Market Commentary

Welcome to this week’s Tranched newsletter.

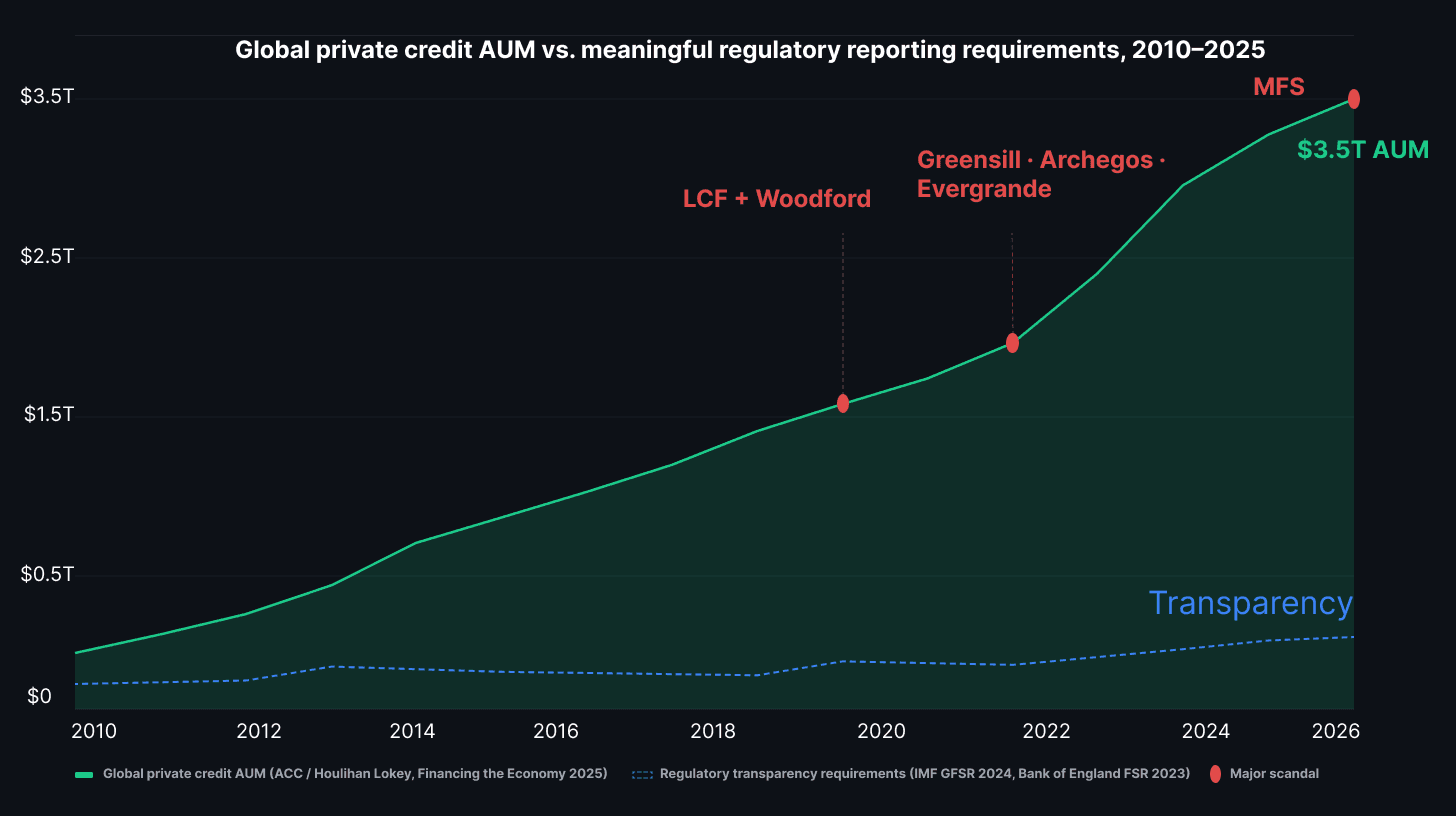

Private credit has spent the last decade growing into a $3.5T market by filling a gap that mainstream banks left behind. The pitch has always been straightforward: direct lending, secured by real assets, managed by specialists.

