Regulation

Welcome to this week’s Tranched newsletter.

We examine how on-chain yield markets, built on staking, lending and increasingly sophisticated vault infrastructure, are scaling faster than the regulatory vocabulary used to describe them.

As stablecoin credit deepens, real-world asset collateral enters protocols and programmable vaults formalise allocation logic, questions of legal attribution and enforceability move to the forefront.

Drawing on proposals to bind smart contracts to recognised electronic credentials under the EU’s eIDAS framework, we explore how execution logic, identity and supervision may converge, and why that alignment will determine whether on-chain lending remains peripheral or integrates into broader capital markets infrastructure.

The Vocabulary Gap

Decentralised finance yield products are increasingly becoming part of mainstream capital flows.

Major exchanges have begun offering multi-protocol yield solutions, for example Kraken’s launch of DeFi Earn, which aggregates yield across several protocols and chains and attracted substantial deposits in its first week of operation.

Traditional asset managers are also stepping into the space. Bitwise Asset Management has rolled out Morpho-based USDC yield vaults, positioning itself as a curator of on-chain yield products. At the same time, institutional interest in staking infrastructure is rising, with firms like Ripple expanding custody and staking integrations aimed at large clients.

Lending markets continue to deepen as well, with decentralised lending protocols recording significant growth in total value locked and stablecoin lending activity, spurred by increasing institutional participation and real-world asset collateralisation. Capital is therefore moving through more structured on-chain vehicles, reflecting both investor demand and product innovation.

Despite these developments, regulatory and policy discussions are still grappling with foundational definitions. Draft documents have continued to reference concepts such as “staking stablecoins,” even though staking, by design, pertains to supporting proof-of-stake network security and is inapplicable to stablecoins.

Precision in terminology matters. Before capital markets infrastructure can scale, its core mechanics must be properly understood.

Let's open up our glossary for a moment.

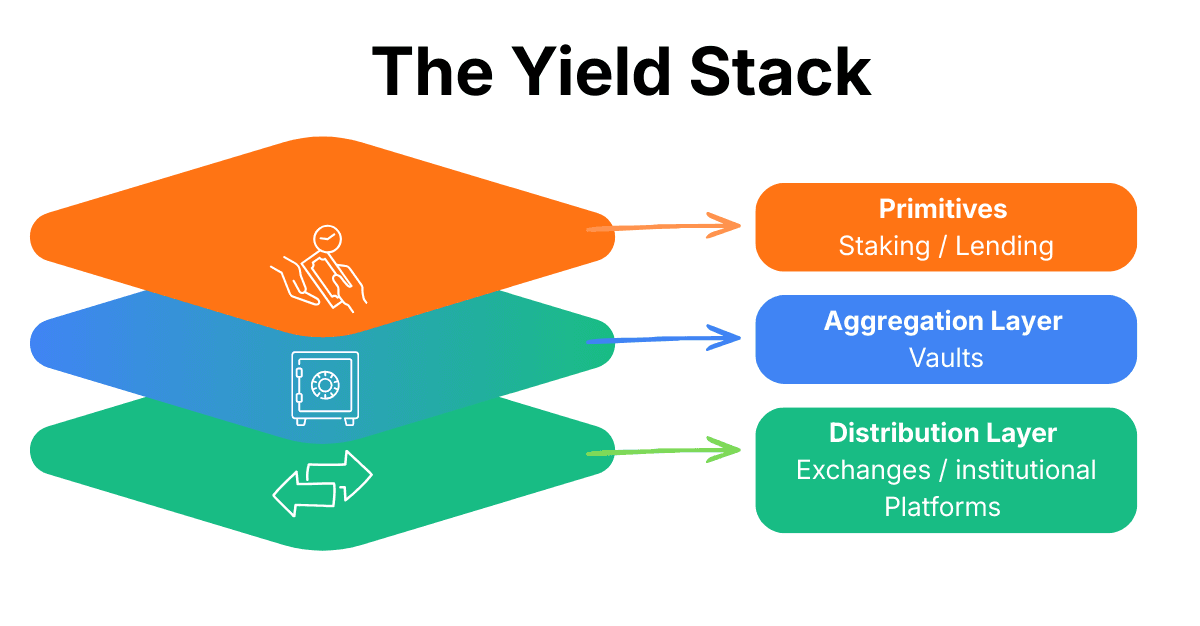

In on-chain finance, yield typically derives from a small set of distinct primitives:

Staking

This refers to participation in network validation in exchange for protocol rewards and transaction fees.Lending

This encompasses supplying capital to borrowers who pay interest, typically against over-collateralised positions.

Layered on top of these primitives are vault structures.

