Welcome to this week’s Tranched newsletter.

Private credit was built to fill the void that banks left after 2008. It grew into a $3.5T market on the promise of steady, uncorrelated returns. Now, AI disruption, collateral fraud, and redemption queues have arrived in the same quarter, and that promise is facing its first real test.

This week, we trace the full arc, from ancient grain loans to the AI reckoning, and ask whether private credit's infrastructure can support the weight it now carries.

3000 BCE: The original non-bank lenders

The idea of lending outside formal banking institutions is older than banking itself.

The earliest recorded loans were scratched onto clay tablets in Mesopotamia around 3000 BCE, where temples and palaces functioned as proto-banks, lending grain and silver to farmers and merchants. The Code of Hammurabi, issued around 1754 BCE, capped interest on silver loans at 33% and included what may be the world's first debt forgiveness clause: if a storm destroyed the harvest, the borrower owed nothing that year.

For millennia, the pattern repeated. When formal institutions could not or would not lend, private capital found a way. Pawnbrokers in ancient Greece and Rome. Mezzanine-style financing along the Silk Road. Letters of credit during the Mughal dynasty. The structural logic has always been the same: where regulated capital retreats, unregulated capital advances.

That logic has never been more relevant than it is right now.

1977: The junk bond revolution

The modern story of private credit begins not in 2008, but in a Los Angeles office far from Wall Street, where a young bond trader named Michael Milken was developing a thesis that would reshape corporate finance.

Milken's insight was that lower-rated corporate bonds were systematically mispriced. The market treated them as untouchable. He treated them as an overlooked asset class. From his desk at Drexel Burnham Lambert, he began issuing high-yield bonds for companies that traditional banks refused to serve, and the numbers proved him right. High-yield bond issuance went from $300M in 1977 to over $18B by 1986, with Drexel commanding 53% market share.

The high-yield market became the engine of the leveraged buyout boom. Milken financed the corporate raiders, Carl Icahn, T. Boone Pickens, Ronald Perelman, and enabled deals like the $25B RJR Nabisco buyout that defined an era. By the mid-1980s, Milken was earning over $500M a year.

Then it collapsed. Milken was charged with securities fraud in 1989. Drexel Burnham Lambert filed for bankruptcy in February 1990. The junk bond market froze. But the infrastructure Milken built did not disappear. As Bloomberg has noted, private credit today is "a new label on an old wine," the newest phase of the leveraged debt revolution that Drexel started. Nearly every major player in today's private credit landscape traces a direct or indirect lineage to Drexel alumni.

1990s–2000s: Mezzanine and the middle market

With the junk bond market in retreat, the financing needs of smaller companies did not vanish. They migrated into a private market alternative: mezzanine lending. Mezzanine funds like Crescent Mezzanine offered subordinated debt that sat between senior bank loans and equity, structured with payment-in-kind interest and equity warrants, targeting returns of 18–20%.

Banks, meanwhile, were being reshaped by regulation. The Highly Leveraged Transaction (HLT) rules of the late 1980s discouraged lending to companies where debt exceeded 6x EBITDA. The proliferation of CLOs through the 1990s allowed institutional investors to access leveraged loans for the first time, and the leveraged finance market grew to $3T by 2021. But privately originated credit was growing faster.

