On-chain Infrastructure

Welcome to this week’s Tranched newsletter.

We examine how autonomous AI systems are beginning to function as capital allocators by managing treasuries, optimising yield and executing financial decisions at a speed and scale that existing market infrastructure was not designed to accommodate.

As stablecoin settlement volumes approach those of traditional payment rails, tokenised Treasury markets cross $9B and institutional structured credit moves on-chain, the question becomes what the architecture needs to look like for that participation to be reliable.

Drawing on developments across agent payment infrastructure, tokenised real-world assets and on-chain credit protocols, we explore how the financial stack is being rebuilt from the settlement layer up, and why the institutions that move earliest on infrastructure will define how this market matures.

One of the most significant themes at Consensus Hong Kong was more structural than price action or the latest cycle’s dominant narrative.

Capital on-chain is increasingly being positioned for machines.

Across panels, private roundtables, and investor conversations, this sentiment gave rise to questions such as:

What happens to market structure when AI agents become active allocators of capital?

What does settlement latency mean when your counterparty operates in milliseconds?

What does portfolio rebalancing look like when it's governed by code rather than quarterly committee decisions?

This was a conversation centered around infrastructure, and whether traditional financial rails can accommodate systems that never sleep, never wait for a human to approve a transaction, and optimise continuously within pre-defined mandates.

The Architecture Problem

To understand why this matters, consider the mismatch.

Traditional banking infrastructure was designed around human decision cycles: quarterly allocation committees, T+2 settlement, batch reporting, and operational layers that assume humans are always in the loop. Those assumptions made sense for decades because humans were always in the loop.

AI systems operating as treasury agents, liquidity managers, or hedging engines don't share those constraints. They can monitor positions in real time, execute conditional logic across dozens of instruments simultaneously, and respond to changes in spread or yield without waiting for a meeting.

Here, the bottleneck becomes the infrastructure itself, specifically, settlement latency, data opacity, and the inability of legacy systems to interact with programmable logic.

This is why blockchains entered the conversation at Consensus, as the machine-native financial rails.

