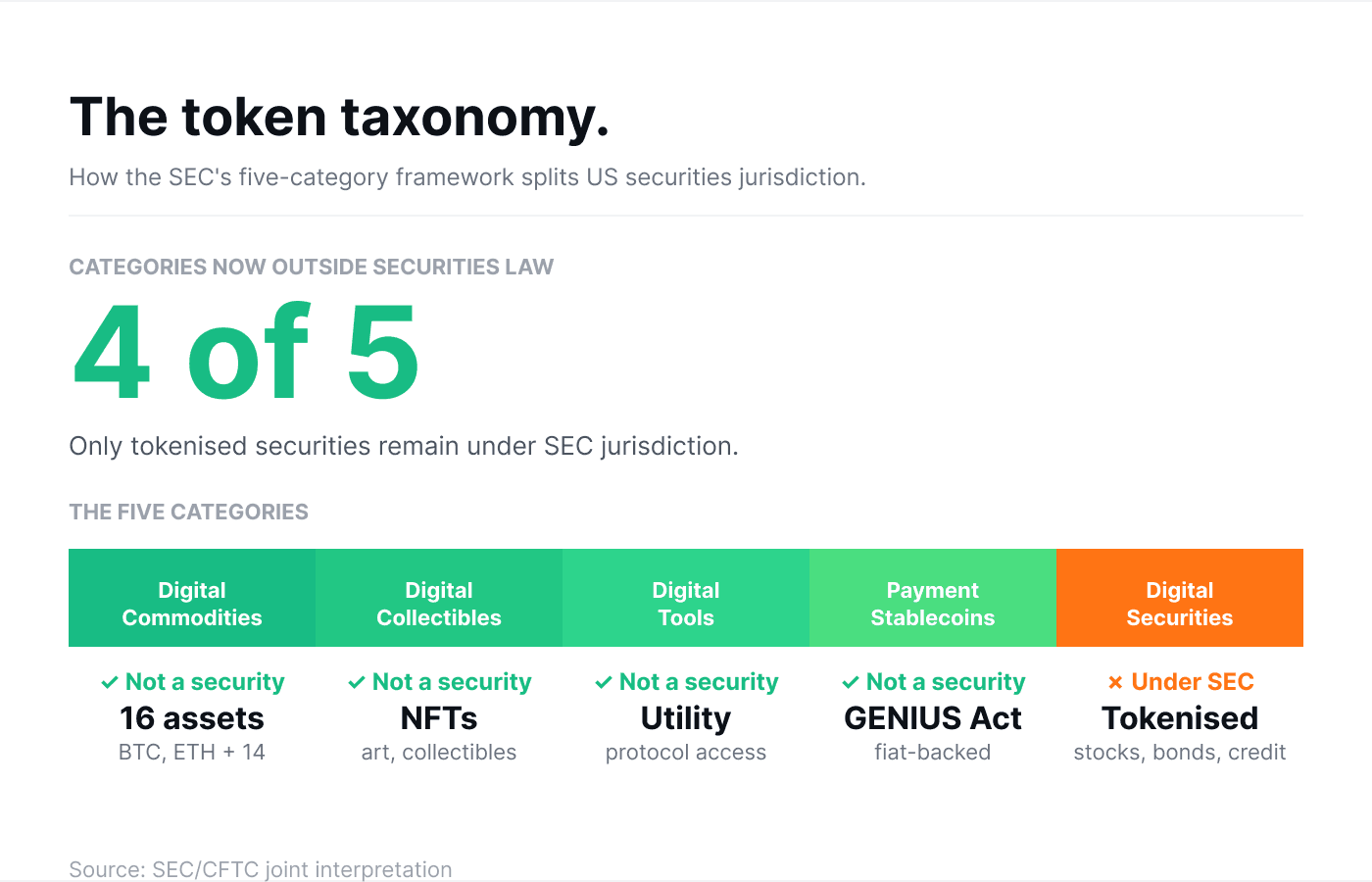

The exemption sits inside a broader five-category taxonomy jointly published with the CFTC in March, which placed four of the five token types (digital commodities, collectibles, tools, and stablecoins) outside securities law entirely. Only tokenised securities remain under SEC jurisdiction.

The message was explicit. "The SEC's head-in-the-sand posture and its shoot-first, ask-questions-later approach are days of the past," Atkins said. The agenda, branded "A-C-T" for advance, clarify, transform, is designed to keep tokenisation of equities, bonds, and other real-world assets inside US markets rather than pushing experimentation offshore.