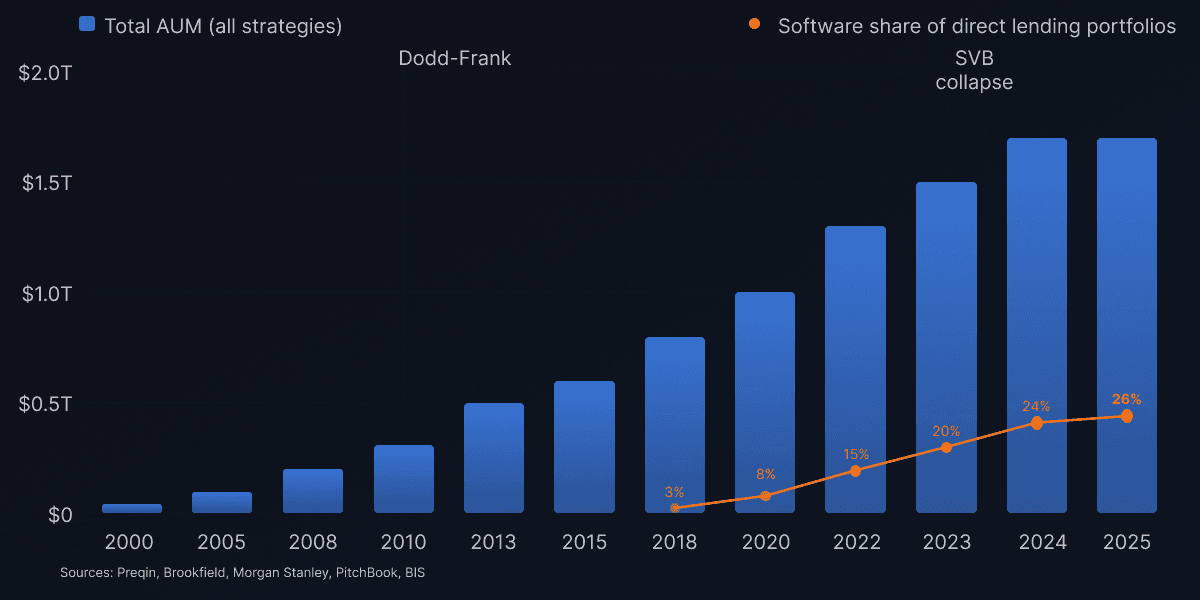

By the early 2000s, private credit AUM reached $44B, with dedicated mezzanine funds serving companies too small for the public high-yield market and too leveraged for traditional banks. The architecture of what would become a multi-trillion dollar asset class was already being laid.

2008: The great substitution

The Global Financial Crisis transformed private credit from a niche strategy into a structural pillar of global finance.

When Lehman Brothers collapsed in September 2008, the banking system seized. What followed was the most aggressive regulatory tightening in a generation. Basel III raised capital requirements, the Dodd-Frank Act made middle-market lending more expensive for regulated institutions, and banks began a retreat from corporate lending that has never fully reversed. According to the Federal Reserve, private credit now accounts for approximately 15% of outstanding corporate debt, with aggregate volumes comparable to leveraged loans and high-yield bonds combined.

By 2010, private credit AUM had reached $310B. The asset class had found its structural rationale: where banks could no longer go, private lenders would.

2015–2023: Software becomes the consensus trade

The growth accelerated through the 2010s, but it was not evenly distributed. Beginning around 2020, enterprise software became the consensus trade in private credit. The thesis was intuitive: recurring subscription revenue, high margins, sticky customer bases, low historical default rates. Between 2020 and 2023, direct lenders funded 40–70% of leveraged buyouts, up sharply from 15–25% pre-pandemic. By end-2025, according to the BIS, outstanding loans to SaaS firms had reached over $500B, accounting for 19% of total direct loans. Morgan Stanley estimates software exposure across direct lending portfolios at approximately 26%.

The asset class overtook venture capital to become the second-largest private market strategy behind private equity. Retail investors flooded in through BDCs and semi-liquid vehicles. Evergreen private credit fund assets surged to $644B, up 28% from end-2024. Covenant-lite structures proliferated. A "zero-loss fantasy" took hold.

Every metric that credit committees rely on, pointed in the same direction. Then the direction changed.