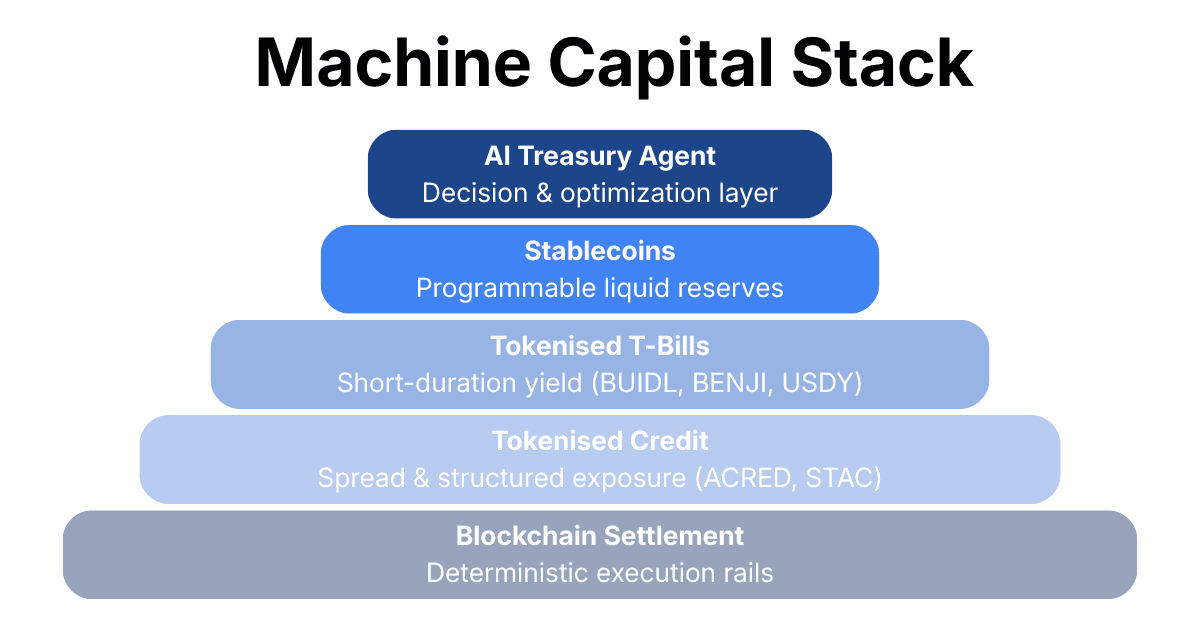

What features does an autonomous treasury system actually need to function?

Deterministic settlement

Programmable constraints embedded in smart contracts

Transparent on-chain data

These are no longer features that solely appeal to retail crypto users.

The question is whether on-chain infrastructure has matured enough to serve these functions at institutional scale. The evidence from 2025 suggests it has moved considerably further than most outside the space realise.

What Machines Hold: The Stablecoin Layer

If you grant the premise that AI systems will begin managing meaningful capital allocations, a natural follow-on question is:

In what form do they hold liquid reserves?

If autonomous systems begin managing meaningful capital allocations, the question of what form they hold liquid reserves in has a fairly obvious answer: stablecoins.

As instruments that settle instantly, integrate natively with smart contract logic, and compose with yield-bearing on-chain products, stablecoins offer something traditional cash accounts never could: a reserve asset that a machine can programmatically deploy without human intervention

The infrastructure is already in place. Coinbase, Google, Visa, and Stripe have all shipped or announced agent payment standards over the past year. Total stablecoin transaction volume hit $33T in 2025, up 72% year-on-year according to Artemis Analytics, with Q4 alone recording $11T. Furthermore, stablecoin issuers now collectively hold over $150B in U.S. Treasuries, making them the 17th largest holder of U.S. government debt globally.

The more interesting question that was front of mind at Consensus, is what agents do with idle reserves. An autonomous treasury system holding stablecoin balances and optimising continuously will route that liquidity somewhere. The question is where, and what that demand looks like at scale.

Tokenised Yield: The First Natural Destination

When a system holding liquid stablecoin reserves is optimising continuously, idle cash is an inefficiency by definition. The most natural first destination, with sufficient regulatory clarity, institutional credibility, and on-chain composability, is tokenised short-duration government debt.