The UK Treasury announced the same day what amounts to a parallel move. A single rulebook covering stablecoins, tokenised deposits, and traditional payment services under the Payment Services Regulations framework, alongside £1M of new fintech funding and the appointment of Chris Woolard (former interim CEO of the FCA) as Wholesale Digital Markets Champion. Firms are expected to begin applying for authorisation from September 2026, with full rules in force by October 2027.

The ECB's April 9 opinion, now gaining traction across European markets, completes the triangulation. The bank endorsed the Commission's plan to transfer authorisation, monitoring, and enforcement powers for all crypto-asset service providers from national competent authorities to ESMA, ending what France's AMF had called a "race to the bottom" among smaller jurisdictions competing for MiCA licences.

The Rails Are Being Poured

Underneath the regulation, the infrastructure is already being built.

The NYSE and Securitize signed an MOU on April 14 to develop a tokenised securities platform, with Securitize positioned as the lead digital transfer agent for the new venue. Subject to SEC and FINRA approval, the platform will support 24/7 trading of US-listed equities and ETFs, fractional share purchases, stablecoin-based funding, and on-chain settlement via multiple blockchains. ICE is working in parallel with BNY and Citi to support tokenised deposits across its clearing houses.

On April 21, Digital Asset published a report documenting live cross-border repo trades settled using tokenised collateral. The headline finding: atomic settlement eliminates the idle collateral and time-zone friction that have historically limited the liquidity of cross-border securities finance.

The market data backs the infrastructure story.