The problem, visible again in February 2026, is that "secured by real assets" has always depended on someone's word.

That someone, in this case Market Financial Solutions, may have been lying.

What Happened at MFS

Market Financial Solutions was a London-based bridging lender. Founded in 2006, it specialised in short-term property finance for borrowers that mainstream banks wouldn't touch, such as transitional deals, complex structures, fast timelines.

By the end of 2024 it had a £2.4B loan book and institutional backing from Barclays, Santander, Wells Fargo, Jefferies, and Apollo's Atlas SP Partners. In March 2025 it received a clean audit. In February 2026, it entered administration: a creditor-led insolvency process

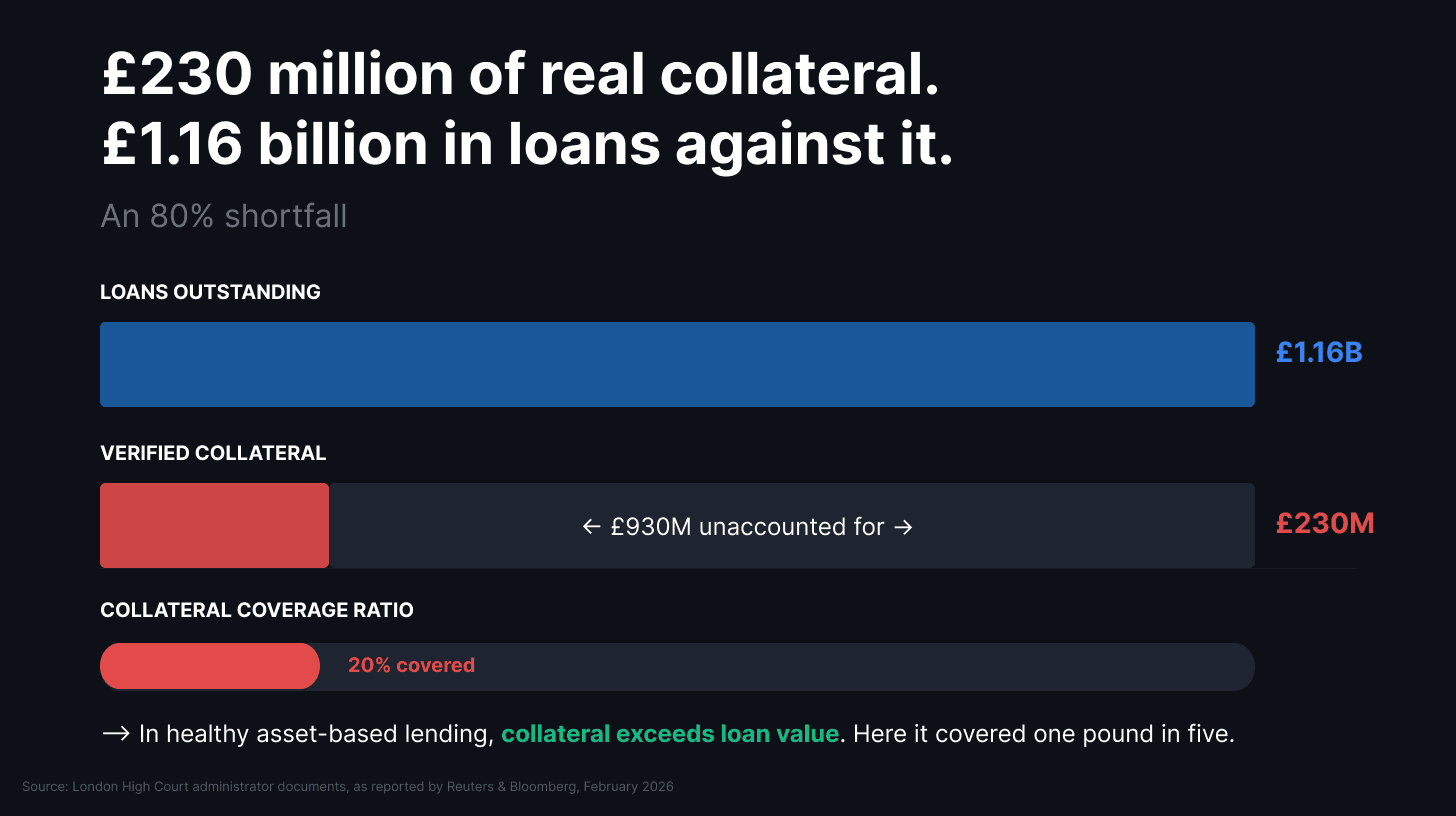

The allegation at the centre of the collapse is double-pledging. The same property titles, administrators claim, were used as collateral for multiple separate loans simultaneously, with none of the lenders aware of the others. When administrators went looking for the assets, they found £230M of verifiable collateral sitting behind £1.16B in loans. An 80% shortfall.

Let’s have a look at the timeline.

🟠 January 2026: Barclays detected anomalies and froze MFS accounts.

🟠 Mid-February, every director except the founder had resigned, including two independent directors appointed specifically to strengthen governance, and the founder’s wife, who left four days before the administration filing.

🟠 February 25, the High Court approved administration following applications from two creditors citing "serious irregularities."

The market reaction was immediate.

📉 Jefferies fell nearly 10% in a single session.

📉 Barclays dropped 4.2%.

📉 The S&P 500 bank index fell 4% on the day.

This was a reaction to not only MFS, but also what this implies about the broader market.