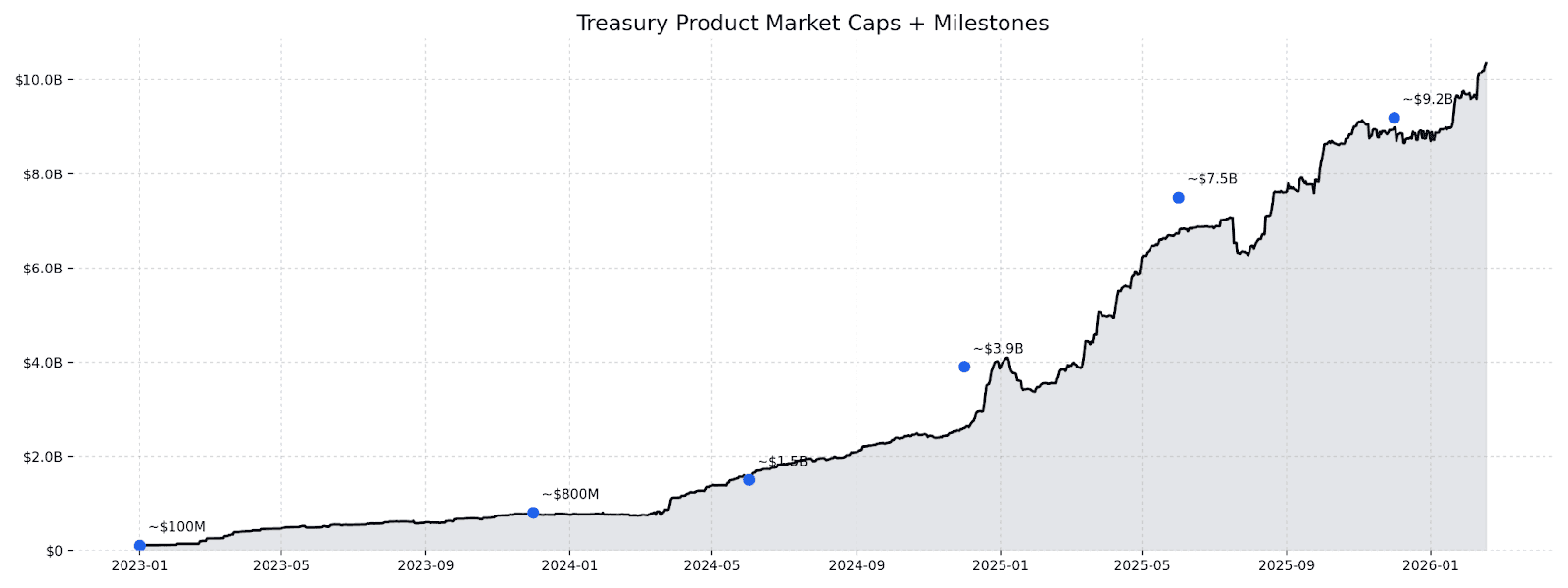

The market has grown from under $100M in early 2023 to $9.2B by the end of 2025. BlackRock's BUIDL fund, managed via Securitize, reached $2.3B in AUM and has become collateral for an expanding class of on-chain products such as Ethena's USDtb and Ondo's OUSG. BUIDL has also been accepted as collateral on Binance, a transition that moves it from a cash management instrument into genuine market plumbing.

These are regulated, yield-bearing instruments that settle atomically, are readable by machine, and compose natively with DeFi protocols, all properties an autonomous treasury agent requires. For such a system, the spectrum from stablecoin reserves to T-bill exposure to diversified credit forms a complete, programmable capital stack.

Source: rwa.xyz (Treasury Product Metrics), accessed Feb 2026

Structured Credit: The Harder, More Interesting Problem

The most underappreciated implication of this theme is what it means for structured credit.

Traditional securitisation markets operate through operationally heavy processes:

Committee-driven allocation decisions

Quarterly reporting cycles

Manual reconciliation across servicers and trustees

Settlement timelines that routinely stretch to weeks

Traditional securitisation markets are operationally heavy by design. Loan eligibility is governed by complex, deal-specific criteria. Waterfall payment logic that determines who gets paid what, in what order and under which conditions, requires continuous monitoring of portfolio performance against concentration limits, delinquency triggers, and regime states.

The information that would allow dynamic, real-time risk management exists in these markets is trapped in formats that neither machines nor most humans can access efficiently.

When the underlying mechanics of securitisation move on-chain, they become machine-readable by definition.