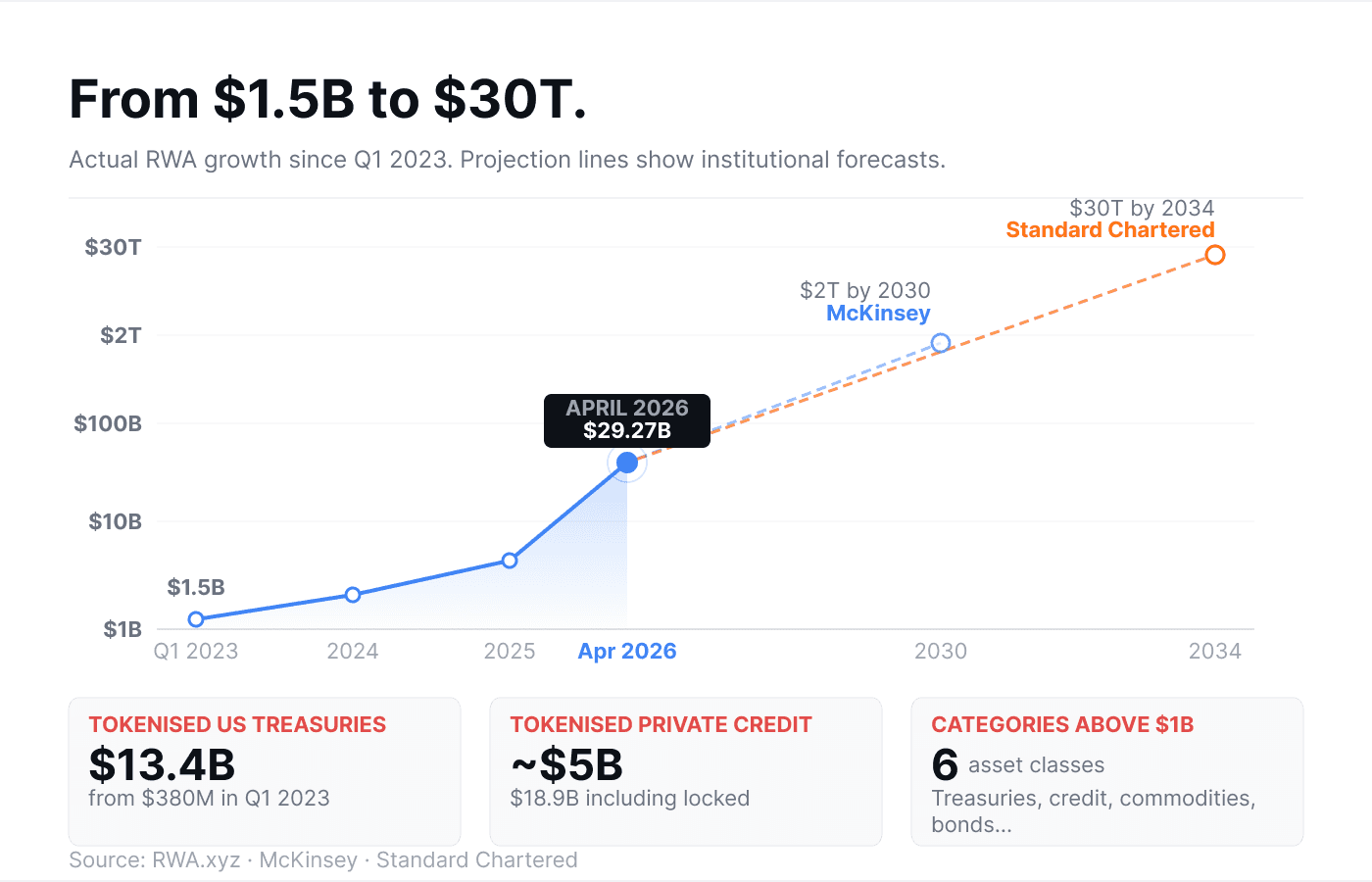

Tokenised real-world assets crossed $29.27B on-chain in April, a roughly 20x expansion over three years. Tokenised US Treasuries alone grew from $380M in Q1 2023 to $13.4B today, with BlackRock's BUIDL at $2.4B, Ondo's suite at $2.6B, and Circle's USYC at $2.7B leading the category. Six individual RWA categories (Treasuries, private credit, commodities, corporate bonds, non-US sovereign debt, and institutional funds) now each exceed $1B in distributed on-chain value.

Standard Chartered projects the tokenised RWA market will reach $30T by 2034. McKinsey's more conservative $2T by 2030 gets to the same place more slowly. Either number describes an order-of-magnitude expansion from where the infrastructure sits today.

The Pressure Test

In March, Blackstone's $82B BCRED fund faced $3.7B in quarterly redemption requests, a record 7.9% of fund shares. The standard tender-offer cap is 5%. Blackstone lifted it to 7% and then, rather than gate investors, the firm and its employees directly bought the remaining 0.9%, roughly $400M in combined contributions, to meet 100% of withdrawal demand.

The episode is being read across private credit as a stress test survived. It should also be read as evidence of what the current data layer can and cannot support. BCRED met its redemptions not because an authorised participant could arbitrage the wrapper against its underlying at tight spreads, but because a trillion-dollar manager absorbed the shortfall with its own balance sheet. The redemption was met. The substantiation problem was not solved.

Blue Owl, Ares, and several smaller managers have faced similar pressure in recent quarters. Apollo CEO Marc Rowan, speaking on CNBC last week, was blunt: "If you can't, as a first lien credit manager, meet 5% redemptions per quarter, I'll say it frankly: You're an idiot." The statement is defensible on his firm's numbers. It also points at the harder question sitting underneath: in a tokenised, daily-liquid ETF wrapper, who substantiates NAV on a bespoke private credit loan when the AP cannot see the instrument-level state?

This is the gap the regulation and the rails do not close.

The Data Layer Problem

The disconnect has a technical name. A private credit ETF operates a daily-liquid wrapper over an asset class whose instruments are bespoke, bilaterally negotiated, and documented in hundreds of pages of governing legal text. For that wrapper to trade at tight spreads, an authorised participant has to substantiate NAV independently of the manager. For public credit, that works because observable trades, dealer quotes, and evaluated pricing services triangulate from comparables. For bespoke private credit, none of those inputs exist at the granularity the arbitrage requires.

A recent Nammu21 analysis laid this out in detail. An authorised participant needs two things to price a bespoke loan. First, the instrument itself: covenant package, amendment mechanics, EBITDA definitions, event-of-default terms, prepayment economics, all rendered as structured, machine-readable data rather than a PDF to be parsed. Second, a continuous event stream (waivers, amendments, revolver draws, rating migrations) delivered faster than the quarterly reporting cycle most private credit still runs on.