Vault structures are programmable allocation engines that aggregate yield strategies across protocols and chains under predefined constraints.

Once these key mechanics are understood, we can now shift our attention to how they are recognised and enforced within existing legal systems.

From Cryptographic Assurance to Legal Attribution

Vault infrastructure introduces a meaningful shift in how yield products are constructed.

Capital allocation rules are embedded in code.

Exposure limits are programmable.

Asset movements are observable on-chain.

Withdrawal rights are encoded rather than discretionary.

These features provide strong forms of technical assurance by allowing participants to verify where assets sit and how they are deployed.

As adoption widens, deeper questions emerge around identity and enforceability.

When a smart contract executes capital allocation decisions, under which legal identity does it operate?

How is accountability established across jurisdictions?

How do existing trust frameworks recognise programmable execution?

These questions sit at the intersection of technology and law.

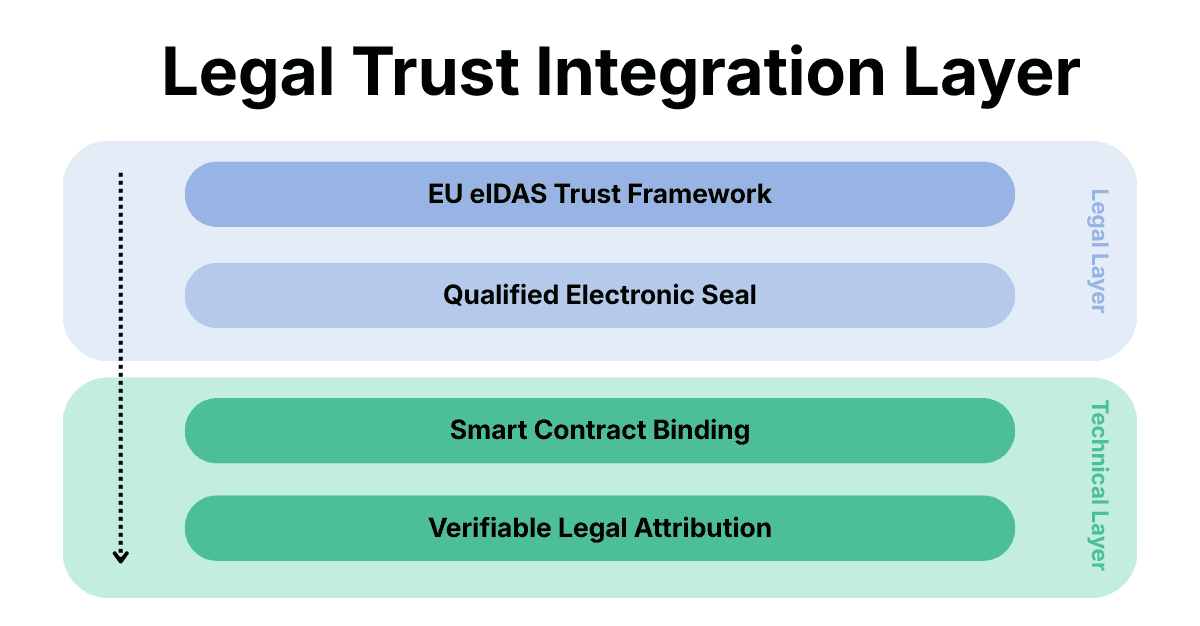

The academic paper “Know Your Contract: Extending eIDAS Trust into Public Blockchains” addresses this intersection directly. The European Union’s eIDAS framework governs qualified electronic signatures and seals. The authors propose extending the European Union’s eIDAS trust framework into public blockchain environments by binding smart contracts to legally recognised electronic credentials.

Under this architecture:

A smart contract can be cryptographically linked to a qualified electronic seal.

Identity attribution can be machine-verifiable.

Compliance checks can be embedded into execution logic.

Regulatory oversight can interface with public networks without relying solely on intermediaries.

The objective is to create a bridge between public blockchain execution and established European trust infrastructure.

As product complexity increases and capital allocators demand stronger accountability, that bridge moves from theoretical design to practical necessity.

Infrastructure Is Maturing

This proposal to bind smart contracts to recognised electronic credentials reframes the regulatory conversation.

The discourse moves beyond how tokens are classified or how intermediaries are supervised and begins to encompass how legally recognised identity attaches to autonomous execution.

Most regulatory frameworks today are designed around identifiable actors: issuers, custodians, brokers, asset managers. Yet programmable vaults and allocation engines operate according to embedded logic that can deploy capital without discretionary intervention.

As these structures scale, the gap becomes clearer.