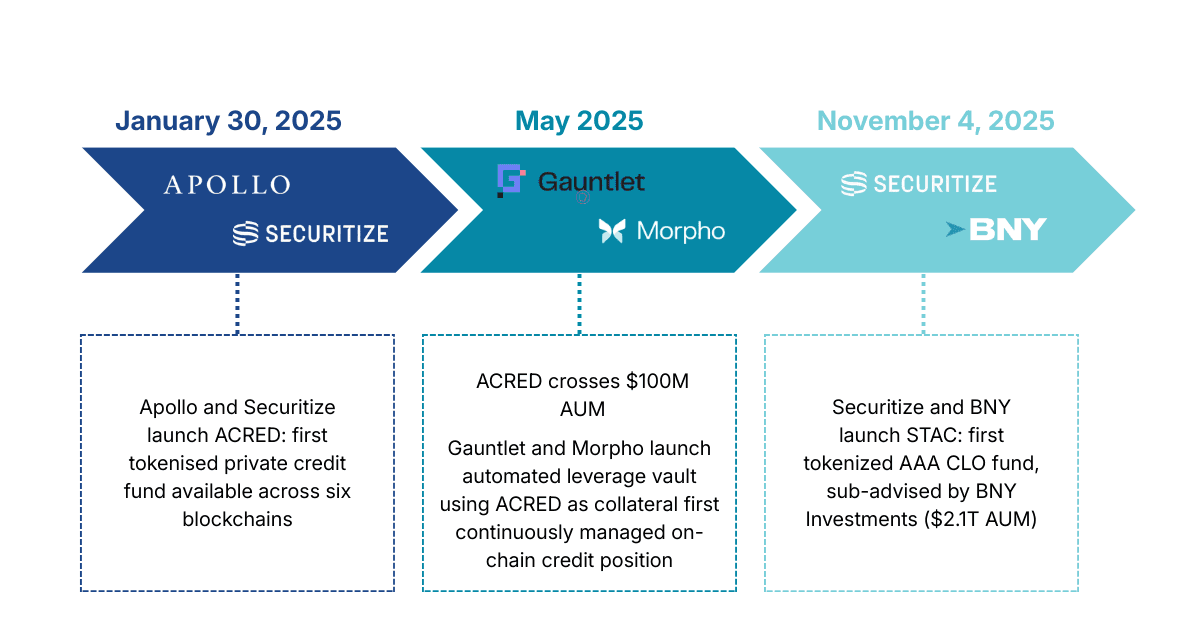

Securitize and BNY launched the first tokenised AAA CLO fund in November 2025, with BNY Investments, who manages $2.1T in fixed income, as sub-advisor and a $100M anchor from Grove Protocol. The global CLO market exceeds $1.3T.

What's been tokenised is still a rounding error, but the institutional infrastructure is now in place.

Separately, Gauntlet's automated leverage vault using Apollo's ACRED tokens as collateral on Morpho offers a more speculative preview.The vault continuously monitors yield and borrow rates, adjusting exposure without human intervention. It's a prototype of the logic that has the potential to govern AI-managed credit portfolios.

The academic literature on automated financial systems is instructive here. Research on algorithmic market-making and reinforcement learning applied to fixed income consistently finds that the binding constraint on automation in credit markets is data accessibility and settlement friction. If you remove those constraints, the systems can function. On-chain credit infrastructure is precisely what removes them.

The Governance Questions That Don't Have Answers Yet

It is important to note that the shift toward machine capital allocation introduces problems the industry is yet to solve.

The most serious is liquidity reflexivity in stress events. When multiple automated systems optimise against similar signals within similar risk parameters, correlated behaviour during market dislocations becomes likely. Credit markets, where liquidity is thinner and bid-ask spreads can widen dramatically under stress, are more vulnerable than equity markets where algorithmic flash crashes have already occurred.

There's also the liability question. If an autonomous system makes an allocation decision that results in loss, whether accountability lies with the model, the operator, or the protocol, is genuinely unclear. This is a practical barrier institutions will need resolved before permitting AI systems real discretion over capital. The jurisdictions advancing stablecoin licensing frameworks such as the EU's MiCA, Singapore's MAS, and the U.S. post-GENIUS Act environment, are better positioned to attract institutional deployment of autonomous systems precisely because they provide the legal clarity AI-managed treasuries require.

So how do we think about this opportunity?

Previous cycles asked: which assets appreciate? The conversation at Consensus Hong Kong asked something different: which on-chain instruments can automated systems safely hold, transact, and compose?

The marginal buyer of tokenised yield in this scenario isn't a portfolio manager reviewing quarterly allocations. It's an automated treasury agent rebalancing continuously within a defined mandate. This changes the demand dynamics for these instruments in ways meaningful for anyone building or investing in the underlying infrastructure.

The build phase is underway. The governance frameworks and liability structures that would allow institutions to deploy AI systems with real discretion are not yet in place, but the conversation has moved from whether machine capital will participate in on-chain finance to what the necessary conditions are for it to do so at scale. This is a meaningful shift in the seriousness of the question being asked.