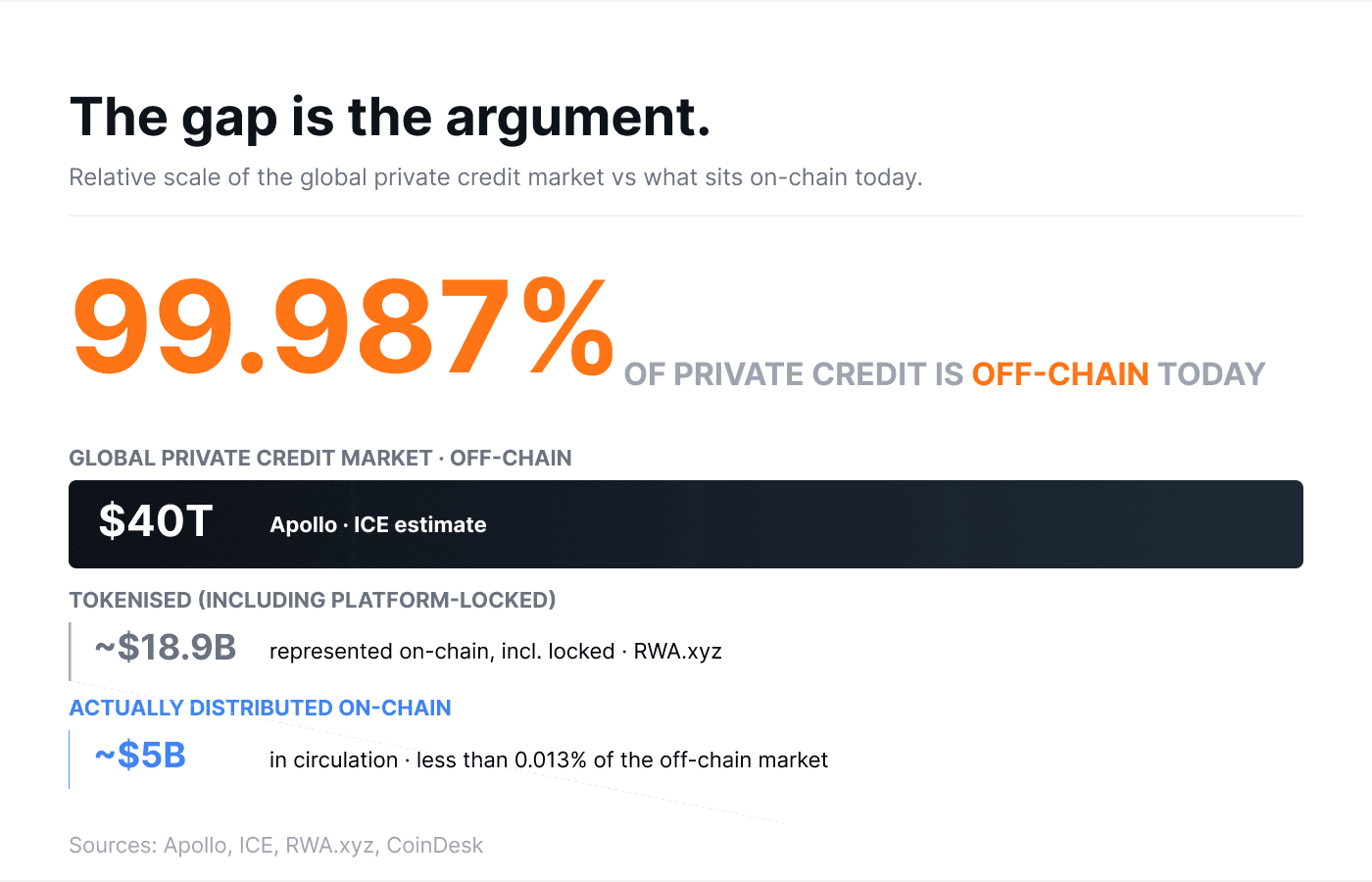

Neither exists today at the cadence required. The industry knows. ICE launched ICE Private Credit Intelligence in March 2026 with Apollo as anchor partner, explicitly positioned to address the fact that "the data infrastructure supporting the asset class has not kept pace." ICE evaluates roughly 3M fixed income instruments today. The private credit market they are trying to instrument is $40T. The gap is the business opportunity.

This is the layer that most directly determines whether any of the regulatory or infrastructure work announced this week actually scales. A tokenised private credit ETF with quarterly reporting is still a quarterly reporting problem, just with a blockchain wrapper.

Where This Lands

Regulation clears the path. The SEC's innovation exemption, the UK's unified framework, and the ECB's supervisory consolidation are collectively the most coordinated legal infrastructure the asset class has ever had.

Rails carry the trade. NYSE/Securitize, Digital Asset's repo infrastructure, and the $29B in tokenised RWAs already on-chain establish that the plumbing works.

The data layer is still missing. Every calculation agent function (waterfall distribution, borrowing base certification, eligibility testing, covenant monitoring) sits between the instrument and the wrapper.

In traditional private credit, those functions are run periodically, often on spreadsheets, frequently by parties with commercial entanglement to the transaction. A tokenised wrapper moving at 24/7 cadence over an underlying calculated quarterly by a conflicted agent is not an infrastructure that scales to $30T.

This is the layer Tranched is building. Verifiable methodology. Structural independence between the certifying party and the transaction. Every input logged. Every output tied to a specific version and date. Continuous calculation against a live portfolio state rather than a snapshot from the last reporting cycle.

You can tokenise a bespoke loan. You can trade it 24/7. But if no one can tell you what it is worth at 2am, none of the rest matters.