The Pattern

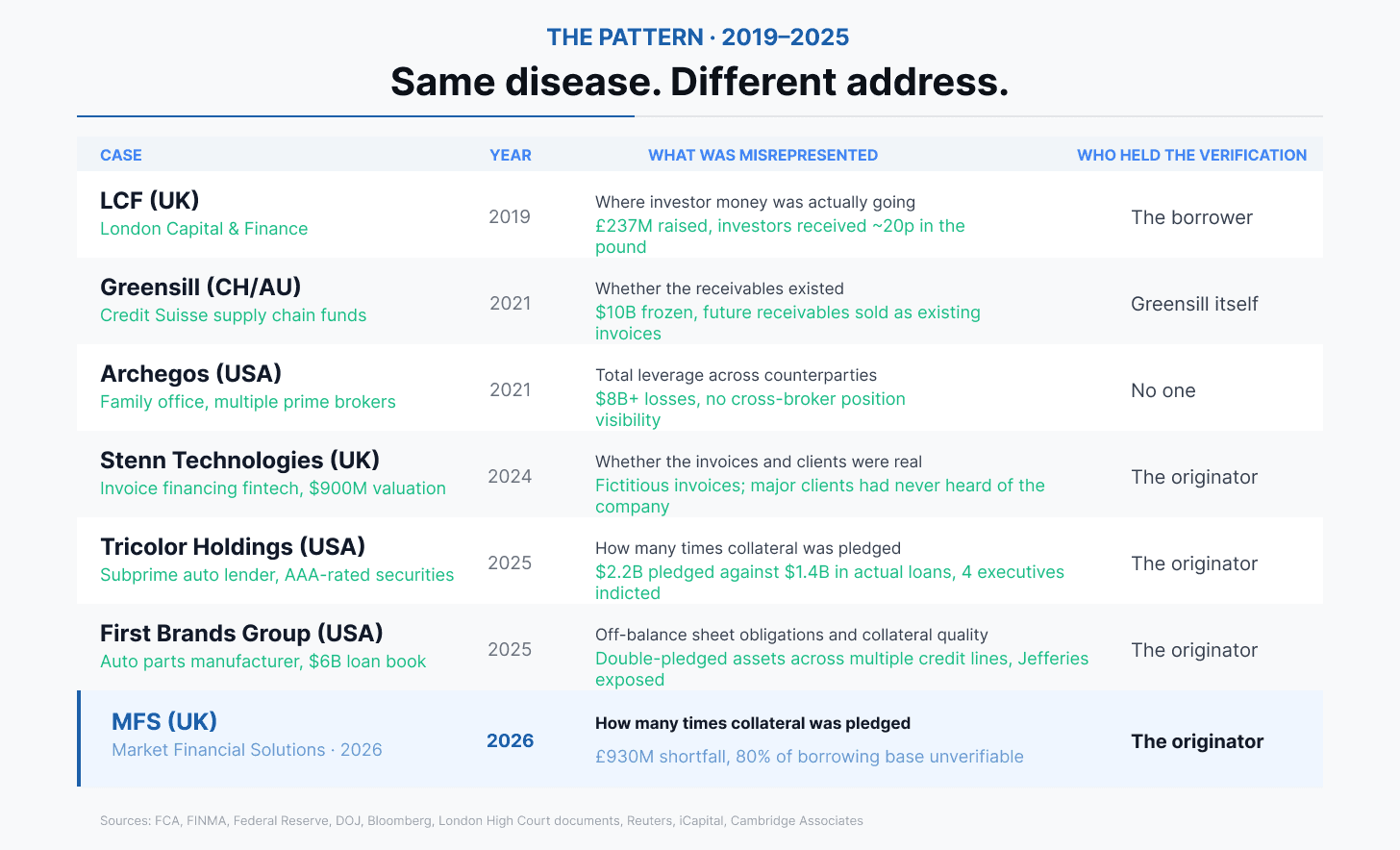

The MFS event belongs to a sequence that has been running for at least seven years.

The IMF's Global Financial Stability Report (April 2024) identified private credit's "lack of transparency" as a core systemic vulnerability and one that "could lead to a deferred realisation of losses followed by a spike in defaults."

The Bank of England's December 2023 Financial Stability Report flagged similar concerns, noting that opacity in private credit limits regulators' ability to understand risk build-up across the sector.

Let’s have a look at some similar cases from the past.

Each of the following cases failed for the same underlying reason: the people providing capital could not independently verify what they were lending against.

We’ll now dive deeper into some of them:

🔵Tricolor Holdings (USA, 2025): Tricolor was a Texas-based subprime auto lender that packaged car loans into AAA-rated securities and sold them to pension funds, insurers, and asset managers. It filed for Chapter 7 liquidation in September 2025 after warehouse lenders discovered alleged double-pledging. Around 40% of its portfolio showed identical attributes to at least one other loan, meaning Tricolor received multiple financings for the same assets. Federal prosecutors subsequently indicted four executives including the CEO. The alleged discrepancy: $2.2B in collateral pledged against $1.4B in actual loans. The same mechanism as MFS. Different asset class, identical structure.

🔵First Brands Group (USA, 2025): First Brands was a Michigan-based auto parts manufacturer that funded an acquisition spree of over 20 companies through incremental term loans and supply chain financing. It was being pitched to investors as a $6B loan opportunity just weeks before collapse. Its use of off-balance sheet working capital facilities was significant and lacked appropriate transparency. The company was subsequently accused of double-pledging assets across multiple credit lines. Jefferies, which had marketed the deal, faced significant reputational damage. Lenders who believed they held secured positions discovered the collateral had already been pledged elsewhere.

🔵Stenn Technologies (UK, 2024): Stenn was a London-based invoice financing fintech valued at $900M in 2022, backed by Citigroup, Barclays, HSBC, and Centerbridge Partners. It collapsed into administration in December 2024 after HSBC, triggered by a passing reference in a US money laundering indictment, began investigating Stenn's transactions and discovered that many of its largest supposed clients had never heard of the company. The invoices underpinning its loan book were fictitious.