Early 2026: The AI reckoning

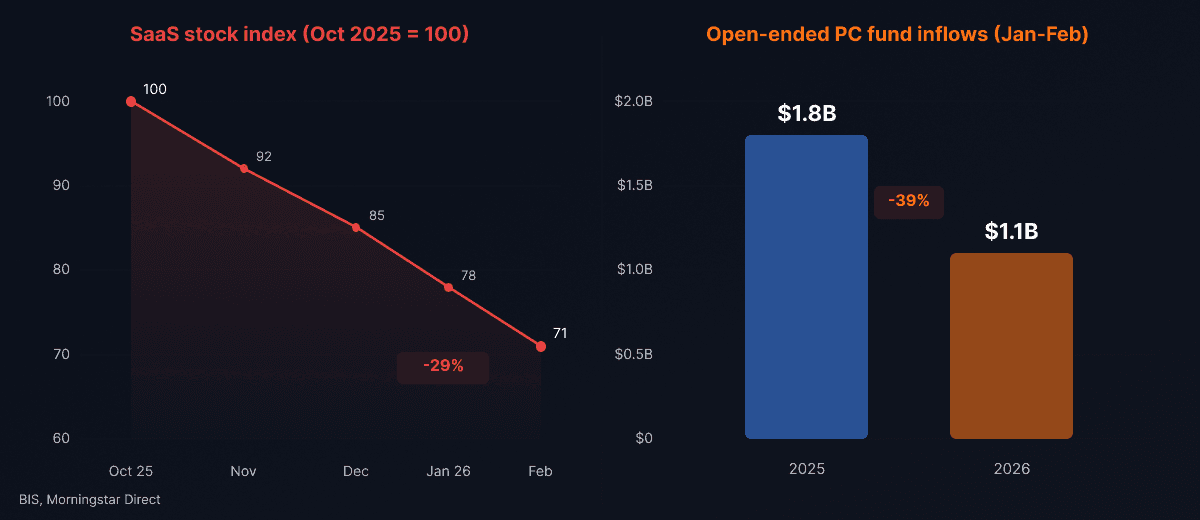

In early 2026, AI disruption fears hit the software sector with measurable force. Publicly traded SaaS stocks fell nearly 30% between October 2025 and February 2026. AI-native tools began automating the exact functions that many enterprise software companies charge subscription fees to provide. For software borrowers financed at peak valuations with floating-rate debt, this meant simultaneous revenue pressure and rising debt service costs.

Oaktree Specialty Lending CEO Armen Panossian noted on a Q1 2026 earnings call that disruption concerns call into question the refinanceability of maturing software loans and that outcomes for some borrowers may prove to be binary. Private credit fund inflows in the first two months of 2026 dropped by more than a third year-on-year. Blackstone's flagship fund BCRED posted its first monthly loss in three years. UBS warned that default rates could climb to 13% in an aggressive disruption scenario. Morgan Stanley's base case projects 8%.

Redemption requests spiked across non-traded Business Development Companies (BDCs) and interval funds, with several large vehicles capping or slowing withdrawals. According to LPL Research, between 25% and 35% of private credit portfolios carry some degree of AI-related disruption risk.

The opacity problem

The AI disruption story is significant on its own. What makes it structurally dangerous is that it is hitting a market defined by opacity. Private credit loans are generally unrated and untraded. Valuations are internally generated by the same managers whose fee income depends on stable marks. When Morningstar analysts tried to assess how far software loan prices had been marked down, they acknowledged there was no active secondary market to provide an answer.

That opacity has already produced outright failures. In February 2026, UK bridging lender MFS collapsed with a £930M collateral shortfall, having allegedly pledged the same property titles to multiple lenders simultaneously. It followed the US bankruptcies of First Brands and Tricolor on similar allegations. The exposed institutions, Barclays, Apollo, Elliott, SMBC, Jefferies, Wells Fargo, were among the most sophisticated in global finance. We covered the MFS collapse in depth in a previous edition of this newsletter. The pattern across all three cases is consistent: verification failure.