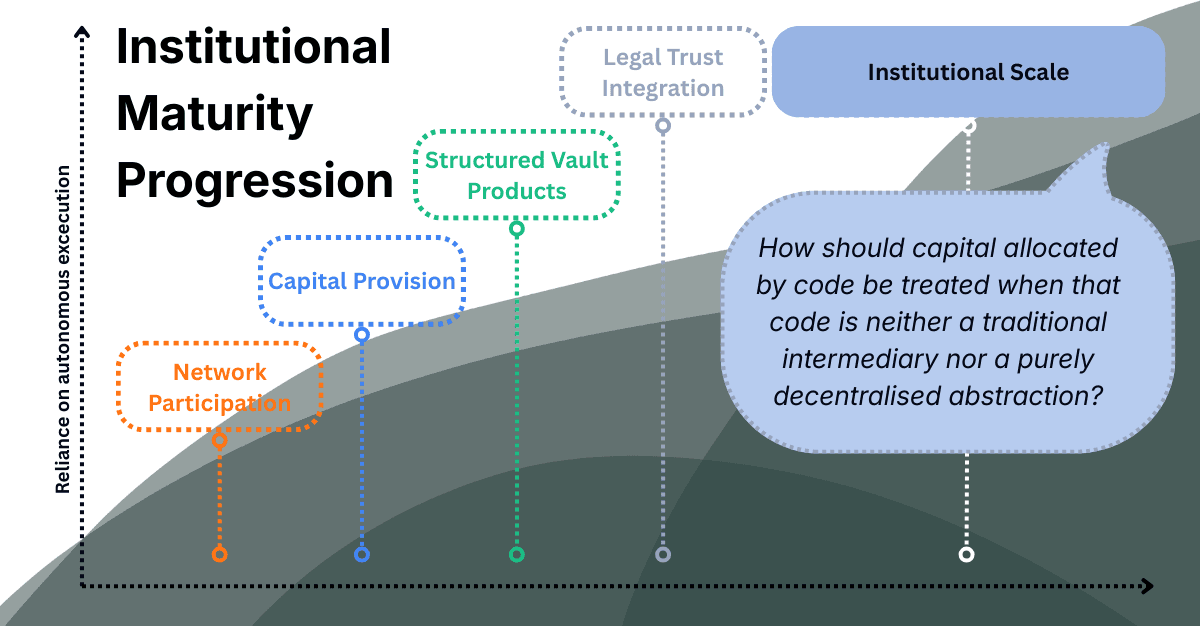

Institutional engagement with on-chain yield markets tends to follow a progression:

Initial participation at the network layer through staking

Engagement with lending markets that mirror structured credit

Adoption of programmable vaults capable of dynamic allocation

Each step increases reliance on autonomous execution.

At that point, the legal system encounters a structural question: how should capital allocated by code be treated when that code is neither a traditional intermediary nor a purely decentralised abstraction?

These are not abstract concerns. They directly affect:

Balance sheet recognition

Capital treatment and risk-weighting

Counterparty exposure analysis

Supervisory accountability

Insolvency interpretation

Regulatory bodies will soon need to address:

Whether cryptographically bound smart contracts can function as legally attributable execution agents, and under what conditions.

How fiduciary responsibility interacts with embedded allocation constraints

How supervisory oversight applies when financial logic is executed automatically rather than through human discretion.

As programmable finance becomes embedded within structured products, the regulatory perimeter must expand beyond actors to include execution logic itself.

That transition marks the point at which programmable finance begins to integrate with capital markets infrastructure.

Earlier, we opened the glossary.

Yield in on-chain finance rests on primitives like staking and lending, and scales through vault infrastructure that aggregates, constrains, and distributes that yield. What began as protocol-native activity is increasingly being structured into products accessible to a broader set of allocators.

What are we witnessing as a result?

Lending markets are expanding in both depth and composition.

Stablecoin credit has become a meaningful liquidity layer.

Real-world asset collateral is entering protocol environments.

Institutional participants are engaging not only with token exposure, but with programmable credit infrastructure.

Vaults play a central role in that shift by transforming lending activity into structured vehicles. Allocation parameters are encoded, exposure limits are predefined and capital is deployed according to transparent logic rather than discretionary mandate.

As this architecture matures, legal and supervisory interpretation becomes inseparable from product design.

These considerations sit alongside yield mechanics. They shape whether on-chain lending remains a parallel system or becomes embedded within broader capital markets infrastructure.

The discussion around legally attributable smart contracts, including proposals to bind execution logic to recognised electronic credentials, reflects this maturation. It signals a move toward integrating programmable finance within established trust frameworks rather than operating outside them.

The vocabulary is clarifying.

The infrastructure is scaling.

The legal framing is emerging.

How those elements align will determine the durability of the system being built.