🔵Greensill Capital / Credit Suisse (Switzerland & Australia, 2021) : Greensill packaged supply chain invoices into investment products and distributed them through Credit Suisse to institutional clients. Over $10B flowed into four funds with a growing proportion of those "invoices" being projections of future receivables rather than not existing claims, from companies of uncertain creditworthiness.

A peer-reviewed case study by Bhattacharya & Reddy describes it as a textbook failure of counterparty due diligence dressed up as financial innovation.

🔵Archegos Capital (USA, 2021) : Archegos held large, concentrated positions in a small number of stocks via total return swaps, which carried no public disclosure requirement. Multiple prime brokers including Credit Suisse, Nomura, Morgan Stanley, Goldman Sachs, each extended leverage independently, each believing they were managing a contained risk. When the positions unwound, Credit Suisse lost approximately $5.5B and Nomura lost $2.9B. The Federal Reserve's subsequent guidance on counterparty credit risk identified the absence of cross-broker position visibility as the central failure.

🔵London Capital & Finance (UK, 2019): LCF raised £237M from 11K retail investors through mini-bonds marketed as safe and diversified. The proceeds were loaned to approximately 12 businesses, nearly all connected to four individuals. PwC formed suspicions of fraud during the audit and didn't report them; three audit firms were subsequently sanctioned by the Financial Reporting Council. Investors were told to expect around 20 pence in the pound. The FCA logo on the product, one investor noted, was "the fatal thing" as it implied oversight that wasn't there.

Three Things That Keep Going Wrong

Across these cases, the same structural weaknesses appear each time.

Collateral that can't be independently verified.

In property lending, the land registry can only be checked manually, periodically, and by parties who depend on the originator to surface the right information. The gap between what's represented and what's real is only visible when someone goes looking, usually after the fact.

Verification left to the interested party. In almost every case, the entity attesting to asset quality was the entity with the most to gain from overstating it.

🟠 Greensill reviewed its own receivables.

🟠 MFS managed its own collateral records.

🟠 LCF's lending was invisible to its auditors.

The due diligence chain consistently ended at the point where independence mattered most.

Regulation that arrives after the damage.

🟠 The Woodford fine came in 2025, six years after the fund suspended.

🟠 FINMA's Greensill enforcement concluded two years post-collapse.

Regulatory responses are thorough and important, but they are post-mortems and don’t prevent the next case from happening.