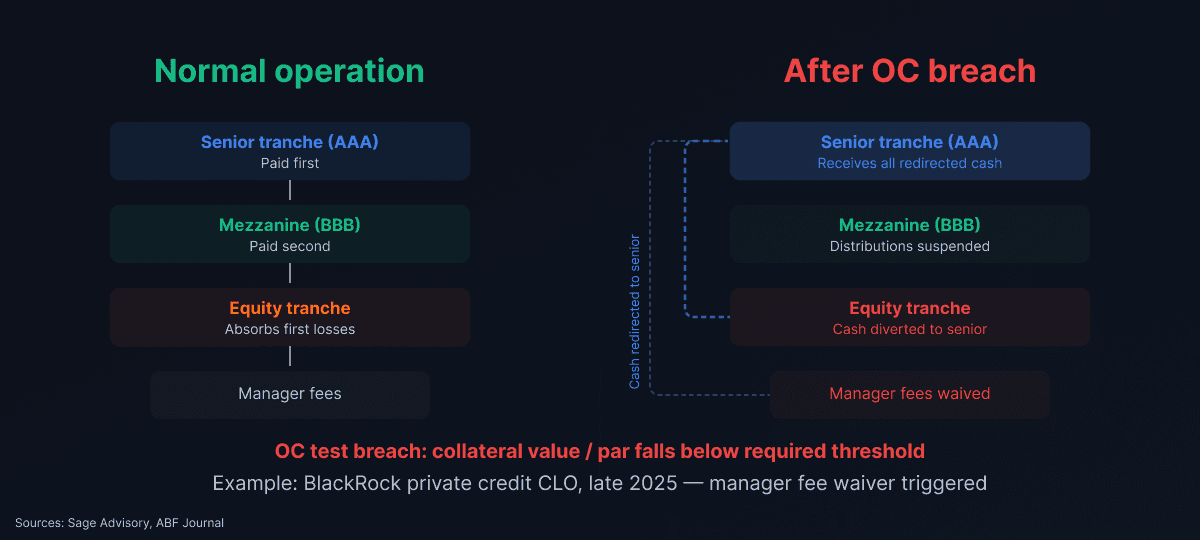

At the structured product level, the stress is becoming mechanical. Private credit CLOs have hit record issuance levels, and when the underlying loans are opaque, the structures built on top inherit that opacity. A BlackRock private credit CLO breached over-collateralisation tests in late 2025, triggering a manager fee waiver and cash flow redirection to senior tranches.

What 5,000 years of lending tells us

The pattern that runs from Mesopotamian temples to Milken's junk bonds to today's private credit market is remarkably consistent.

→ Formal institutions restrict lending.

→ Private capital fills the gap.

→ Growth outruns infrastructure.

→ Opacity accumulates.

→ A shock reveals what was always there.

The Code of Hammurabi addressed this with debt forgiveness and interest caps. Post-Milken regulators addressed it with securities law and capital requirements. After 2008, Basel III and Dodd-Frank addressed it with leverage ratios and risk-weighted assets.

What none of these addressed was the verification layer itself: the ability to confirm, in real time, that collateral exists, that it has not been pledged elsewhere, that portfolio reporting matches reality, and that waterfall mechanics are being enforced as designed.

This is where the structural argument for on-chain infrastructure becomes concrete.

Immutable collateral registries make double-pledging mechanically impossible. Real-time loan tape reporting, of the kind Tranched is building into its architecture, replaces quarterly self-reporting with continuous, auditable data feeds. Automated borrowing base calculations remove the discretion that allows collateral gaps to persist undetected. Programmable waterfall mechanics enforce tranche priority without manual intervention.

None of this requires every participant to adopt blockchain. It requires the plumbing beneath private credit to treat transparency as a structural feature rather than an optional disclosure.

A $3.5T market that has never faced a full credit cycle, concentrated in an asset class that AI is in the process of restructuring, with verification failures surfacing across multiple geographies, may be exactly the forcing function that makes this transition inevitable.

The question is no longer whether the "zero-loss fantasy" holds. It is whether the infrastructure beneath the market is capable of telling participants, in real time, when it does not.