What On-Chain Infrastructure Changes

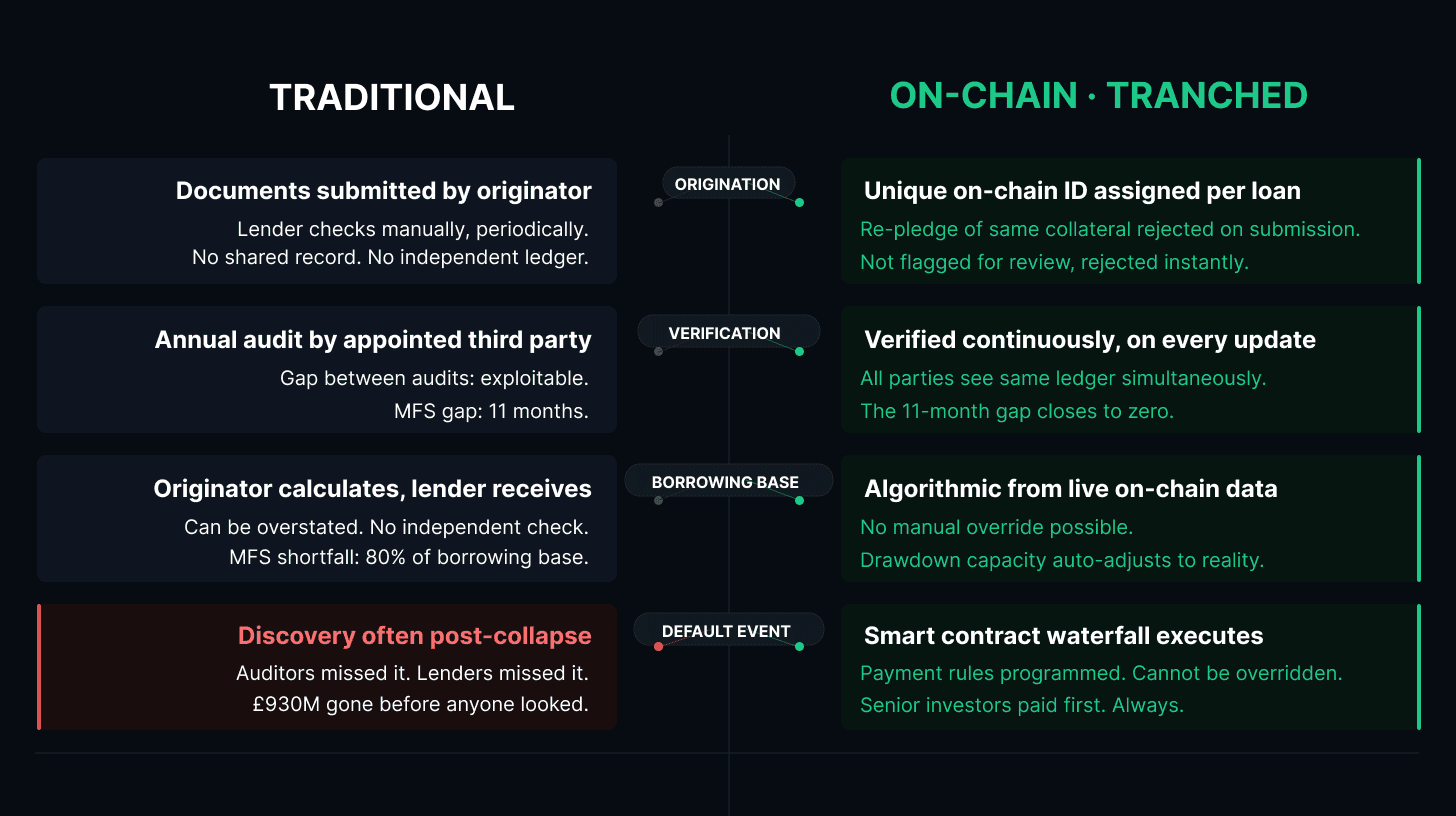

A key argument for moving private credit on-chain is that certain failures become structurally impossible rather than merely discouraged.

→ When a loan is registered on a shared, immutable ledger, visible simultaneously to all authorised parties, double-pledging gets rejected on submission.

→ When a borrowing base is calculated algorithmically from live on-chain data, no originator can manually override it.

→ When a waterfall executes through a smart contract, the payment rules don't bend based on who's asking.

As of mid-2025, over $13.3B in private credit had been tokenised globally, growing 74% in twelve months. BlackRock, KKR, Hamilton Lane, and Apollo are active participants.

This is what Tranched is built for.

Every loan registered through Tranched's protocol receives a unique on-chain ID. Re-pledging the same collateral is rejected at the protocol level.

The borrowing base is calculated from live on-chain data with no manual override.

All authorised parties including investors, facility agents and custodians, see the same state of the pool at the same time.

Eligibility rules and concentration limits are encoded at deployment and enforce themselves continuously.

Collateral is verified on every update.

The eleven-month window between MFS's clean March 2025 audit and its February 2026 collapse, in which an 80% collateral shortfall was invisible, closes to zero.

The Broader Point

Private credit provides capital to businesses and transactions that mainstream banks won't touch, at a scale the economy depends on. The cases above aren't arguments for changing the infrastructure it runs on.

The current infrastructure was built for a market that didn't have an alternative. That alternative now exists.

The question for anyone operating in private credit is how long the existing infrastructure remains acceptable given what we now know what it allows.